Who must submit a balance sheet?

The balance sheet is one of the financial reporting forms.

The legislation establishes that all legal entities, regardless of their organizational form and the applicable taxation regime, must prepare and submit reports to tax and statistical authorities. This obligation also applies to non-profit organizations and bar associations. Balance sheets and profit and loss statements do not have to be submitted only to entrepreneurs, as well as branches of foreign companies. But they can do this on their own initiative.

Attention! Previously, some organizations were exempt from preparing a balance sheet, but currently such provisions are no longer in effect. Business entities classified as small businesses are given the right to submit reports in a simplified form. It includes a balance sheet in Form 1 and a statement of financial results in Form 2, so enterprises must send it to regulatory authorities.

Construction principles

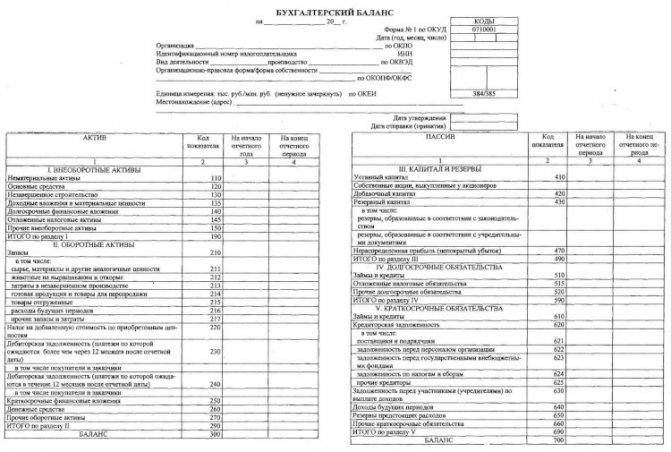

The structure of the enterprise’s balance sheet is a two-sided table for a certain date - at the end of the quarter or at the end of the year:

- left side - Asset, which reflects economic assets by composition and placement;

- the right side is the Passive, which reflects funds by source of education and intended purpose.

An important condition of the Balance is that the Asset must always be equal to the Liability. Since Liabilities represent the Capital and Liabilities of an enterprise, this equality can be presented as follows:

Assets = Capital + Liabilities

The Asset and Liability items of the Balance Sheet, based on economic homogeneity, are summarized in certain sections of the report.

The asset of the Balance Sheet reflects the property of the enterprise and consists of two sections:

- Non-current assets: fixed assets; Construction in progress; intangible assets; profitable investments; long-term financial investments and so on;

- Current assets: inventories and costs; cash; accounts receivable; short-term financial investments and so on.

The liability side of the Balance Sheet is the source of formation of the enterprise’s property and consists of two sections:

- Capital and reserves – equity capital: authorized, additional and reserve capital of the company; savings and social funds; targeted funding and revenues; retained earnings;

- Borrowed capital – external liability: long-term loans; short-term loans and borrowings; accounts payable.

Each separate type of property or source of funds is called a “balance sheet item.”

Balance due dates

According to the general rules, the balance sheet - Form 1 must be submitted as part of the reporting for the past year no later than March 31 of the following year. This deadline must be observed when submitting balance sheets and other forms to the Federal Tax Service and statistics.

In addition, under certain conditions, an audit report must be sent to Rosstat as an attachment. The deadline is set for ten days, but no later than December 31 of the following year.

Some organizations need to submit financial statements and publish them due to the type of activity they carry out, or according to other criteria defined by law. For example, tour operators must send their reports to Rostrud within three months from the date of their approval.

The legislation provides for separate deadlines for organizations that registered after September 30 of the reporting year. Due to the fact that their calendar year may be determined differently in this case, the due date may be set by such organizations on March 31 of the second year after the current one. For example, Rebus LLC received an extract from the Unified State Register of Legal Entities on October 25, 2017; the accounting report must be submitted for the first time on March 31, 2021.

Attention! Accounting statements are usually submitted based on the total for the year. However, it is possible to present it quarterly. In this case it is called intermediate. Such documentation is very often needed when applying for loans from banks, company owners, etc.

Where is it provided?

The provisions of federal laws establish that Form 1 balance sheet and Form 2 profit and loss statement, and in certain cases other forms, must be submitted:

- Federal Tax Service - reporting must be submitted at the place of registration of the company. Therefore, branches and other separate divisions do not submit it, and only the parent company submits consolidated statements. This must be done at the place where it is registered, taking into account these departments.

- Rosstat - currently submitting reports to statistical authorities is mandatory. If this is not done, then, just as in the first case, the company and officials may be held liable.

- For the founders and other owners of the company - this is due to the fact that each annual report of the organization must be approved by its owners.

- To other bodies, if the relevant regulations define such a duty.

Attention! Banks may be asked to provide reporting when applying for various types of loans and borrowings from them. Especially if you take out a loan to open or develop a business.

Currently, when concluding contracts, many large companies ask for Form 1 Balance Sheet, Form 2 Profit and Loss Statement. This should be done at the discretion of the company management.

However, at present, many specialized companies through which you can submit reports have a service that allows you to obtain all the necessary information about a partner according to his TIN or OGRN. This data is provided by the Federal Tax Service itself based on previously submitted reports.

You might be interested in:

Reporting in 2021 for LLCs and individual entrepreneurs: deadlines, general table for LLCs, simplified tax system, UTII, unified agricultural tax

Form 2. Statement of financial results

When preparing a statement of financial results, the same rules apply as when creating a balance sheet. Another thing is that here it is necessary to carry out calculations very carefully to reflect the net profit after tax indicator. This indicator must be identical to the organization’s income tax return. They must be the same, otherwise the Federal Tax Service may apply penalties. Accounting statements forms 1 and 2 (filling sample) are presented below:

- Sample of filling out Form 1 (balance);

- Sample of filling out form 2 (report).

You can also download the form (Form 2 of financial statements):

- Balance sheet;

- Report form.

Similar articles

- Accounting statements for 2021 under the simplified tax system

- New forms of financial statements in 2021

- Financial statements in TOGS: what is it?

- Accounting calendar for 2021 - reporting

- Composition of financial statements 2021 for small businesses

Delivery methods

The OKUD form 0710001, which is part of the annual report, can be submitted to the Federal Tax Service and Rosstat in the following ways:

- Personally by a company representative to an inspector or Rosstat specialist.

- By sending through the postal service - in this case, the letter is subject to requirements for the content of the inventory, and it must also be valuable.

- Through an electronic document management system - in this case, the company must have an appropriate electronic digital signature (EDS) and enter into an agreement with a special operator. You can also send the aileron file with reporting through the tax website; you will also need an enhanced digital signature.

Attention! The legislation stipulates the submission of the report in electronic form if the number of employees of the organization is more than 100 people.

Balance sheet form 2021 free download

Balance sheet form 1 form 2021 free download in Word format.

Balance sheet form 1 form 2021 download free in Excel format.

Balance sheet with line codes form download in Excel format.

Download a sample of filling out the balance sheet in Form 1 for 2021 in PDF format.

How to fill out a balance sheet using Form 1

Title part

After the name of the form, it is indicated on what date it is being generated. The actual date of submission of the report must be entered in the table, in the line “Date (day, month, year)”. Next, the full name of the subject is written down, and opposite in the table is its OKPO code.

After this, his TIN is indicated on the next line in the table. Next, you need to indicate the main type of activity - first in words, and then in a table using the OKVED2 code. Then the organizational form and form of ownership are indicated.

On the contrary, the corresponding codes are entered in the table, for example:

- The code for LLC is 65.

- for private property - 16.

On the next line you need to choose in what units the data in the balance sheet is presented - in thousands or millions. The table displays the required OKEI code. The last line contains the address of the subject's location.

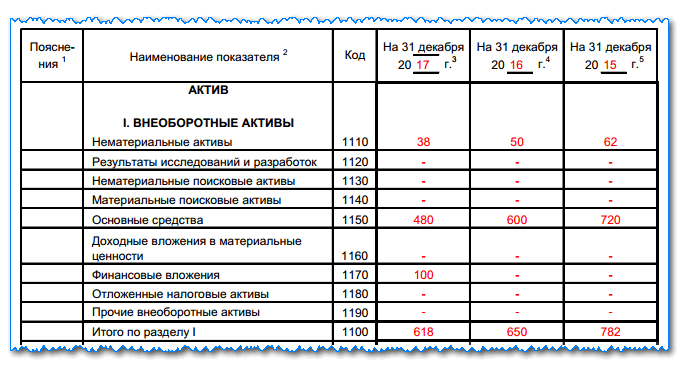

Assets

Fixed assets

Line “Intangible assets” 1110 is the balance of account 04 (except for R&D work) minus the balance of account 05.

Line “Research results” 1120 - account balance 04 for sub-accounts that reflect R&D;

Line “Intangible search requests” 1130 - account balance 08, subaccount of intangible costs for search work.

Line “Material search requests” 1140 – account balance 08, subaccount for the costs of material assets for search work.

Line “Fixed assets” 1150 - account balance 01 minus account balance 02.

Line “Income-bearing investments in MC” 1160 - the balance of account 03 minus the balance of account 02 in terms of accrued depreciation on assets related to income-generating investments.

Line “Financial investments” 1170 - account balance 58 minus account balance 59, as well as account balance 73 in terms of interest-bearing loans over 12 months.

Line “Deferred tax assets” 1180 - account balance 09, it is possible to reduce it by account balance 77.

Line “Other non-current assets” 1190 - other indicators that need to be reflected in the section, but they are not included in any line.

The line “Total for section” 1100 is the sum of lines from 1110 to 1190.

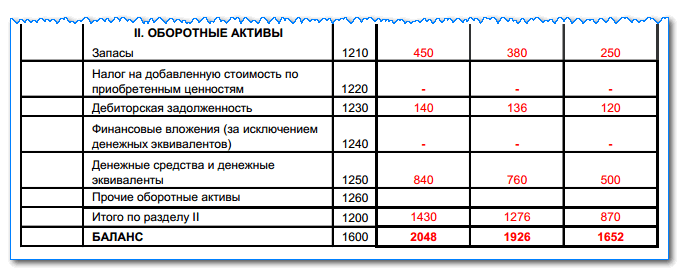

Current assets

Line “Inventories” 1210 - the sum of indicators is entered in the line:

- account balance 10 minus account balance 14, or account balances 15, 16

- Balances on production accounts: 20, 21, 23, 29, 44, 46

- Balances of goods on accounts 41 (minus the balance on account 42), 43

- account balance is 45.

Line “Value added tax” 1220 - account balance 19.

Line “Accounts receivable” 1230 - the sum of indicators is entered:

- Debit balances of accounts 62 and 76 minus the credit balance of account 63 in the subaccount “Reserves for long-term debts”;

- The debit balance of the account is 60 for advances made for the supply of products and services.

- Debit balance of account 76, subaccount “Insurance payments”;

- The debit balance of the account is 73, excluding the amounts of loans on which interest is accrued;

- Debit balance of account 58, subaccount “Granted loans for which interest is not accrued.”

- Debit account balance 75;

- Debit account balance 68, 69

- The debit balance of the account is 71.

You might be interested in:

SZV-STAZH: who should take it, in what time frame, sample filling

Line “Financial investments” 1240 - the sum of indicators is entered:

- account balance 58 minus account balance 59;

- account balance 55, subaccount “Deposits”;

- account balance 73, subaccount “Loan settlements”.

Line “Cash” 1250 - the sum of account balances 50, 51, 52, 55, 57 is entered.

Line “Other current assets” 1260 - indicators that should be shown in the section, but were not included in any previous line.

The line “Total for section” 1200 is the sum for lines from 1210 to 1260.

Line “Balance” 1600 - the sum of lines 1100 and 1200.

Passive

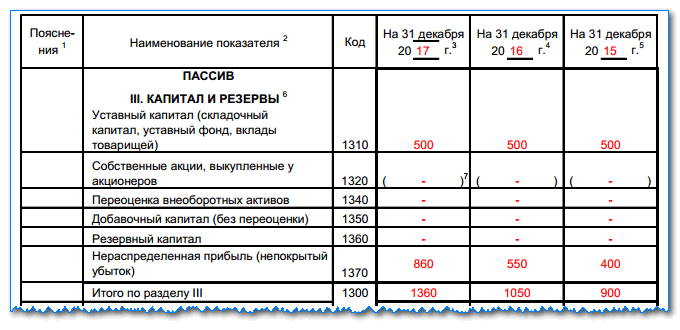

Capital and reserves

Line “Authorized capital of the organization” 1310 - account balance 80.

Line “Own shares” 1320 - account balance 81.

Line “Revaluation of non-current assets” 1340 - account balance 83 in terms of the amounts of revaluation of fixed assets and intangible assets.

Line “Additional capital” 1350 – account balance 83 without the amounts of additional valuation of fixed assets and intangible assets.

Line “Reserve capital” 1360 - the sum of account balances 82, as well as 84 in terms of special funds.

Line “Retained earnings (uncovered loss)” 1370 - account balance 84 without special funds.

Line “Total for section” 1300 - the sum for lines 1310, as well as from 1340 to 1370 minus line 1320.

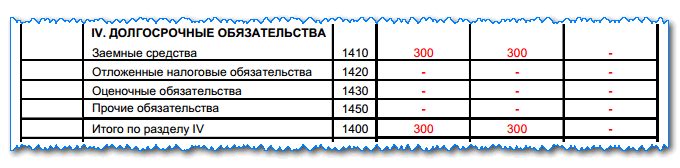

long term duties

Line “Borrowed funds” 1410 - account balance 67, including the amount of loans and interest accrued on them.

Line “Deferred tax liabilities” 1420 - account balance 77, it can be reduced by account balance 09.

Line “Estimated liabilities” 1430 - account balance 96 for the subaccount of estimated liabilities for more than 12 months.

Line “Other liabilities” 1450 - credit balances of accounts , , 68, 69, , 76 for which liabilities with a maturity period of more than 12 months are reflected.

Line “Total for section” 1400 - the sum for lines from 1410 to 1450.

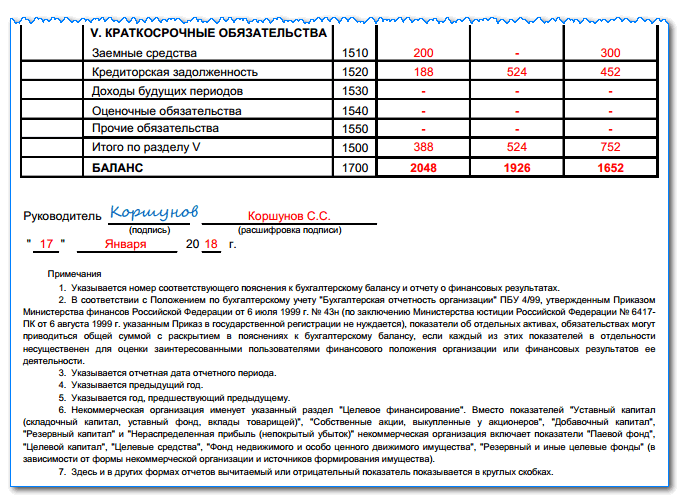

Short-term liabilities

Line “Borrowed funds” 1510 - account balance 66, including loan amounts and interest accrued on them.

Line “Accounts payable” 1520 - The amount of indicators is entered in the court:

- Balances of accounts 60 and 76, which show the debt to suppliers and contractors;

- The balance on the credit of account 70, except for the debt on payment of income on shares and shares;

- The balance on the credit of the sub-account “Settlements on deposited amounts” of account 76;

- Credit balances of accounts 68 and 69;

- Account credit balance 71;

- Balances on the subaccounts “Calculations for claims” and “Calculations for property insurance” on account 76;

- Credit balances on accounts 76 and 62 for advances received;

- Credit balance on the subaccounts “Calculations for the payment of income” of account 75 and “Calculations of income for the payment of income on shares” of account 70

Line “Deferred income” 1530 - loan balances for accounts 86 and 98.

Line “Estimated liabilities” 1540 - balance from account 96 in the subaccount of estimated liabilities for less than 12 months;

Line “Other short-term liabilities” 1550 - other short-term liabilities that cannot be included in the previous terms of Section V.

The line “Total for section” 1500 is the sum for lines from 1510 to 1550.

Line “Balance” 1700 - the amount for lines 1300, 1400 and 1500.

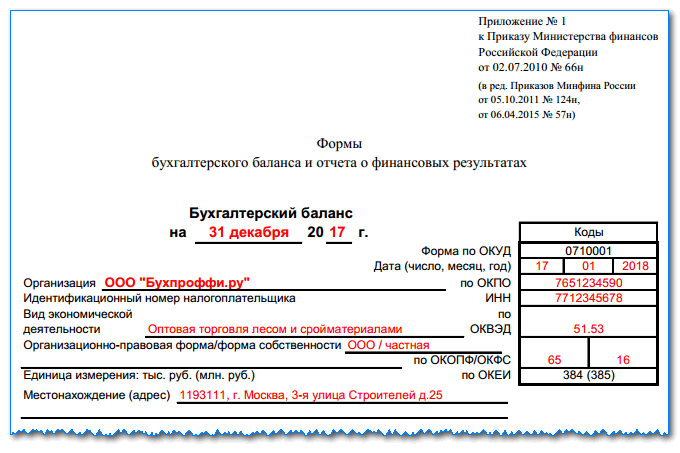

Sample balance sheet form 1

The form consists of a “header” and two tables: assets and liabilities. Let's fill in each part of the balance sheet sequentially.

Fill out the header:

At the top we indicate on what date the balance sheet is drawn up. We will give an example of the organization Confectioner LLC, which reports for the calendar year 2012.

Accordingly, the balance sheet date is December 31, 2012.

Next, we write the name of the organization, its individual code OKPO, INN, type of activity OKVED, approved by the classifier of statistical authorities.

In the line “organizational and legal form” we write LLC, “form of ownership” - private, also here you need to note the corresponding property codes: OKFS, OKOPF. For LLC - code 65. For private ownership, the corresponding code is 16.

All numerical entries in the balance sheet will be expressed in thousands; accordingly, in the “unit of measurement” line of the balance sheet we will indicate the code 384. For millions of rubles, the corresponding code will be 385.

In the last line of the “header” we indicate the legal address of the organization, that is, the address where it is officially registered.

We fill out the “Assets” table of the balance sheet:

This table consists of two sections: non-current assets and current assets. As mentioned above, to fill out Form 1 we will use the data from the balance sheet.

Opposite each type of asset (in the balance sheet these are called balance sheet items) the corresponding amount is written, rounded (for our case) to thousands of rubles. The first column indicates data as of the reporting date of the reporting period (for our sample, 12/31/2012), the second column shows data as of the end of the previous year (12/31/2011), and the third column shows data as of the end of the year preceding the previous one (12/31/2010). ).

Section I Non-current assets Form 1: (click to expand)

- intangible assets (1110): the residual value is indicated, obtained as the difference between the accounting value of intangible assets (debit 04 “Intangible assets) and accrued depreciation (credit 05 “Amortization of intangible assets”), the data from line 1120 is not taken into account here;

- research and development results (1120): data on completed research and development works (R&D), data for this article is taken from the account. 04 “Intangible assets” sub-account “R&D”;

- intangible and tangible exploration assets (1130-1140): data on search, exploration of mineral deposits, as well as on the equipment used for this.

- fixed assets (line 1150): we also indicate the residual value obtained as the difference between the accounting value of fixed assets (debit account 01 “Fixed Assets”) and accrued depreciation (credit account 02 “Depreciation”);

- profitable investments in tangible assets (1160): data on fixed assets accounted for in account 03 “Income-generating investments in tangible assets” are also determined by their residual value.

- financial investments (1170): the organization’s financial investments for a period of more than 12 months are indicated (composed of debit 58 “Financial investments” and debit 55 “Special accounts in banks” subaccount “Deposits”);

- deferred tax assets (1180): the balance of account 09 “Deferred tax assets” is taken;

- other non-current assets (1190): all other non-current assets that were not reflected in previous articles are indicated.

- Total for section I (1100): the values of lines 1110-1190 are summed up.

Section II Current assets form 1:

- inventories (1210): all inventories available to the enterprise are taken into account (data relating to materials, raw materials are taken: account 10 “Materials”, 15 “Procurement and acquisition of material assets”; related to production: 20 “Main production”, 21 “ Semi-finished products of own production", 23 "Auxiliary production", 28 "Defects in production", 29 "Service production and facilities"; relating to goods and finished products: 41 "Goods", 42 "Trade margin", 43 "Finished products", 44 “Sales expenses”, 45 “Goods shipped”, as well as 97 “Deferred expenses”;

- VAT on acquired assets (1220): the balance of account 19 “VAT on acquired assets” is indicated, that is, the VAT that was presented by suppliers but not accepted for deduction;

- accounts receivable (1230): the amount of debt of counterparties to the organization, data is taken from accounts that record relationships with various counterparties: suppliers (account 60), buyers (account 62), personnel (70, 71, 73), tax office and PF (68 and 69), founders (75), other counterparties (76);

- financial investments (1240): investments for a period of less than 12 months;

- cash and cash equivalents (1250): all funds of the enterprise in rubles (account balance 50 and 51), foreign currency (account balance 52), checks, letters of credit (account balance 55 for subaccounts “Checks”, “Letters of Credit”);

- other current assets (1260): all other current assets that are not reflected in the previous lines are indicated;

- total for section II (1200): the sum of the values of lines 1210-1260.

Balance (1600): the data of lines 1100, 1200 are summed up.

We fill out the “Liabilities” table of the balance sheet, form 1:

The liability table of Form 1 consists of three sections: capital and reserves, long-term liabilities, short-term liabilities.

Section III Capital and reserves:

- authorized capital (1310): credit balance of account. 80 “Authorized capital”;

- own shares (1320): debit balance of account. 81 “Own shares (shares)”;

- revaluation of non-current assets (1340): if the organization revalued intangible assets and fixed assets, then the amount by which the value of non-current assets increased (credit balance account 83 “Additional capital”);

- additional capital without revaluation (1350): credit balance of account. 83 minus the amounts specified in line 1340);

- reserve capital (1360): if the organization creates reserve capital from retained earnings, then this data is reflected in this line (debit 82 “Reserve capital”);

- retained earnings (uncovered loss) (1370): data is taken from account 84 “Retained earnings (uncovered loss”).

- Total for section III (1300): the sum of the values of lines 1310-1370.

Section IV Long-term liabilities:

- borrowed funds (1410): loans to an organization for a period of more than 1 year (loan 67 “Settlements on long-term loans and borrowings”);

- deferred tax liabilities (1420): credit 77 “Deferred tax liabilities”;

- estimated liabilities (1430): credit 96 “Reserves for future expenses”, the period for fulfilling these obligations is over 1 year;

- other liabilities (1450): all liabilities not reflected above for a period of more than 1 year are indicated;

- total for section IV (1400): the sum of the values of lines 1410-1450.

Section V Current Liabilities: (click to expand)

- borrowed funds (1510): loans with a maturity of less than 1 year (loan 66), as well as long-term loans with a repayment period of less than 1 year (loan 67);

- accounts payable (1520): debt to suppliers (account 60), customers (62), personnel (70, 71, 73), budget (68 and 69). founders (75), other counterparties (76) for a period of less than 1 year;

- deferred income (1530): data from account 98 “Deferred income” (credit balance);

- estimated liabilities (1540): loan 96 “Reserves for future expenses”, maturity period less than 1 year;

- other liabilities (1550): all other short-term liabilities with a maturity of less than 1 year that are not reflected above are indicated;

- total for section V (1500): sum of lines 1510-1550.

Balance (1600): sum of line values 1400, 1500.

Upon completion of the balance sheet form 1, the values of lines 1700, 1600 must match. And this is logical. After all, liabilities are the sources of asset formation; each accounting entry (accounting entry) is made simultaneously as a debit to one account and a credit to another. If you have any discrepancies when filling out form No. 1, then you need to look for an error in accounting. The task is painstaking and long, but there is no other way out.

See here for the procedure for filling out a balance sheet for small businesses. In this article you will find a sample of filling out Form 2, here for Form 3, and here for Form 4.

in .xls format

(approved by Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66 (as amended by Order of the Ministry of Finance of the Russian Federation dated October 5, 2011 No. 124n)

Common mistakes when filling out a balance

When filling out a balance sheet, novice accountants often make the following mistakes:

- Accounts receivable and payable are shown as a collapsed indicator. This is a mistake - in the balance sheet you need to show separately the debt to debtors or creditors and separately - received or paid advances. Profits and losses should be reflected using the same principle.

- The amount of the advance received should not be reflected in pure form, but together with the VAT received with this payment.

- Fixed and intangible assets are reflected at historical cost. This is not true. These values must be adjusted to the amount of accrued depreciation for each type of property.

- Interest-free loans are shown as part of financial investments. This is incorrect; they should be shown as part of accounts receivable by maturity.

- Negative indicators are written with a minus sign. According to the instructions for filling out the form, negative values must be shown in parentheses without a minus.

Rules for filling out the report form

Filling out the balance sheet should be done by a specialist - a company accountant or an outsourced outsourced employee. Preparation of the document is possible only after completion of all other accounting work, when accurate and reliable data on the company’s finances is known. The basic information is taken from the balance sheet: its final indicators are transferred to the balance sheet.

If the table is filled out for the year, then the reporting date will be December 31. The structure of the balance sheet involves the division of assets and liabilities into short-term and long-term (current and non-current).

Basic rules for filling out a balance sheet:

- assets and liabilities cannot be counted against each other (for example, if a company has accounts receivable for 30 thousand and accounts payable for 10 thousand, their difference is not recorded in the document, but each is indicated in full on separate lines);

- the balance sheet will contain data for at least 2 years;

- amounts are indicated in thousands;

- all indicators are reflected in a net assessment, that is, minus regulatory values;

- when indicating the cost of fixed assets of production, depreciation is taken into account;

- data on loans, credits, deposits, deposits in other companies and securities are divided into short-term and long-term, respectively, displayed in different parts of the assets;

- receivables and payables are shown as assets and liabilities in current liabilities;

- all funds are displayed as a total amount minus deposits indicated as financial investments;

- retained earnings or uncovered loss is the result of work over a certain number of years.

The balance sheet form is a table that discloses information about short-term and long-term liabilities, debts, and property