General provisions for accounting for the release of defects in the software "1C:Manufacturing Enterprise Management 8"

To account for the costs of producing defective products, the configuration uses:

Movements on account 28 “Defects in production”:

For tax accounting:

Movements in the accumulation register “Defects in production”:

Note! Account 28 is a cost account, so it does not provide quantitative accounting. This account is intended to accumulate costs associated with the production of defective products.

The invoice itself does not provide for the “Nomenclature” sub-conto, that is, we do not see which specific defective products were produced.

The program provides the possibility of object-by-object accounting of released defective products in the “Defects in Production” register.

At the end of the month, the account balance is 28 is recognized as a final defect and is written off in full to the account. 20 for distribution to the cost of manufactured good products.

Whatever option you choose for keeping records of defects, it is important to remember that the release of defects (D 28) is brought to the fact by the program, and the write-off of the account. 28 (K 28) – no.

Accounting for losses from defects

Defects in production are considered to be products, products, semi-finished products, parts, work that, in terms of their quality, do not meet established standards or technical conditions and cannot be used for their intended purpose or can be used after eliminating detected defects.

Depending on the nature of the defects, a distinction is made between correctable and irreparable (final) defects.

Correctable defects are products, semi-finished products (parts and assemblies) and work that can be used for their intended purpose after correction of defects, and their correction is technically possible and economically feasible.

Final (irreparable) defects are considered to be products, semi-finished products, parts and work that cannot be used for their intended purpose and the correction of which is technically impossible or economically impractical, that is, in cases where correcting the defect will require costs exceeding the costs of manufacturing new products instead defective.

In accordance with the Chart of Accounts, accounting for losses from defects is carried out using account 28 “Defects in production”. The debit of account 28 takes into account the cost of irreparable defects, as well as the costs of correcting defects. The credit of account 28 reflects amounts that reduce losses from defects, in particular, the cost of defective products capitalized at the price of possible use, amounts recovered from those responsible for the defects, amounts recovered from suppliers of substandard materials, the use of which was defective.

Non-refundable amounts of losses from defects are included in the cost of those types of products for which defects are detected. If in the period in which a defect was detected, this type of product was not produced, then the amount of losses from defects is distributed by type of product as general production expenses.

Internal marriage

If a defect is detected directly at the enterprise, at certain stages of the technological process, or directly in finished products before they are transferred to customers, the defect is considered internal.

Losses from internal defects are reflected in the costs of the month in which the defect was detected.

The cost of internal irreparable defects, to be reflected on account 28, is determined by the amount of costs for the manufacture of defective products, which includes the cost of raw materials used, labor costs and the corresponding amounts of unified social tax, costs of maintaining and operating equipment, and part of general production expenses.

Accounting for irreparable internal defects is documented by accounting entries:

- Dt 28

“Defects in production”

Kt 20

“Main production”,

21

“Semi-finished products of own production”,

43

“Finished products” - the cost of defective products is written off; - Dt 10

“Materials”,

21

“Semi-finished products of own production”,

41

“Goods”

Kt 28

“Defects in production” - defective products are capitalized at the price of possible use; - Dt 73

“Settlements from personnel for other operations”

Kt 28

“Defects in production” - amounts to be recovered from those responsible for the defect have been accrued; - Dt 76

subaccount “Calculations for claims”

Kt 28

“Defects in production” - amounts to be recovered from suppliers of defective materials have been accrued; - Dt 20, 23 Kt 28

“Defects in production” - losses from defects are included in the cost of production

Example

The company discovered an irreparable defect in a batch of products, the cause of which was the use of low-quality materials.

The costs of manufacturing defective products were: Cost of materials consumed - 25,000 rubles; Salary - 15,000 rubles; The amount of unified social tax is 5,340 rubles; The share of general production expenses is RUB 7,500. The possible sale price of defective products is 20,000 rubles. A claim has been filed against the supplier of low-quality materials; the amount to be recovered is 10,000 rubles.

Contents of operation Dt CT Amount, rub The cost of defective products is reflected (25,000 + 15,000 + 5,340 + 7,500) 28 20 52 840 Defective products are capitalized at the price of possible sale 43 28 20 000 The amount to be collected from the supplier has been accrued 76 28 10 000 Losses from defects are included in the cost of production (52,840 – 20,000 – 10,000) 20 28 22 840

The cost of internal correctable defects includes the cost of raw materials and supplies spent in correcting defects, the wages of employees directly involved in correcting defects, the corresponding amounts of accrued unified social tax, the share of costs for the maintenance and operation of equipment and general production costs attributable to operations to correct defects.

Accounting for correctable internal defects is documented using the following accounting entries:

- Dt 29

“Defects in production”

Kt 10

“Materials” - the cost of raw materials and supplies used to correct the defect has been written off; - Dt 28

“Defects in production”

Kt 70

- calculation of wages for workers involved in correcting defects; - Dt 28

“Defects in production”

Kt 69

- accrual of unified social tax for the wages of workers engaged in correcting defects; - Dt 28

“Defects in production”

Kt 25

- the corresponding share of general production costs is written off; - Dt 73

“Settlements with personnel for other operations”

Kt 28

“Defects in production” - amounts to be recovered from those responsible for the defect have been accrued; - Dt 76

subaccount “Calculations for claims”

Kt 28

“Defects in production” - amounts to be recovered from suppliers of defective materials have been accrued; - Dt 20, 23 Kt 28

“Defects in production” - the costs of correcting defects are included in the cost of production

Example

A defective batch of products was detected at the enterprise.

The costs of manufacturing defective products were: Cost of materials consumed - 25,000 rubles; Salary - 15,000 rubles; The amount of unified social tax is 5,340 rubles; The share of general production expenses is RUB 7,500. Total - 52,840 rubles. The costs for correcting the defect were: Cost of materials used - 8,000 rubles; Salary - 7,000 rubles; The amount of UST is RUB 2,492; The share of general production expenses is 1,500 rubles. Total - 18,992 rubles 5,000 rubles were recovered from those responsible for the marriage.

Contents of operation Dt CT Amount, rub The cost of materials for correcting defects was written off 28 10 8 000 Wages accrued for correcting defects 28 70 7 000 UST accrued 28 69 2 492 General production costs incurred to correct defects have been written off 28 25 1 500 The amount to be recovered from those responsible for the marriage has been accrued 73 28 5 000 The amount collected is withheld from the employees' salaries 70 73 5 000 The amount of losses from defects is included in the cost of production (8,000 + 7,000 + 2,492 - 5,000) 20 28 13 992 The production cost of finished products is reflected (52,840 + 13,992) 43 20 66 832

Stay up to date with the latest changes in accounting and taxation! Subscribe to Our news in Yandex Zen!

Subscribe

Possibilities of the program for recording marriages

The typical mechanism of the program offers the following options for recording the release of defects.

Simplified scheme for recording defect release

This scheme is suitable for you if:

- the enterprise does not need to account for the release of defects in quantitative terms;

- Only final rejects are issued;

- there are no flow movements on the account. 28 (transfer to the guilty unit, transfer to the guilty person).

In this case, we release defective products directly to the account. 28, without coming to the warehouse. On this account we also accumulate other expenses associated with the release of defects and increasing the cost of production.

- D 28 K 20 – release of defective products at book value.

- D 28 K 10, 70, 69, 60 - collection of other costs for producing defects.

- D 20 K 28 - write-off of defective costs to the cost of production.

The release of defects in the program (D count 28) is identical to the release of finished products (D count 43). The release is made according to the same specifications at the accounting (planned) release price. At the end of the month, the release of the marriage is brought to the surface. The amount of collected costs is distributed to the production of suitable products.

Let's consider how the mechanism of this scheme for recording the release of defects is implemented in the program.

Employee remuneration

The employee who manufactured defective products is paid as follows. If the manufactured product is a complete (irreparable) defect, then in this case the employee’s work is not paid. If a partial (correctable) defect is identified due to the fault of the employee, then it is paid at reduced rates depending on the degree of suitability of the manufactured products. Such rules are established by parts 2 and 3 of Article 156 of the Labor Code of the Russian Federation.

Situation: in what documents are losses from marriage recorded?

In documents approved by the head of the organization.

Any fact of economic life, including the release of marriage, must be confirmed by a primary document (Part 1 of Article 9 of the Law of December 6, 2011 No. 402-FZ).

The forms of primary accounting documents are approved by the head of the organization (Part 4 of Article 9 of the Law of December 6, 2011 No. 402-FZ). For example, if a defect is detected in production, a report can be issued. In this case, the document must contain the mandatory details provided for in Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ. In addition, the act should indicate the reasons for the defect, the quantity of defective products, the culprit of the defect, the costs of eliminating the defect and (or) the cost of the defective product, the amounts to be recovered from the culprits of the defect.

Make deductions from your salary to reimburse expenses related to the release of marriage in the same way as deductions related to compensation for material damage.

Conditions of the problem

Product output - Shop 1 (Table 1):

| № | Products | Issue volume | Quality | Planned price | Planned cost |

| 1 | Closet | 10 | Good products | 10 000 | 100 000 |

| 2 | Coffee table | 20 | Good products | 2500 | 50 000 |

| 3 | Closet | 1 | Marriage | 10 000 | 10 000 |

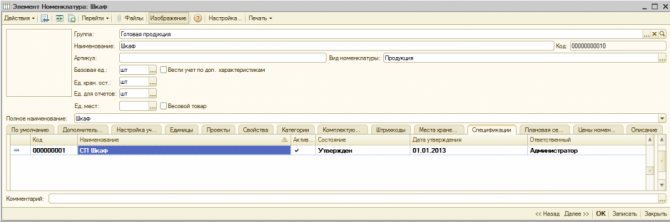

We will set specifications (material consumption standards) for manufactured products. Specifications are set in the item card on the “Specifications” tab:

Note. This tab is available only if the value “Production” is specified in the “Type of reproduction” field (the “Advanced” tab):

During the production process in Workshop 1, the following costs were collected:

Release of defective products

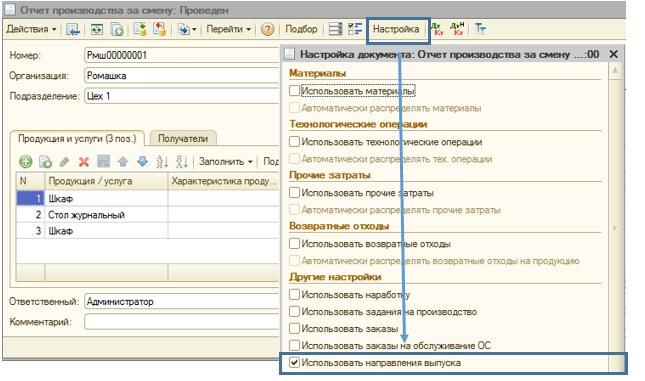

The release of defects is reflected in the document “Production Report for the Shift”.

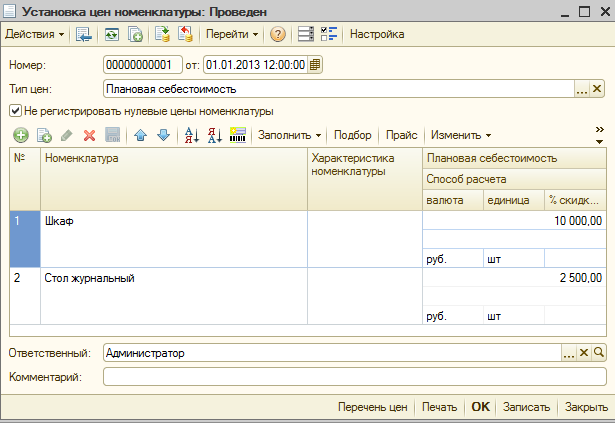

Attention. Before reflecting product output, planned output prices must be set (document “Setting item prices”):

To reflect the release of defects in the document, you need to set the “Use release direction” flag in the additional settings:

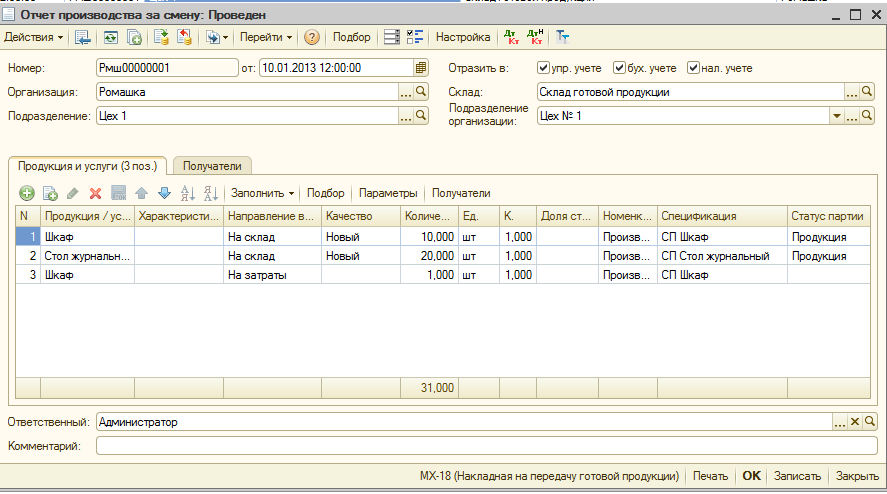

According to the conditions of the example, we will reflect the production of both suitable and defective products.

Menu: Tab “Products and Services”

- When releasing suitable products, in the “Direction of release” column, indicate “To warehouse”.

- When releasing defective products - “At costs”.

Note. The “Specification” field must be filled in for both acceptable and defective products.

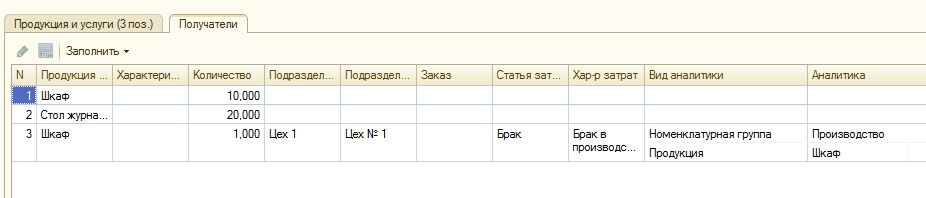

Menu: Tab “Recipients”

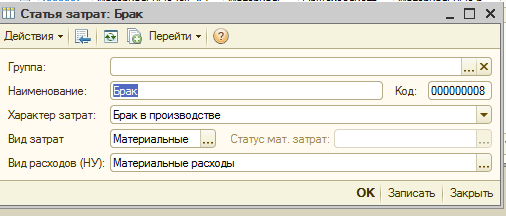

Important . To account for marriage according to the account. 28 as analytics it is necessary to use a cost item with the nature of costs “Defects in production”:

In the “Analytics” field for the “Products” Analytics Type, you can indicate which specific defective products were produced. This information will be recorded in the accumulation register “Defects in production” and accordingly will be displayed in the standard report “Statement of defects in production”.

Object-by-object accounting of defects

If object-by-object accounting of defects is maintained (that is, the “Analytics” field is filled in), then the costs of producing this defective product (cabinet, 1 piece) will be included in the cost of producing the same good product (producing cabinets in the amount of 10 pieces).

If object-by-object accounting is not maintained, then the costs of releasing defects will be included in the cost of all good products produced during the period.

When posting the document, the following transactions will be generated:

- in accounting:

- for tax accounting:

Calculation of the cost of manufactured defects. Closing the account 28

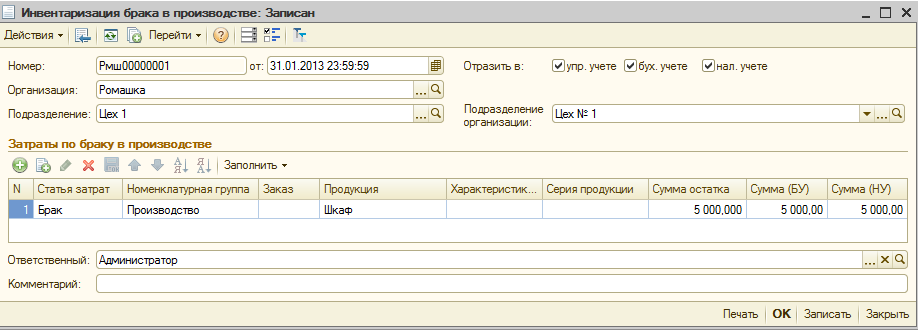

If at the end of the period the costs of releasing defects should remain in work in progress and should not be included in the cost of production, then at the end of the month it is necessary to enter the document “Inventory of defects in production”.

This document is entered once at the end of the month for each production unit. Filling occurs automatically by clicking the “Fill” button - with balances from the “Production Defects” register:

For our example, we will assume that defects should not remain in the WIP. And the entire amount of costs for producing defective products should go towards increasing the cost of producing suitable products.

Accounting

Accounting for defects caused by an employee depends on whether the defect is partial (correctable) or complete (irreparable).

If there is a partial defect, reflect all costs for its correction in the following entries:

Debit 28 Credit 10 (70, 69, 25, 68…)

– expenses for correcting defects committed by the employee are reflected.

If there is a complete defect, reflect its amount by posting:

Debit 28 Credit 20, 21, 43

– the cost of work in progress, semi-finished products, finished products recognized as defective is written off.

The amount that is withheld from the employee for releasing a defect is reflected as follows:

Debit 73 Credit 28

– reflects the amount that will be withheld from the employee to reimburse the costs of releasing the defect.

Such wiring can be done in one of the following cases:

- the amount of the defect does not exceed the employee’s average monthly earnings (if it exceeds, make the entry for the amount of the average monthly earnings);

- the employee admitted guilt for the marriage and its amount;

- The court made a decision to withhold the amount of the marriage from the employee.

If these conditions are not met, write off the reject amount as follows:

Debit 20 Credit 28

– losses from defects are included in the costs of main production.

This procedure follows from the Instructions for the chart of accounts.

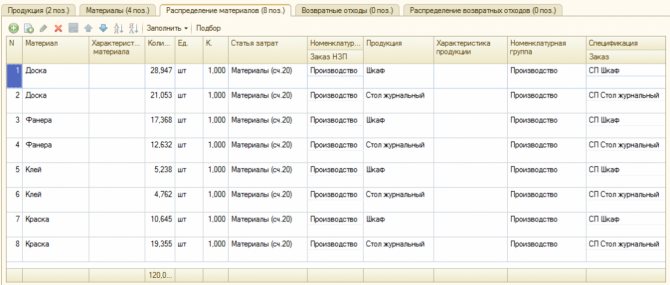

Distribution of material costs (document “Distribution of materials for production”)

Important. Material costs in 1C:UPP can be included in the production cost either by the boiler method (distribution of costs according to a given distribution base), or distributed according to the share of each material according to the specification in the production cost.

In our example, consider the distribution of material costs according to specifications.

We will make a manual calculation of material costs included in the cost of manufactured products.

For example, 50 boards were written off in Workshop 1. To produce 1 cabinet according to specification, 10 boards are required. For the entire production of cabinets (including defective ones), the requirement is 10 * 11 = 110 pieces. According to the standard, 4 boards are required to produce one coffee table. Total planned requirement 4 * 20 = 80 pcs.

Let's assume that there was no work in progress at the end of the month.

When distributing, we find that 50 units were used to produce 11 cabinets. * (110/190) = 28,947 pcs.

The cost of 1 board is 300 rubles. Accordingly, the material costs for spent boards for the production of all cabinets (including defective ones) amount to 300 * 28.947 = 8684.10 rubles.

| № | Products | Mat. costs (pcs.) | Mat. costs (rub.) | ||||||

| Board | Plywood | Glue | Dye | Board | Plywood | Glue | Dye | ||

| 1. | Closet | 28,947 | 17,368 | 5,238 | 10,645 | 8684,1 | 2 605,2 | 261.90 | 745,15 |

| 2. | Coffee table | 21,053 | 12,632 | 4,762 | 19,355 | 6 315,9 | 1 894,8 | 238,1 | 1 354,85 |

| Total: | 50 | 30 | 10 | 30 | 15000 | 4500 | 500 | 2100 | |

Total material costs:

- Wardrobe (11 pieces) – RUB 12,296.35.

- Coffee table (20 pcs.) – RUB 9,803.65.

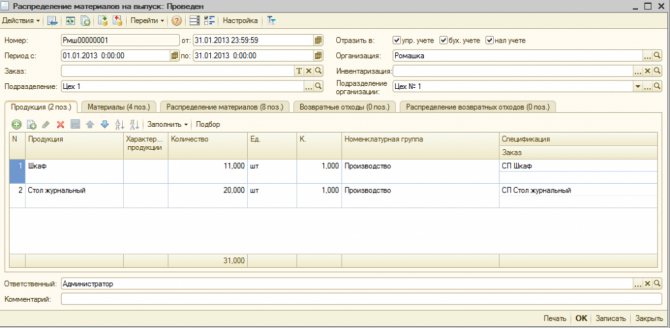

In the program, material costs can be distributed to a specific output directly in the release document (“Production report for a shift”) or in a specialized document “Distribution of materials per output.”

The “Products” tab is automatically filled with the list of released finished products, including defective ones, using the “Fill” button. If necessary, the data can be edited:

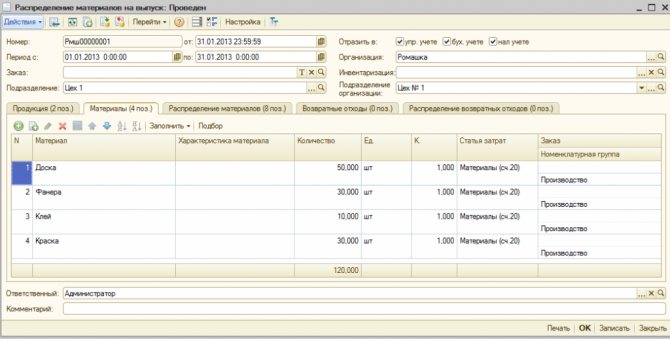

The “Materials” tab is filled in with all material costs written off for the specified period for the department selected in the document header:

On the “Distribution of Materials” tab, the automatic distribution of material inventories to manufactured products occurs according to the specifications:

Thus, we see that the material component of the cost of defective products is calculated in exactly the same way as for suitable products.

Income tax

When calculating income tax, losses from marriage are taken into account in full as part of other expenses (subclause 47, clause 1, article 264 of the Tax Code of the Russian Federation). It does not matter at whose expense the defect is written off: at the expense of the employee or at the expense of the organization.

The amount of damage that the employee must pay must be reflected in non-operating income (clause 3 of Article 250 of the Tax Code of the Russian Federation).

Under the cash method, the amount of non-operating income will be equal to the amount of deductions from the employee’s salary in each reporting period (clause 2 of Article 273 of the Tax Code of the Russian Federation).

When using the accrual method, determine income as the amount of compensation for damage as of the date the guilty party was found guilty (for example, on the date of signing an order to withhold damage from an employee’s salary). If the organization seeks compensation for damages through the court, the date of recognition of income is the day the court decision enters into force.

This is stated in subparagraph 4 of paragraph 4 of Article 271 of the Tax Code of the Russian Federation.

The court decision comes into force within 10 days from the date of its adoption by the court, provided that it has not been appealed (Articles 209, 321, 338 of the Civil Procedure Code of the Russian Federation). In this case, income is recognized in the amount specified in the court decision.

An example of deducting the cost of a repairable defect from an employee’s salary. The organization applies a general taxation system

LLC "Proizvodstvennaya" applies a general taxation system. The contribution rate for insurance against accidents and occupational diseases is 0.9 percent. The organization pays contributions to compulsory pension (social, medical) insurance at general rates. The organization produces office furniture. In March, a correctable defect occurred in the production of products. The reason for the defect was failure to comply with the technology by worker A.I. Ivanov. The employee does not have rights to deductions for personal income tax.

The organization's expenses for correcting the defect amounted to 24,188 rubles, including:

- cost of materials used – 8480 rubles;

- the salary of employees correcting marriages is 12,000 rubles;

- the amount of contributions for compulsory pension (social, medical) insurance – 3600 rubles;

- the amount of contributions for insurance against accidents and occupational diseases is 108 rubles.

Ivanov’s average monthly salary is 27,000 rubles.

Ivanov's partial marriage was paid at reduced rates. In March, when the employee committed marriage, his salary was accrued in the amount of 22,000 rubles, personal income tax on this amount is 2,860 rubles. (RUB 22,000 × 13%).

Since the amount of the marriage is less than the average salary of an employee, Ivanov fully compensates for the damage caused to the organization. The maximum amount that can be withheld from an employee in March is: (RUB 22,000 – RUB 2,860) × 20% = RUB 3,828.

The accountant made the following entries in accounting.

In March:

Debit 28 Credit 10 – 8480 rub. – the cost of materials used to correct the defect has been written off;

Debit 28 Credit 70 – 12,000 rub. – salaries were accrued to employees correcting marriages;

Debit 28 Credit 69 “Settlements with the Pension Fund” – 2640 rubles. (RUB 12,000 × 22%) – pension contributions have been accrued;

Debit 28 Credit 69 subaccount “Settlements with the Social Insurance Fund” – 348 rubles. (RUB 12,000 × 2.9%) – contributions to the Russian Social Insurance Fund have been accrued;

Debit 28 Credit 69 “Settlements with FFOMS” – 612 rubles. (RUB 12,000 × 5.1%) – contributions to the Federal Compulsory Medical Insurance Fund have been accrued;

Debit 28 Credit 69 subaccount “Settlements with the Social Insurance Fund for contributions to insurance against accidents and occupational diseases” - 108 rubles. (RUB 12,000 × 0.9%) – premiums for insurance against accidents and occupational diseases have been calculated;

Debit 73 Credit 28 – 24,188 rub. – the costs of correcting the defect are attributed to the guilty employee;

Debit 20 Credit 70 – 22,000 rub. – Ivanov’s salary for March was accrued;

Debit 20 Credit 69 “Settlements with the Pension Fund” – 4840 rubles. (RUB 22,000 × 22%) – pension contributions are calculated from Ivanov’s salary;

Debit 20 Credit 69 subaccount “Settlements with the Social Insurance Fund” – 638 rubles. (RUB 22,000 × 2.9%) – contributions to the Russian Social Insurance Fund were accrued from Ivanov’s salary;

Debit 20 Credit 69 “Settlements with FFOMS” – 1122 rubles. (RUB 22,000 × 5.1%) – contributions to the FFOMS are accrued from Ivanov’s salary;

Debit 20 Credit 69 subaccount “Settlements with the Social Insurance Fund for contributions to insurance against accidents and occupational diseases” - 198 rubles. (RUB 22,000 × 0.9%) – contributions for insurance against accidents and occupational diseases were calculated from Ivanov’s salary;

Debit 70 Credit 68 subaccount “Personal Income Tax Payments” – 2860 rubles. (RUB 22,000 × 13%) – personal income tax was withheld from Ivanov’s salary.

Debit 70 Credit 73 – 3828 rub. – losses from marriage were withheld from Ivanov’s salary.

In April:

Debit 70 Credit 50 – 15,312 rub. (22,000 rubles – 2860 rubles – 3828 rubles) – Ivanov’s salary was issued.

When calculating income tax, the accountant included in expenses the cost of the correctable defect - 24,188 rubles, and reflected the amount of compensation in income - 24,188 rubles.

An example of deducting the cost of an irreparable defect from an employee’s salary. The organization applies a general taxation system

LLC "Proizvodstvennaya" applies a general taxation system. The contribution rate for insurance against accidents and occupational diseases is 0.9 percent. The organization pays contributions to compulsory pension (social, medical) insurance at general rates. Due to non-compliance with technology in April, worker A.I. Ivanov allowed the product to be defective. Marriage cannot be fixed. The commission estimated losses from defects (cost of materials, employee’s salary, salary accruals, etc.) at 20,000 rubles.

The average salary of an employee is 15,000 rubles. Ivanov has no rights to deductions for personal income tax.

Complete marriage is not paid for. Therefore, in April, when the employee committed a marriage, his salary was accrued in a smaller amount - 10,000 rubles.

In this case, the amount of material damage (RUB 20,000) is greater than the average employee salary (RUB 15,000). Therefore, by order of the manager, the cost of losses within 15,000 rubles is withheld from the employee’s earnings.

The accountant made the following entries in accounting.

In April:

Debit 28 Credit 20 – 20,000 rub. – the actual cost of the defect is written off;

Debit 73 Credit 28 – 15,000 rub. – losses from defects have been reduced by the amount of the employee’s average monthly earnings;

Debit 20 Credit 28 – 5000 rub. (20,000 rubles – 15,000 rubles) – losses from defects are written off against the cost of similar products manufactured in the reporting period;

Debit 20 Credit 70 – 10,000 rub. – the employee’s wages are accrued;

Debit 20 Credit 69 “Settlements with the Pension Fund” – 2200 rubles. (RUB 10,000 × 22%) – pension contributions accrued;

Debit 20 Credit 69 subaccount “Settlements with the Social Insurance Fund” – 290 rubles. (RUB 10,000 × 2.9%) – contributions to the Russian Social Insurance Fund have been accrued;

Debit 20 Credit 69 “Settlements with FFOMS” – 510 rubles. (RUB 10,000 × 5.1%) – contributions to the Federal Compulsory Medical Insurance Fund have been accrued;

Debit 20 Credit 69 subaccount “Settlements with the Social Insurance Fund for contributions to insurance against accidents and occupational diseases” - 90 rubles. (RUB 10,000 × 0.9%) – premiums for insurance against accidents and occupational diseases have been calculated;

Debit 70 Credit 68 subaccount “Personal Income Tax Payments” – 1300 rubles. (RUB 10,000 × 13%) – personal income tax withheld.

In April, when an employee committed a marriage, the organization can recover only 1,740 rubles at a time. ((RUB 10,000 – RUB 1,300) × 20%).

Debit 70 Credit 73 – 1740 rub. – losses from marriage are withheld from the employee’s salary.

In May:

Debit 70 Credit 50 – 6960 rub. (RUB 10,000 – RUB 1,300 – RUB 1,740) – the employee’s salary was issued.

The organization calculates income tax on a monthly basis (accrual method). In April, the accountant included in expenses the cost of an irreparable defect - 20,000 rubles, and reflected the amount of compensation in income - 15,000 rubles.

Distribution of other costs

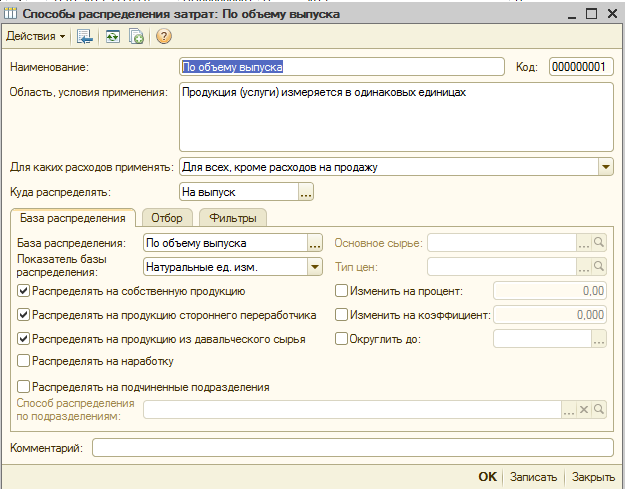

Other costs in the program are included in the cost of production according to the methods of distribution of cost items.

Menu: information register “Methods of distribution of cost items of an organization”

In our example, we will set the distribution method for other costs “By volume of output” (in quantity).

Calculation example. Costs for labor costs included in the cost of manufactured cabinets = 10,000 rubles. (ZPL) / (11 (production of cabinets) / 31 (entire volume of production) = 3,548.39.

| № | Products | PPL (rub.) | Social fear (rub.) | Services (RUB) | Total (RUB) |

| 1. | Closet | 3 548,39 | 709,68 | 1 774,19 | 6032,26 |

| 2. | Coffee table | 6 451,61 | 1 290,32 | 3 225,81 | 10967,74 |

| Total: | 10 000 | 2000 | 5000 | 17 000 |

Calculation of production costs

Let's manually calculate the cost of each unit of production (before including the costs of defects in the cost of producing cabinets):

| Products | Production volume (pcs.) | Material costs (rub.) | Other costs (RUB) | Production cost (RUB) | Unit cost (RUB) |

| Closet | 11 | 12 296,35 | 6032,26 | 18 328,61 | 1666,24 |

| Coffee table | 20 | 9 803,65 | 10 967,74 | 20 771,39 | 1038,57 |

Let's manually calculate the cost of manufactured good products:

| Products | Production volume (pcs.) | Material costs (rub.) | Other costs (RUB) | Increase in price for defective production (rub.) | Production cost (RUB) | Unit cost (RUB) |

| Closet | 10 | 12 296,35 | 6032,26 | 1666,24 | 19 994,85 | 1999,49 |

| Coffee table | 20 | 9 803,65 | 10 967,74 | 20 771,39 | 1038,57 |

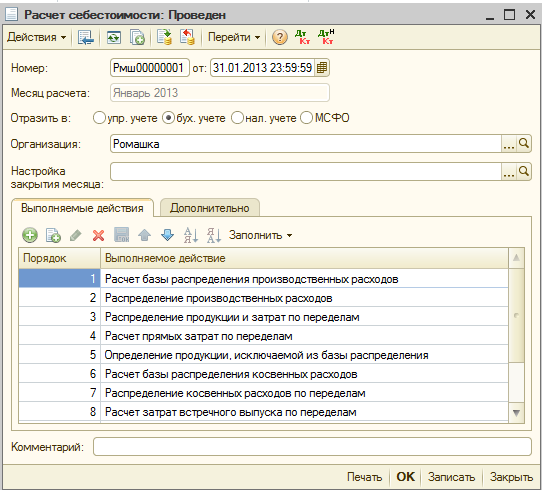

The formation of the cost of all manufactured products (including defective ones) in the program is carried out using the document “Cost Cost Calculation”:

When carrying out this regulatory document, entries will be generated to generate the actual cost of production (including defective products):

The cost of producing defective products is included in the cost of producing suitable products:

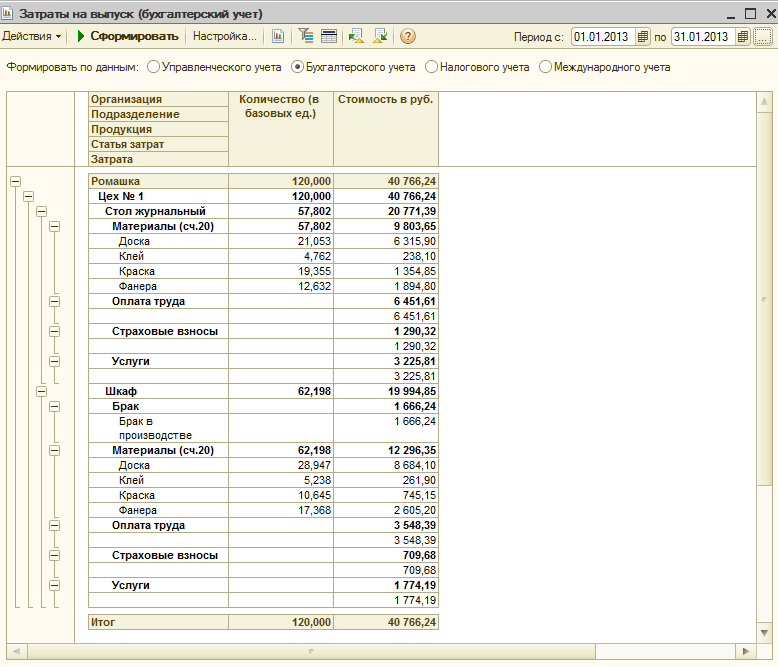

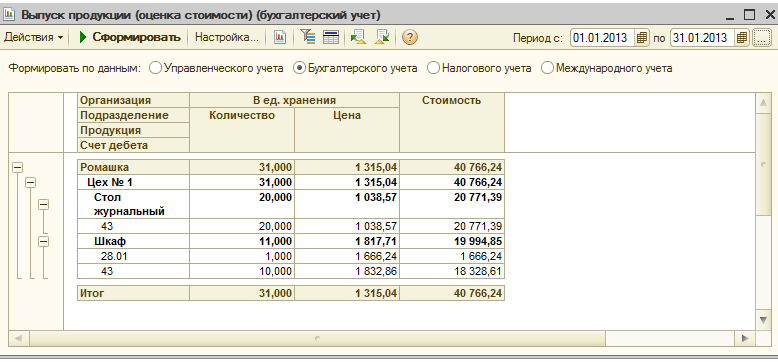

As a result, when carrying out the document “Calculation of cost”, we will obtain the cost of each type of manufactured product. This information can be analyzed using the “Output Costs” report:

The “Quantity” column indicates the amount of inventory written off as expenses.

In the “Cost” column we can see the cost of the entire production of suitable products received into the warehouse.

Note. The calculated cost of the defective cabinet (RUB 1,666.24) is included in the cost of production of products of the same name (cabinets).

The volume and cost of production, including defective products, can be analyzed using the “Product Output (Cost Estimation)” report:

Accounting

In accordance with the instructions for using the Chart of Accounts for accounting the financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n (hereinafter referred to as the Instructions), account 28 is used to account for losses from defects in production, including from internal final defects "Defects in production."

Analytical accounting on account 28 is carried out for individual structural divisions, types of products, expense items, reasons and culprits of the defect. Costs for identified internal defects are reflected in the debit of account 28. In the situation under consideration, such costs include the cost of unfinished products recognized as irreparable defects.

According to the Instructions, amounts attributed to the reduction of losses from defects (for example, amounts to be withheld from those responsible for the defects), as well as amounts written off to production costs as losses from defects, are reflected in the credit of account 28.

Let us note that non-refundable amounts of losses from defects are recognized for accounting purposes as expenses for ordinary activities (clause 5 of PBU 10/99 “Expenses of the organization”). In this case, losses from defects are included in the costs of the production (accounts 20 “Main production”, 23 “Auxiliary production”, 29 “Service production and facilities”), in the process of which the defect occurred. The specified operation to write off non-reimbursable losses from defects is carried out at the end of each month. As a rule, account 28 has no balance at the end of the month.

Clause 99 of the Regulations states that the amounts of non-reimbursable losses from defects are included in the cost of the product or type of work for which a defect is detected. In most cases, the inclusion of losses from defective products in the cost of work in progress is not allowed. An exception is for individual and small-scale production, provided that these losses relate to a specific order that has not been completed in production.

Taking into account the above, when accounting for internal final defects, the following entries are generated in accounting:

Debit 28 Credit 20

— the cost of products recognized as final defects is included in the cost of defects.

If an employee is identified who has committed a defect during the production process, then the cost of defective products can be charged to his account in the manner prescribed by labor legislation (Articles 238, 246-248 of the Labor Code of the Russian Federation):

Debit 73 “Settlements with personnel for other operations” Credit 28

— the cost of defective products is charged to the account of the guilty employee.

At the end of the month, non-reimbursable losses from defects (account 28 balance) are reflected in accounting as follows:

Debit 20 Credit 28

— non-reimbursable losses from defects are included in the costs of the main production;

Debit 43 “Finished products” Credit 20

— non-refundable losses from defects are included in the cost of products of good quality produced in the reporting month.