Account 91 in accounting

A complete list of other income and expenses can be studied in the order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n.

The “Other income and expenses” account is active-passive. The credit of the account reflects the receipt, and the debit records the expense:

The main subaccounts for 91 accounts are presented in the figure:

The purpose of analytical accounting for 91 accounts is to provide the ability to determine the financial result based on each type of income and expense. Consequently, when classifying income and expenses, it is necessary to take into account the homogeneous type of costs to ensure the possibility of determining the financial result for each operation of the same type.

For example, amounts under the article “Fines and penalties for contractual obligations” can be attributed to both expenses and income, therefore, the financial result under this article can be analyzed. Or, by analyzing the expense item for paying for the services of credit institutions, the enterprise will be able to see the effectiveness of working with the bank, whether the bank’s “products” are beneficial to the enterprise.

Which accounts are involved in accounting entries for accounting for deposit transactions?

The deposit account refers to the so-called special accounts in the bank, for the accounting of which account 55 is intended in the accounting department. The Chart of Accounts (approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, as amended on November 8, 2010) provides for several sub-accounts for this account. Deposits are accounted for in subaccount 55.3 “Deposit accounts”.

Since deposits are recognized as financial investments in accordance with clause 3 of PBU 19/02, they can also be taken into account in account 58 “Financial investments” by opening the corresponding sub-account.

The organization establishes the method of accounting for the movement of money on deposit in its accounting policy.

Accounts 55 and 58 are active, so an increase in funds on deposit will be by debit, and a decrease in the deposit account or returned to the owner to the current account will be by credit.

As for the entries on the receipt of interest on the current account and, accordingly, their accrual, account 91 “Other income and expenses” will be involved in them. Subaccount 1 to this account “Other income” is intended to reflect various income, including interest received, from activities not related to the main one.

Why is account 91 needed?

The result of a business is profit or loss. Companies spend and receive money not only in their core activities: there are other sources of income and directions of payments. For example, a manufacturer can make money by selling leftover raw materials, or a trading company can rent out warehouses. And among the expenses of almost every business is the maintenance of a current account. All this is other income and expenses.

More examples in the table:

| Other income | other expenses |

|

|

It is important that the list does not include revenues and expenses that have become extraordinary.

Account accounting is regulated by PBU 9/99 and PBU 10/99. According to them, the account reflects two types of income and expenses:

- operational - related to economic activity, but not its purpose;

- non-realization - follow from economic activity.

General provisions for accounting for other income and expenses

Accounting for other income and expenses is regulated by PBU 9/99 and PBU 10/99, which present:

- an open list of types of other income and expenses (clause 7 of PBU 9/99, clause 11 of PBU 10/99);

- the procedure for determining the amount of other income and expenses (clause 10 of PBU 9/99, clause 14 of PBU 10/99);

- procedure for recognizing other income and expenses in accounting (clauses 12–16 PBU 9/99, clauses 16-18 PBU 10/99).

The principles of drawing up entries for accounting of other income and expenses are regulated in the chart of accounts (Order of the Ministry of Finance of Russia dated October 30, 2000 No. 94n).

To make it easier to navigate the instructions of PBU 9/99, PBU 10/99 and the chart of accounts, we suggest that you familiarize yourself with 2 visual tables: “Accounting for other income” and “Accounting for other expenses”.

In them, opposite a separate type of income (expense), you can see:

- entries reflecting the amount of income (expense) in accounting;

- date of entry of income (expense) into accounting;

- the procedure for determining the amount of income (expense) in accounting.

Account 02 Depreciation of fixed assets

Depreciation of fixed assets can be calculated in the following ways:

- in a linear way;

- reducing balance method;

- the method of writing off the cost by the sum of the numbers of years of useful life;

- by writing off the cost in proportion to the volume of products (works).

The chosen method is fixed in the accounting policy. You can use different depreciation methods for different groups of homogeneous fixed assets.

Depreciation is accrued monthly starting from the month following the one in which the property was accepted for accounting as a fixed asset.

The amounts of accrued depreciation are written off as expenses for ordinary activities, these are:

Debit 20,23,25,26,29 - Credit 02.

Or included in other expenses (if the object is of a non-production nature or is intended for rental, if renting is not a regular type of activity):

Debit 91-2 - Credit 02.

If a fixed asset is used to create, modernize or reconstruct another non-current asset, then:

Debit 08 - Credit 02.

Postings to display profits and losses on account 99

In general, the accounting entry for making a profit or incurring losses in account 99 is as follows:

- Dt99 – Kt84 – retained earnings are taken into account;

- Dt84 – Kt99 – transfer of the amount of net loss;

- Dt99 – Dt90 – write-off of losses for the leading type of activity;

- Dt90 – Kt99 – reflection of profit for the leading type of activity;

- Dt99 – Kt91 – display of losses from other types of activities;

- Dt91 – Kt99 – receipt of income from other types of activities;

- Dt96 – Kt99 – increase in profit due to the balance of unused reserves;

- Dt99 – Kt10 – write-off of the cost of materials damaged as a result of emergency situations;

- Dt73 – Kt99 – recovery of expenses incurred from those responsible in emergency circumstances;

- Dt99 – Kt68 – calculation of income tax.

Profits and losses from emergency circumstances and situations include cash flows due to fire, flood, nationalization of an enterprise, natural disasters, receipt of insurance compensation, etc.

Reflection of information on account credit 91

Account 91, loan entries are made for the following types of business transactions: income from the sale of fixed production assets, proceeds from the gratuitous receipt of assets (current and non-current), fines received, penalties under agreements with counterparties, exchange rate differences, dividends received from participation in other partnerships, income from the provision of loans, advances, proceeds from the sale of intangible assets, innovative developments, amounts of overdue debt to creditors, etc.

Typical transactions on 91 accounts

Account 91 may reflect income and expenses from operations not related to the main activities of the enterprise, in particular:

- Subaccount 91.01 - income from rent, transfer of rights to intellectual property, participation in the authorized capital of other organizations, etc.;

- Subaccount 91.02 - expenses for interest on loans, maintenance of fixed assets for conservation, fines, penalties, etc.

When reflecting the main transactions for other income, the following entries can be used:

Expenses for non-core activities of an enterprise can be taken into account as follows:

What do other income and expenses include?

On the account 91 takes into account other income and expenses.

Other income is income not related to the normal activities of the organization. What does other income include?

Other income includes:

- income from the rental of fixed assets and intangible assets;

- dividends from contributions to the authorized capital of other organizations;

- interest on securities;

- proceeds from the sale of fixed assets, materials (if this is not a normal activity of the organization);

- fines, penalties, penalties received from counterparties;

- assets received free of charge;

- income received in the form of compensation for losses caused to the organization;

- profits from previous years revealed in the current year;

- expired accounts payable;

- exchange rate differences from foreign exchange transactions;

- revaluation of assets.

Other income also includes other income. This issue will be discussed in more detail in the near future, when we move on to the topic of taxation.

Other expenses are expenses of an organization that are not related to the normal activities of the organization.

What do other expenses include?

Other expenses include

- expenses associated with leasing assets;

- related to participation in the authorized capital of other organizations;

- related to the write-off, sale and disposal of fixed assets, intangible assets, materials;

- interest on loans, borrowings;

- payment for bank services;

- contributions to reserves;

- paid fines, penalties, penalties;

- compensation for damages caused;

- losses from previous years;

- expired accounts receivable;

- exchange rate differences from foreign exchange transactions;

- asset write-down;

- charitable expenses;

- other expenses.

They are divided into operational and non-operating.

I note that income and expenses arising as a result of emergency situations are not taken into account in this account, but are credited directly to the account. 99 "Profits and losses."

| Buy ★ bestselling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8000 books purchased |

Account 91 - active or passive

Account 91 belongs to the category of mixed, or active-passive. It simultaneously takes into account both assets and liabilities. And its balance is changeable - it can only be debit or only credit.

On credit 91 accounts during the month reflect income from other sources, and on debit - other expenses. At the end of the month, the debit and credit turnovers are compared, the smaller is subtracted from the larger and the result is obtained. If the balance turns out to be a credit balance, income exceeds expenses, and the company generates profit from other activities. If it's the other way around, it's a loss.

There should be no balance left in the account at the end of each month. It is written off to the Profit and Loss account.

Account details 91

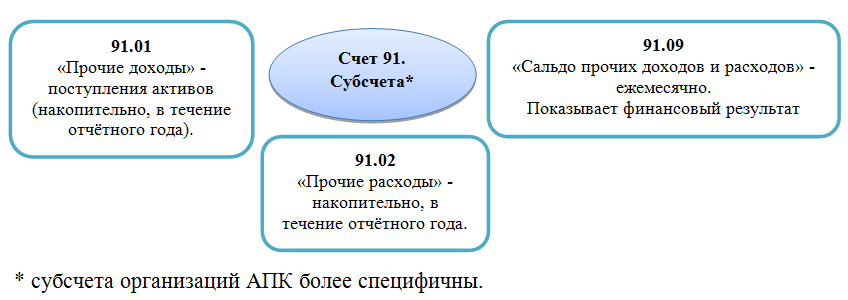

For additional detailing of analytical accounting for business operations from other types of activities, the opening of special sub-accounts is provided:

- 91-1 “Other income” (PD);

- 91-2 “Other expenses” (PR);

- 91-3 “VAT”;

- 91-9 “Balance of other income and expenses.”

Please note that, taking into account the specifics of the company’s activities, additional sub-accounts may be opened. So, for example, you can further detail account 91-2 by type of other expenses. However, such a decision must be fixed in the accounting policies of the organization.

Reflection in accounting

Account 91 is intended to reflect other, non-operating, operating expenses and income in the organization's accounting. The entire period preceding the annual report, other expenses and income of the organization are accumulated in active-passive accounting accounts, which in the chart of accounts (unified) of accounting is called “Other income and expenses ” . At the same time, the correspondence of account 91 depends on the item of expense and (or) income; analytical accounting should, based on the accounting policy of the organization, be carried out for each item separately, this will significantly simplify the analysis of the composition of the indicator when assessing the result of the enterprise. The following subaccounts must be opened for this account:

— 91/1 “Other income” — intended to reflect all types (except extraordinary) of an enterprise’s income not related to its main activities.

— 91/2 “Other expenses” — this subaccount reflects other, non-current, operating expenses.

— 91/9 “Balance of other income and expenses” — account 91 is closed through this subaccount.

Analytical accounting

Analytical accounting for 91 accounts has two tasks:

- Provide the opportunity to determine the financial result for each operation;

- Divide income and expenses into operating and non-operating to simplify the preparation of a report on financial results.

The chart of accounts provides three subaccounts to accounting account 91:

- 91-1 - other income;

- 91-2 - other expenses;

- 91-9 - balance.

Example . Bely Oak LLC paused production during the coronavirus crisis and decided to rent out the machine to earn extra money. Monthly rent payment is 21,000 rubles, including VAT 3,500 rubles. Depreciation - 3,000 rubles per month. The White Oak accountant will record the following transactions on a monthly basis:

- Dt 62 Kt 91.01 - 21,000 rubles - payment received from the tenant.

- Dt 91.02 Kt 68 - 3,500 rubles - tax charged on rental payment.

- Dt 91.02 Kt 02 - 3,000 rubles - depreciation of the machine has been accrued.

- Dt 51 Kt 62 - 21,000 rubles - the money was credited to the account.

But three subaccounts are not enough to effectively manage an organization and conveniently prepare accounting records. More detailed information is needed about groups and types of income and expenses.

The second option is to open sub-accounts within the following groups:

- 91-1 - operating income;

- 91-2 - operating expenses;

- 91-3 - non-operating income;

- 91-4 - non-operating expenses;

- 91-9 - balance.

You can open additional subaccounts for each of the groups in order to link the indicators of the financial results report with the subaccounts. For example, among operating income, highlight interest, income from participation in other companies and other income.

Other income and expenses in accounting

Other income and expenses, as a general rule, are reflected in account 91. Income is accounted for on the credit side of account 91, and expenses - on the debit side. To account for them, first-order subaccounts are opened:

- 91.1 – for accounting of income;

- 91.2 – for cost accounting.

Entries for subaccounts 91.1 and 91.2 are made by the accountant cumulatively throughout the reporting period. At the end of the month, the difference between other income and costs is displayed, which is recorded in subaccount 91.9: the debit shows the loss, and the credit shows the profit.

IMPORTANT! Analytical accounting should provide the ability to identify financial results for each operation.

Read about the nuances of accounting for other income and expenses here. And you will find the main entries for accounting for other expenses in K+:

Trial access to the legal system is free.

To break down costs and income into operating, non-operating and emergency companies, they have the right to independently develop a chart of accounts, approving it in a local act, or use industry charts of accounts, for example, for enterprises of the agro-industrial complex (AIC). The chart of accounts for agricultural companies was approved by Order of the Ministry of Agriculture dated June 13, 2001 No. 654 and allows medium and large companies to record other income and expenses using the following subaccounts:

- 91.1 – operating income;

- 91.2 – operating expenses;

- 91.3 – non-operating income;

- 91.4 – non-operating expenses;

- 91.9 – balance of other income and expenses.

The final balance of subaccount 91.9 in any case is closed monthly to account 99 “Profit/Loss”, as a result of which account 91 has no residual balance as of the reporting date.

Other operating expenses are reflected in subaccount 91.2.

Read about the procedure and principles for accounting for income and expenses in an organization here.

Correspondence of account 91 with other accounting accounts

Almost any activity of the organization can become a source of other income and expenses, therefore the number of corresponding accounts is almost equal to the number of accounts in the plan. We have collected all the numbers in a table.

| Only by debit | Only on loan |

| 01 02 03 04 07 08 10 11 14 15 16 19 20 21 23 28 29 58 59 60 63 66 67 68 69 70 71 73 76 79 81 94 98 99 | 07 08 10 11 14 15 20 21 23 28 29 41 43 45 50 51 52 55 57 58 59 60 63 66 67 62 71 73 75 76 79 81 96 98 99 |

How can 1C help an accountant?

Automation of final operations significantly saves time when compiling reports. Therefore, 1C.8 versions 2.0 and 3.0 provide for a whole cycle of regulatory operations. They must be carried out gradually, strictly in the sequence in which they were conceived.

Important point! Violation of the sequence of routine operations leads to incorrect data in analytical reports. We must remember that some of the operations are interconnected. It is impossible to calculate profit if cost accounts are not reset.

Regular operations are located in the “Accounting, Taxes and Reporting” menu, “Period Closing” section, “Month Closing” subsection. Here in the third stage you can see “Closing 90, 91 accounts”.

This processing deals with zeroing the required account. 91, just like other accounts, is not closed if there are errors. Incomplete cost items and other analytical sub-contos may result in the transaction being rejected. You can learn more about how the operation works from the video:

Empty subcontos form negative balances in analytics, which confuse the balance sheet, leading movements into chaos. Therefore, it is necessary to fill out the analytics very carefully and thoughtfully, entering primary operations in the program.

Standard operations with 91 accounts

Transactions on 91 accounts are related to income and expenses. Receipts are reflected in the credit of the account. Let's look at typical operations:

| Wiring | The essence of the operation |

| Dt 41 Kt 91-1 | During the inventory, unaccounted for goods were found. |

| Dt 63 Kt 91-1 | The balance of the reserve for doubtful debts was written off. |

| Dt 51 Kt 91-1 | Rent was received for the fixed asset provided for temporary use. |

| Dt 51 Kt 91-1 | Interest received on the loan issued. |

| Dt 60 Kt 91-1 | The amount of the creditor for which the statute of limitations has expired is reflected. |

| Dt 62 Kt 91-1 | Income was received from the sale of a fixed asset. |

| Dt 98 Kt 91-1 | The assets were received free of charge. |

| Dt 99 Kt 91 | Write-off of balance. |

Accounting entries related to other expenses:

| Wiring | The essence of the operation |

| Dt 91-2 Kt 01 | The residual value of the retired fixed asset is written off. |

| Dt 91-2 Kt 02 | Depreciation has been calculated on leased fixed assets. |

| Dt 91-2 Kt 10 | The actual cost of materials donated to another company was written off. |

| Dt 91-2 Kt 14 | A reserve has been created to reduce the cost of the MC. |

| Dt 91-2 Kt 60 | Write-off of receivables that are unrealistic for collection. |

| Dt 91-2 Kt 66 | Interest paid on the loan. |

| Dt 91-2 Kt 51 | A penalty under the contract was recognized as payable. |

| Dt 91-2 Kt 94 | A shortage in excess of the norm is reflected, there are no culprits. |

Kontur.Accounting will help you maintain your accounting records. The service determines income and expenses in accordance with the Tax Code of the Russian Federation and takes into account when to recognize them. Keep records, pay salaries and submit reports via the Internet. Anyone who registers with Accounting for the first time receives a 14-day trial period.

Document flow for account 91

Postings for 91 accounts are compiled on the basis of well-formed primary documents, which are filled out by the accounting department, respectively, for each specific type of expense and income. The following types of documents are used:

- An accounting certificate is used when crediting reserves of unused payments to income (operating, non-operating, other), calculating deviations in the value of registered inventory items, and amounts of deferred income.

- An invoice is used when calculating interest on credits, loans, borrowings, income from participation in the share capital (authorized capital) of a third enterprise, income from ownership of securities.

- The inventory list, expenses and income on the basis of this document are carried out on account 91 in correspondence with active accounts for accounting for inventory, finished goods, cost accounts of the main and auxiliary production.

- The act of acceptance and transfer of fixed non-current assets when writing off the residual value of sold or written off non-current assets.

- The calculated depreciation sheet is used to write off depreciation accrued on fixed assets that are leased.