KBK for personal income tax payment

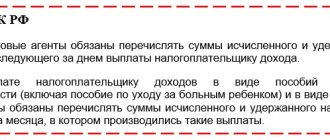

In a situation where the income is wages, the state takes the tax on it not from the employee after accrual, but from the tax agent - the employer, who will issue the employee a salary with taxes already paid to the budget.

Personal income tax is calculated by subtracting documented expenses from the amount of income of individuals and taking a certain percentage of this amount (tax rate). Personal income tax is assessed separately for residents and non-residents of the Russian Federation, but this does not apply to employees. Some income specified in the legislative act is not subject to taxation (for example, inheritance, sale of real estate older than 3 years, gifts from close relatives, etc.) The income declaration gives individuals the right to certain tax deductions.

What do personal income tax payers need to know about KBK?

For 2021, the budget classification codes for paying income tax for employees have not changed. Thus, the BCC, which were approved by Order of the Ministry of Finance No. 65n dated July 1, 2013 (as amended) remain relevant. Personal income tax at an increased rate for income over 5,000,000 rubles is sent to the KBK specified in the order of the Ministry of Finance dated 06/06/2019 No. 85n, dated 10/12/2020 No. 236n, dated 12/07/2020 No. 297n.

Let’s say right away that tax deductions for individuals in 2021 will be made to various BCCs, depending on:

- type of payment;

- taxpayer status.

Budget classification codes will not differ when paying for employees who work under a contract, regardless of whether the employees are residents or not.

As already noted, codes differ by type of payment. In the table below we have presented the BCC for personal income tax payment in 2021 for incomes less than 5,000,000 rubles;

| Individual entrepreneurs on OSNO, notaries, lawyers | KBK for personal income tax | Legal entities (organizations) - tax agents | KBK for personal income tax |

| Personal income tax payment | 182 1 01 02020 01 1000 110 | Personal income tax payment | 182 1 01 02010 01 1000 110 |

| Penalties for personal income tax | 182 1 01 02020 01 2100 110 | Penalties for personal income tax | 182 1 01 02010 01 2100 110 |

| Personal income tax fines | 182 1 01 02020 01 3000 110 | Personal income tax fines | 182 1 01 02010 01 3000 110 |

When generating a payment order for the payment of income tax from employees, do not forget to check whether you have correctly indicated the BCC for personal income tax in 2021. An incorrectly specified code can lead to unwanted costs and claims from the Federal Tax Service due to failure to receive payment on time.

Personal income tax on dividends in 2021 rate and BCC

So, first of all, let’s look at the budget codes that must be indicated when issuing payment orders for paying taxes on dividends. BCC for personal income tax on dividends in 2021 is 182 1 01 02021 01 1000 110, and for income tax on dividends 182 1 01 02021 01 1000 110. As for the interest rate, it is 15% for non-residents. But for Russians themselves, as well as foreign citizens who have stayed in Russia for more than 183 days and have a residence permit, the personal income tax rate on dividends in 2021 is only 13%.

Personal income tax on dividends in 2021 rate, KBK (budget classification code), for residents and non-residents, payment order, how to pay and complete information on paying income tax.

How many business projects are born in a cafe over a glass, when a person with organizational skills and ideas scams his friend out of money to open a business. The latter hopes to receive a substantial sum, called dividends, for the rest of his life. It should be noted that there are very few enterprises in Russia that pay dividends to their founders, because it is much easier to register a person as a freelance employee and pay him a salary, with all taxes, without having to add extra reporting. Enterprises try not to show excess profits, but by updating fixed assets and assets, as well as creating additional expenses, reduce them to zero. However, some firms still pay income to their founders. Accordingly, according to the law, this income must be subject to tax, the level of which is constantly changing.

Personal income tax payment from dividends 2021 sample filling

Payment of the tax must be made no later than one working day following the day the income is issued (Clause 6, Article 226 of the Tax Code of the Russian Federation). An exception is made for vacation pay and sick leave: tax on them must be paid no later than the last day of the month in which the employee was given the appropriate funds.

- If you have calculated the penalties yourself and pay them voluntarily. In this case, the basis will have a tax code, that is, voluntary repayment of debt for expired tax periods in the absence of a requirement from the Federal Tax Service.

- If you pay at the request of the Federal Tax Service. In this case, the base will have the form TP.

- You transfer based on the inspection report. This is the basis of payment to AP.

In the case when an organization is created on the basis of authorized capital, it must periodically share its income with those who founded it, as well as shareholders. Actually, dividends are those funds that remain after paying taxes, insurance premiums, salaries and other things. They are the income of shareholders who, through the purchase of shares, invested in the enterprise, and can now receive the part of the profit they deserve.

It is not necessary to endorse this document with a seal, since the signatures placed under the document are sufficient. But if the legal acts of the enterprise themselves contain a mandatory condition for placing a seal on such a document, then this should be implemented.

Below we present in the table the current main BCCs for 2021 for income tax.

| TYPE OF NDFL | KBK IN 2021 |

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fines on employee income | 182 1 0100 110 |

| Tax paid by individual entrepreneurs on the general taxation system | 182 1 0100 110 |

| Penalties for personal income tax paid by individual entrepreneurs on the general system | 182 1 0100 110 |

| Penalties for personal income tax paid by individual entrepreneurs on the general system | 182 1 0100 110 |

Foreign organizations and individuals will be able to indicate “0” in the “TIN of the payer” field if they are not registered with the tax office. An exception is payments administered by tax authorities. The amendment comes into force on January 1, 2021.

When deducting money from the income of an individual debtor to pay off the debt, indicate his TIN in the “TIN of the payer” field. It is no longer possible to enter an organization’s TIN from July 17, 2021.

If a payment order was drawn up by an individual without an account and intends to transfer money to the budget using it, the details must indicate the individual’s tax identification number or “0” if the number has not been assigned. It is prohibited to indicate the TIN of a credit institution. This rule is effective from October 1, 2021.

The main change concerns individual entrepreneurs, notaries, lawyers and heads of peasant farms. From October 1, 2021, payer status codes “09”, “10”, “11” and “12” will no longer be valid. Instead, the taxpayers listed above will indicate code “13,” which corresponds to individual taxpayers.

Also, some of the codes will be deleted or edited. New codes will be added:

- “29” - for politicians who transfer money to the budget from special election accounts and special referendum fund accounts (except for payments administered by the tax office);

- “30” - for foreign persons who are not registered with the Russian tax authorities, when paying payments administered by customs authorities.

From October 1, the list of payment basis codes will decrease. Codes will disappear:

- “TR” - repayment of debt at the request of the tax authorities;

- “AP” - repayment of debt according to the inspection report;

- “PR” - debt repayment based on a decision to suspend collection;

- "AR" - repayment of debt under a writ of execution.

Instead, you will need to indicate the code “ZD” - repayment of debt for expired periods, including voluntary. Previously, this code was used exclusively for voluntary debt closure.

Also, from October 1, the code “BF” will be removed - the current payment of an individual paid from his own account.

This field indicates the document number that is the basis for the payment. Its completion depends on how field 106 is filled in.

The new code for the basis of payment in the four invalid cases is “ZD”. But despite this, the deleted codes will appear as part of the document number - the first two characters. Fill out the field in the following order:

- “TR0000000000000”—number of the tax office’s request for payment of taxes, fees, and contributions;

- “AP0000000000000” - number of the decision to prosecute for committing a tax offense or to refuse to prosecute;

- “PR0000000000000” - number of the decision to suspend collection;

- “AR0000000000000” – number of the executive document.

For example, “TR0000000000237” - tax payment requirement No. 237.

The procedure for filling out field 109 changes to pay off debts for expired periods. When specifying the “ZD” code, you need to enter in the field the date of one of the documents that is the basis for the payment:

- tax requirements;

- decisions to prosecute for committing a tax offense or to refuse to prosecute;

- decisions to suspend collection;

- writ of execution and initiated enforcement proceedings.

Error:

An individual independently pays personal income tax to the budget on the dividends he receives. At the same time, in the payment order he indicates KBK 182 1 0100 110.

This budget classification code is used only in cases where personal income tax on dividends is paid by a legal entity acting as a tax agent for an individual. When an individual independently transfers funds to the budget to pay personal income tax, KBK 182 1 0100 110 is used.

Error:

The accountant believes that it is impossible to clarify the personal income tax payment on dividends sent using the old KBK.

In fact, it is necessary to submit an application to clarify the tax payment to the budget. This helps to avoid arrears.

KBK for personal income tax on dividends in 2021

Dividends are accrued to the participants of the organization due to the fact that it has retained earnings. That is, one that is not required to pay expenses, as well as to establish and maintain effective business activities.

We recommend reading: How to count on child benefits for a third child in Chuvashia

The profit that individuals receive as a result of equity participation in organizations and companies is called dividends. It is paid directly by organizations to individuals. This situation, along with other payments intended to individuals from organizations, is accompanied by tax payments. One of which is personal income tax. The organization itself has the responsibility to calculate this amount, withhold it from the individual, and also transfer it to the budget - also lies on the shoulders of the tax agent, which this organization is. At the same time, in order to transfer the payment, you will definitely need to know the exact BCC for personal income tax on dividends in 2021.

Personal income tax rate on dividends in 2021

It is necessary to pay attention to the fact that in the process of determining the amount of tax on accrued dividends of resident founders, one must take into account whether the legal entity itself received a share of payments from another company in the current or previous reporting tax period.

Initially, it is necessary to pay attention to the payment of personal income tax by entrepreneurs under the simplified tax system. I do not take into account the fact that when using the simplified taxation regime, companies are exempt from accounting; when dividends are accrued to participants in the authorized capital, an obligation is automatically formed.

KBK for payment of personal income tax on dividends in 2021

Profit is divided between participants in accordance with the procedure reflected in the charter of the legal entity. Most often this distribution is made in proportion to the share of participation. Newly admitted participants can also count on payment of dividends according to their available share.

The profit received by the enterprise after taxation can be distributed among the participants of the company. Dividends recognize not only income from the distribution of remaining profits received by the participant, but also other similar payments to the participants (letter of the Ministry of Finance of the Russian Federation dated May 14, 2021 No. 03-03-10/27550). Dividends are also recognized as receipts outside the Russian Federation, recognized as such by the legislation of other countries (Clause 1, Article 43 of the Tax Code of the Russian Federation).

KBK for personal income tax on dividends in 2021: sample payment order

When a company passes through many payments with different budget classification codes, it is very easy to make a mistake in writing the BCC for personal income tax on dividends. Fortunately, the error can be corrected without significant damage to the organization if the right steps are taken.

In December 2021, the company received and distributed profit in the amount of RUB 200,000. Now you need to calculate personal income tax on dividends. Since both company participants are residents of the Russian Federation, a 13% rate is applied to their income.

Reasons for changing the BCC in the Russian Federation

Every accountant knows that in order to make a payment correctly, be it taxes, contributions or penalties, it is important to enter the correct budget classification code. Therefore, it is necessary to update the database of new codes, since the old ones will become invalid, and payments made using them will be returned to the sender or will be regarded as unclear. Such a development of events is fraught with the accrual of penalties and the application of fines .

There are no small things in life, especially when it comes to finances and paperwork. To avoid administrative penalties and other troubles, you should carefully study the changes in the maintenance of documentation on fees for income for employees and the transfer of deductions for 2021. We will talk about the nuances associated with wages, sick pay, vacation pay and travel allowances.

CBC personal income tax on non-resident dividends in 2021 in Russia

Russian companies are considered tax agents for dividend income of participants - individuals, therefore they withhold and transfer tax to the budget. To make the payment correctly, the accountant of a JSC or LLC needs to follow the following algorithm.

We recommend reading: Unified register of pledged property

If organizations (LLC or JSC) pay dividends to their participants (founders or shareholders) based on the results of their activities, then they are required to withhold income tax from this amount. In the article, we will consider at what rate personal income tax should be withheld from dividends in 2021 and when to transfer the tax to the budget.

Transfer deadlines

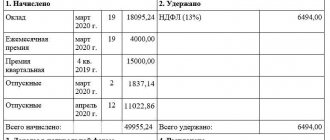

As a general rule, personal income tax is paid no later than the day following the date of transfer of wages to employees. For example, the accountant closed the salary for March 2021 on 03/31/2021. The funds were paid to employees on 04/05/2021, which means that personal income tax is withheld on 04/05/2021 and transferred to the budget until 04/06/2021.

When it comes to calculating vacation pay or various types of benefits (for temporary disability, caring for a sick child), different rules apply. The tax must be transferred to the budget system of the Russian Federation before the end (last day) of the month in which accrual and payment for vacation or sick leave were made, indicating the BCC for personal income tax in 2021 in the payment order. That is, if an employee goes on vacation from 03/22/2021, vacation pay was transferred to him along with an advance payment on 03/15/2021. Accordingly, income tax was withheld on March 15 and transferred until March 31, 2021.

Please note that you can use a special online calculator to calculate the income tax.

KBK for personal income tax in 2021: table

After the budget receives personal income tax transferred by tax agents, these funds are distributed between the budget of the constituent entity of the Russian Federation and the budgets of municipalities (settlements, municipal districts, urban districts) according to the standards established by budget legislation.

What budget classification codes for personal income tax have been approved for 2021? Which BCCs should I pay personal income tax on salaries, vacation pay and other payments in 2021? Here is a convenient table with the BCC for personal income tax for 2021 (for legal entities). Also in the article you can see a sample payment order for personal income tax payment.

How to fill out a payment order for taxes and contributions in 2021

As mentioned above, in accordance with the Tax Code, tax on dividends must be paid in full, and the deduction rules do not apply to it. Those. In any case, the organization is obliged to transfer a fiscal contribution to the budget.

An error in a payment order from KBK for personal income tax automatically leads to the fact that the money will not be transferred to the required address. That is, the Federal Tax Service will consider you a debtor for this tax. In a situation where it belongs to a group of residents, the personal income tax rate is 13%; if it does not belong to a group of residents, it is 15%.

- funds balance;

- minutes of the general meeting of founders (shareholders) or the founder’s decision on payment;

- an order signed by all responsible persons, i.e. the head of the company, accountant;

- a report on profits and losses for the year;

- and another statement of capital flows and all cash flows during the year;

- appendix to the balance sheet and explanatory note.

faces. Withholding of personal income tax is carried out separately for all individuals and is reflected in special calculation documents. In 2021, the tax rate on dividends received for resident individuals (those who were in the Russian Federation for at least 183 days per year) is 13% , for non-resident individuals this rate is slightly higher and amounts to 15%. The appropriate tax status of the recipients of funds is determined at the time of each payment.

Features of determining the tax base for income received from equity participation in other organizations Examples of calculation To understand the features of calculating personal income tax on dividends, you need to familiarize yourself with the following typical example. for 2021 I received a net profit of 500,000 rubles. This directly points to the fact that the responsibilities for calculating, withholding and remitting tax are assigned to the organization, and not to its participants. If the established deadlines for withholding personal income tax on the amounts in question are missed, the organization may be subject to a certain fine by the regulatory authorities.

Budget classification codes change regularly. Thus, from 2021, the document establishing the BCC for tax payments has been completely updated. That is why, in order to avoid accidental errors, it is better to generate payments automatically - in the BukhSoft program.

That is, personal income tax from dividends is transferred to the same KBK as from other payments to employees (salaries, etc.). If the recipient of “dividend” income is an individual, the tax is transferred to a separate BCC: 182 1 0100 110.

Dividends are profits that enterprises receive as a result of equity participation in companies and organizations. It is paid to both legal entities and individuals. It is subject to personal income tax. To transfer the mandatory payment, budget classification codes are provided.

Article 230. Ensuring compliance with the provisions of this chapter Tax service specialists provide clear explanations that tax agents carrying out transactions with shares and other specialized instruments cannot be subject to the general procedure for providing information on the income of individuals to the inspectorate in the format of certificates in Form 2 -NDFL.

\r\n\r\n

A clear rule will come into effect in the event that the accounting department deducts money from an employee’s salary to pay off debts to the budget. Next, the withheld amount is transferred to the treasury by a separate payment order. In such a payment in the field “TIN of the payer”, from July 17, 2021, it is strictly prohibited to indicate the identification number of the employing company. Instead, you need to put the TIN of the employee himself (amendments made by Order No. 199n).

\r\n\r\n

\r\n\r\n

There are innovations for individuals who pay taxes, fees, insurance and other payments administered by the tax authorities. The changes concern field 101 (the status of the payment originator is entered in it).

\r\n\r\n

Until October 2021, when filling out field 101, these individuals must select one of the following values:

\r\n\r\n

- \r\n\t

- “09” - individual entrepreneur who pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “10” - a notary engaged in private practice, paying taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “11” - a lawyer who has established a law office that pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “12” is the head of a peasant (farm) enterprise who pays taxes, fees, insurance premiums and other payments administered by the tax authorities.

- “13” is an “ordinary” individual.

\r\n\t

\r\n\t

\r\n\t

\r\n\t

\r\n

\r\n\r\n

Starting in October 2021, the values "09", "10", "11" and "12" will be removed. Instead, the value remains, the same for all individuals (“ordinary”, individual entrepreneurs, lawyers, etc.) - “13”. Changes were made by order No. 199n.

When filling out the recipient's details, you need to take into account changes in two fields. Innovations are associated with the transition to a new treasury service and treasury payment system.

- Field 17: the account number of the territorial body of the Federal Treasury (TOFK) is changed;

- Field 15: starting from January 2021, it is necessary to indicate the account number of the recipient's bank (the number of the bank account included in the single treasury account (STA)). In 2021 and earlier, this field was not filled in when paying taxes and contributions.

A clear rule will come into effect in the event that the accounting department deducts money from an employee’s salary to pay off debts to the budget. Next, the withheld amount is transferred to the treasury by a separate payment order. In such a payment in the field “TIN of the payer”, from July 17, 2021, it is strictly prohibited to indicate the identification number of the employing company. Instead, you need to put the TIN of the employee himself (amendments made by Order No. 199n).

Until October 2021, in payments issued when repaying debts for expired periods, in field 106 you can, if necessary, specify one of the following values:

- “TR” - repayment of debt at the request of the tax authority to pay taxes (fees, insurance contributions);

There are innovations for individuals who pay taxes, fees, insurance and other payments administered by the tax authorities. The changes concern field 101 (the status of the payment originator is entered in it).

Until October 2021, when filling out field 101, these individuals must select one of the following values:

- “09” - individual entrepreneur who pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “10” - a notary engaged in private practice, paying taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “11” - a lawyer who has established a law office that pays taxes, fees, insurance premiums and other payments administered by the tax authorities;

- “12” is the head of a peasant (farm) enterprise who pays taxes, fees, insurance premiums and other payments administered by the tax authorities.

- “13” is an “ordinary” individual.

Starting in October 2021, the values "09", "10", "11" and "12" will be removed. Instead, the value remains, the same for all individuals (“ordinary”, individual entrepreneurs, lawyers, etc.) - “13”. Changes were made by order No. 199n.

From 01/01/2021, personal income tax payments must be filled out in a new way - the changes concern the introduction of new accounts and clarification of information about taxpayers. To clarify the recipient of the funds - the Federal Treasury, in connection with the transition to a new procedure for treasury services and a new system of treasury payments, the rules for filling out two fields have changed:

- for field 17 - it indicates the new account number of the territorial body of the Federal Treasury (TOFK);

- for field 15 - it indicates the account number of the bank - the recipient of the funds, which is part of the single treasury account - UTS. Until 2021, when paying taxes and contributions, field 15 was left blank.

From 10/01/2021, an updated list should be applied - the purpose of payment when paying personal income tax when repaying debts for previous periods.

Please indicate the amount in full rubles. The rule applies: transfer taxes to the budget in full rubles, rounding kopecks according to the rules of arithmetic: if less than 50 kopecks, discard them, and if more, round to the nearest full ruble.

All fields are required. The date and amount of the write-off are indicated in numbers and in words. Payment orders are numbered in chronological order.

Each field is assigned a separate number. Let's look at the rules in more detail.

Such a payment order has both similarities with a regular one (it states the same status of the payer, indicates the same details of the recipient, the same income administrator), and differences. We will dwell on the latter in more detail, and then we will provide a sample payment slip for penalties for personal income tax.

The first difference is KBK (props 104). For tax penalties, there is a separate budget classification code, in the 14th–17th digits of which the income subtype code is indicated - 2100.

IMPORTANT! KBK for transferring penalties: 182 1 0100 110.

The second difference between a payment order for penalties is detail 106. The following options are possible:

- If you have calculated the penalties yourself and pay them voluntarily. In this case, the basis will have a tax code, that is, voluntary repayment of debt for expired tax periods in the absence of a requirement from the Federal Tax Service.

- If you pay at the request of the Federal Tax Service. In this case, the base will have the form TP.

- You transfer based on the inspection report. This is the basis of payment to AP.

The third difference is detail 107. Its value depends on what served as the basis for the payment:

- For voluntary payment – “0”. If you are listing penalties for one specific period (month, quarter), it is worth indicating it, for example, MS.02.2018 - penalties for February 2021.

- When paying at the request of tax authorities (basis of TR) - the period specified in the request.

- When repaying penalties according to the verification report (the basis of the AP), they also put 0.

If you pay penalties yourself, enter 0 in fields 108 and 109.

In all other cases, in field 108, provide the document number - the basis for the payment (for example, claims), do not put the “No” sign in this case.

In field 109, indicate:

- date of requirement of the Federal Tax Service - for the basis of payment TR;

- the date of the decision to bring (refusal to bring) to tax liability - for the basis of an administrative agreement.

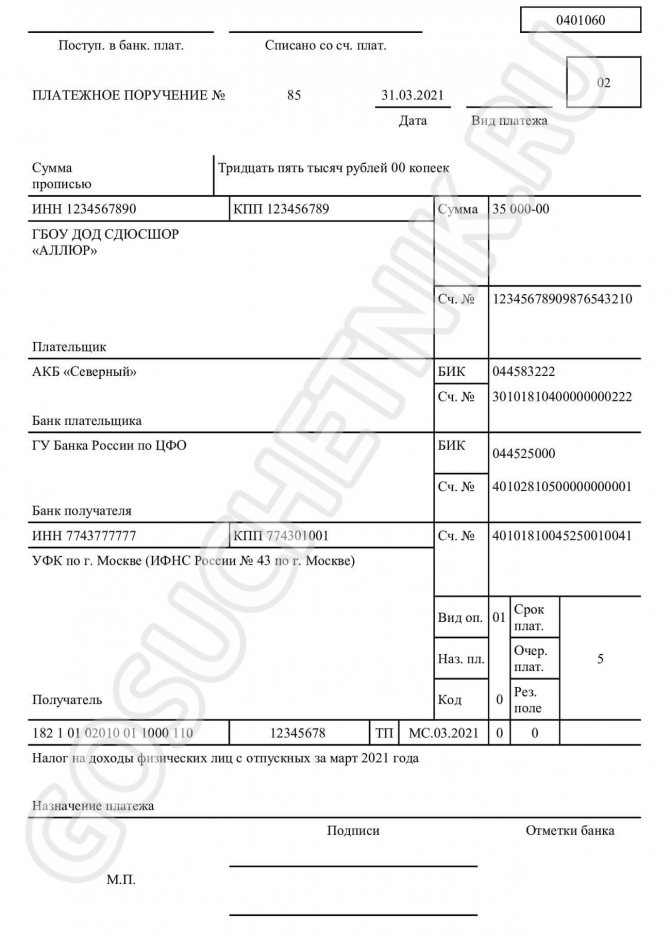

Sample personal income tax payment order in 2021

A payment order is used when transferring funds to another account to pay taxes, pay dividends, wages, etc. Productions that are single or medium-sized in terms of output can issue an order through a bank. Large organizations can generate and send any order via Internet banking.

- Personal income tax penalties from Russian organizations that received dividends from domestic organizations;

- Penalties from foreign organizations that received dividends from Russian ones;

- Penalty for personal income tax from domestic organizations that received dividends from foreign organizations.

Personal income tax rate on dividends in 2021

If a company pays dividends to individuals, it must withhold personal income tax from them. The tax rate can be 13% or 15%. This depends on the status of the income recipient. The tax is calculated using a special formula if the company received dividends from its affiliates. The deadline for paying personal income tax differs for LLCs and JSCs. Also, what kind of reporting needs to be submitted for withheld tax depends on the legal form.

The founders decided to distribute profits for 9 months of 2021. Dole Ivanova S.M. corresponds to an amount of 350,000 rubles. The payment was made on November 1, 2021. Based on the results of the period from November 2021 to October 2021, Ivanov S.M. is a resident. When paying dividends, it is necessary to withhold 45,500 (350,000 x 0.13) rubles.

Formula for calculating penalties for personal income tax in 2019-2020

For each day of delay in transferring personal income tax, penalties (P) are calculated according to the formula (clause 4 of article 75 of the Tax Code of the Russian Federation):

P = Z * S * D where,

- Z – personal income tax amount not paid on time;

- C – interest rate of penalty;

- D – the number of calendar days of delay, which is determined from the day following the due date for tax payment to the day preceding the actual payment of personal income tax.

The interest rate of the penalty depending on the person paying the personal income tax and the number of days of delay is determined as follows:

| Who pays personal income tax | Number of calendar days of delay | |

| Up to 30 days (inclusive) | Over 30 days | |

| Organization | 1/300*R | 1/150*R |

| Individual (including individual entrepreneur) | 1/300*R | |

R is the Central Bank refinancing rate that was in effect during the corresponding period of delay.

KBK personal income tax on dividends in 2021

The tax is paid no later than the day following the day of transfer of dividends. This rule is specified in paragraph 6 of Art. 226 of the Tax Code of the Russian Federation. For example, if the transfer of dividends was made on April 13 (the payment was sent to the bank), the tax must be paid on April 14.

The tax rate is 13%. It has not changed since 2021. If the individual is not a resident of the Russian Federation, the rate increases to 15%. Responsibility for the correctness and timeliness of tax remittance lies with the organization.

Innovations in KBK

There are quite a lot of changes, so you should consider each in more detail:

- The shape has changed. Instead of one sheet, according to the new rules, two . Salary data and deductions with codes are placed on a separate sheet. The right to deduction must be confirmed. Data is entered in a separate field if forms are available.

- The name of the document itself and the application have changed.

- There are also innovations when issuing certificates to employees. There are no significant changes in the uniform for workers. But for the tax office you need to prepare a new sample containing expanded information.

- To fill out the “Characteristic” cell, there are 4 entry options: 1 – normal, 2 – it is not possible to deduct and transfer the tax, 3 – successors of rights, 4 – tax is not transferred to heirs of rights (gifts over 4 thousand rubles)

- Calculation for 2021 should be submitted in extended form .

- The limit on the number of copies provided has been lifted.

- The paper copy must be filled in with black or blue ink. Corrections and blots are not allowed. Documents with compromised integrity are not allowed to be submitted.

- BCC for personal income tax remains unchanged.

On January 1, 2021, a new KBK 182 1 01 02080 01 1000 110 , which is intended for transferring personal income tax to the budget from the amount of income of an individual in the amount of over 5 million rubles . The personal income tax rate on such income is set at 15%.

Separately, we should consider non-standard payments that are taxed and the payment terms for them:

- Material assistance that is not social assistance guaranteed by the state. This payment is taxed at the normal rate. The withheld funds should be transferred to the tax office the next day.

- Gifts indicated in the accounting exceeding the amount of 4 thousand rubles. , are taxed at a rate of 13% . In addition, such gifts are subject to mandatory inclusion in the declaration. The retained interest must be paid no later than the next day.

Table with KBK for 2021 for personal income tax

| Type of personal income tax | KBK in 2021 |

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties for personal income tax on employee income | 182 1 0100 110 |

| Personal income tax fines on employee income | 182 1 0100 110 |

| Tax paid by individual entrepreneurs on the general taxation system | 182 1 0100 110 |

| Penalties for personal income tax paid by individual entrepreneurs on the general system | 182 1 0100 110 |

| Penalties for personal income tax paid by individual entrepreneurs on the general system | 182 1 0100 110 |

Attention!

You can get a free legal consultation at the following numbers:

+7 — Moscow and region +7 — St. Petersburg and region

Calls to all numbers are free.

Personal income tax payment deadlines

must be paid no later than the day following the day the employee (individual) is paid income. For example, the employer paid the salary for January 2021 on February 5, 2021. The date of receipt of income will be January 31, 2021, the tax withholding date will be February 5, 2021. The date no later than which personal income tax must be paid to the budget, in our example – February 8, 2021 (since the 6th and 7th are weekends).

Penalties

- Documents will not be accepted if there are errors in personal data. Such a source will be considered unreliable.

- You should be more careful about paying bonuses in the month of filing the declaration. The absence of such payments in the total amount may be interpreted by the tax office as a reduction in the figure.

- Lateness of more than one day with the transfer of tax in cases where the employee received wages, travel allowances, compensation for unused vacation.

- The tax transfer occurred later than the previous month, in which sick leave and vacation pay were paid.

How to avoid fines

First of all, you should carefully carry out calculations when drawing up documents - this is the best way to avoid fines. If a problematic situation arises, you can provide clarifying documents. In this case, payment must be made before delivery of additional documents. A fine for late payment may not be imposed in cases where the declaration was submitted on time and did not contain errors. It should be understood that in this situation it is necessary to deposit funds with the tax office until the actual discovery of the shortfall.

Penya

If a decision has been made to cancel penalties, penalties still need to be paid in cases where:

- the tax payment date was missed;

- the calculations do not correspond to reality.

When paying a penalty, must be taken into account. This precaution will help you avoid mistakes.

It is better to pay the penalty yourself before the letter from the tax office arrives. The amount can be calculated using the formula.

Payment order

Errors when filling out a payment order, especially in personal data, can lead to the payment not going through . The deposited funds will be frozen and the payment will be considered unclear. This may lead to a delay and the tax office will consider this enrollment as overdue.

Note!

1. When filling out the payer status:

- For individual entrepreneurs - enter numbers 09;

- Legal entities - indicate 02.

2. There are also differences in the tenth digit of the code when transferring financial resources:

- For individual entrepreneurs - 1;

- For legal entities - 2.

3. Transfer of funds from wages and vacation pay is carried out using a special form.

Tax on dividends of non-resident individuals

- Income can be paid either in cash or in kind (property).

- A tax agent obligated to withhold and transfer tax to the budget is a company that pays funds to its participants in cash.

- When paying income to a participant with property, the obligation to pay tax passes to the recipient of this property.

We recommend reading: Inkom real estate apartment rental agreement between individuals with a deposit sample

Since 1995, the Czech Republic has been a member of the Organization for Economic Cooperation and Development (OECD), and since 2021 it has been part of the European Union (EU). At the moment, the Czech Republic is a stable, prosperous country in central and eastern Europe, which attracts foreign investors, including from Russia. Many Russians consider the Czech Republic as a country for permanent residence. In this regard, it seems relevant to consider the legal regulation of taxation of individuals in the Czech Republic.

KBK personal income tax on dividends in 2021

We emphasize that a resident of Russia is considered a person who lives on its territory for at least 183 days over the next twelve months in a row. As an exception, the state allows short-term trips (not exceeding six months in a row) necessary for citizens to receive education or medical care, as well as work trips for the purpose of extracting hydrocarbon resources from fields in the seas. Absence from the country for more than a year without loss of resident status is permissible for three categories of payers:

Codes are used only when financial transactions are related to the state budget, that is, the country is the second party involved or the recipient of the payment. Payers enter the BCC in the appropriate fields of payment orders, not only when they are going to make a payment, but also to reimburse penalties imposed due to late or non-payment of taxes.

Kbk for personal income tax on dividends to the founder in 2021

The profit that individuals receive as a result of equity participation in organizations and companies is called dividends. It is paid directly by organizations to individuals. This situation, along with other payments intended to individuals from organizations, is accompanied by tax payments. One of which is personal income tax. The organization itself has the responsibility to calculate this amount, withhold it from the individual, and also transfer it to the budget - also lies on the shoulders of the tax agent, which this organization is. At the same time, in order to transfer the payment, you will definitely need to know the exact BCC for personal income tax on dividends in 2021.

In this case, the calculation procedure will be as follows: personal income tax = D x 13%, where D is the dividends accrued to the resident. 13% is the tax rate. The calculation will be more complicated if the organization is the founder of another company from which it received any amounts for participation in the current or previous year.

How to fill out a payment order

Let's look at how to correctly fill out a payment order for the transfer of income tax. Payment orders for the payment of fees and insurance premiums are drawn up in accordance with the rules approved by Appendix No. 2 to Order of the Ministry of Finance of the Russian Federation No. 107n dated November 12, 2013. In order for the payment to be generated correctly, you need to pay attention to the following aspects:

- in field 101 “Payer status”, enter the value 02 - tax agent;

- in field 104 - code (for example, KBK for personal income tax refund in 2021 for individuals (the same as when transferring income tax) or code for penalties, fines, interest);

- OKTMO is entered in cell 105 (the correct value for a specific institution is on the official website of the Federal Tax Service);

- field 107 indicates the tax period for which payment is made;

- the basis for the payment, which determines its purpose, is entered in field 106.

It is also mandatory to register the details of the parties - TIN, KPP of the payer (fields 60, 102) and TIN, KPP of the recipient (cells 61, 103).

IMPORTANT!

From 01/01/2021, the rules for filling out tax payment orders have changed. The Federal Tax Service transferred budget revenues to the treasury service system. Now the bank's new BIC and two accounts from the single treasury account are indicated in the payments. Payment details vary for each subject of the Russian Federation.

You can find out more about the rules for filling out a payment order in this material.

KBC dividends in 2021 personal income tax to the founder

Dividends are part of the profit remaining after taxation, which is distributed among participants, shareholders. Within the framework of tax legislation, dividends are recognized only as income accrued to the founder (participant, shareholder) when distributing profits in proportion to his share in the authorized capital (Clause 1, Article 43 of the Tax Code of the Russian Federation). If the founder (participant, shareholder) receives a part of the organization’s profit that is not proportional to his share, this payment is not recognized as dividends for tax purposes. Tax residents always pay personal income tax to the Russian budget (clause

1 tbsp. 224 of the Tax Code of the Russian Federation). At the same time, financiers noted that this rate applies to all dividends paid after 01/01/2021, regardless of the period for which they were accrued (letter of the Ministry of Finance of Russia dated 02/01/16 No. 03-04-06/4275).

New KBS from 01/01/2021

In connection with the introduction of an increased personal income tax rate from January 1, 2021, the Ministry of Finance, by Order No. 236n dated October 12, 2020, made changes to the budget classification codes (BCC) for 2021. The new codes will come into force simultaneously with amendments to Chapter 23 of the Tax Code of the Russian Federation on the introduction of a progressive rate. To transfer taxes to the budget next year, you should, among other things, apply the following BCCs for personal income tax for employees in 2021:

- 182 1 0100 110 - for personal income tax exceeding the amount of 650,000 rubles and relating to part of the base in excess of 5 million rubles;

- 182 1 0100 110 - for personal income tax from the profit of a CFC, which was received by taxpayers who switched to a special procedure for paying personal income tax based on filing a notification with the Federal Tax Service;

- 182 1 0100 110 - for personal income tax from interest (coupon, discount) on circulating bonds of Russian organizations that are denominated in rubles and issued after 01/01/2017.

Additionally, new codes have been introduced for municipal districts.

IMPORTANT!

The calculated BCCs for personal income tax for employees in 2021 for individual entrepreneurs are similar to those indicated in payment orders by legal entities. When paying income tax for employees, you must use the specified ID.

ConsultantPlus experts have sorted out which codes to indicate in payments for taxes and fees. Use these instructions for free.

to read.