Each time an employee is sent on a business trip, the employer is required to calculate travel allowances to be issued to the employee. It is necessary to issue:

- advance payment for travel expenses to the place of business trip and back;

- money for renting accommodation;

- daily allowance.

The worker is also entitled to payment for a business trip based on average earnings (2020): even if the trip lasts several months, the employer is obliged to retain it for the employee for the entire period of temporary absence on the instructions of his superiors.

How to calculate travel allowances online

Even if you know the rules by heart for how travel allowances are calculated, it is easy to make mistakes in the calculations, which can lead to long disputes and proceedings. Our free service will help you avoid them.

How to use an online travel allowance calculator in 2021? To do this you will need 4 digits:

- the employee’s total earnings for the last 12 months or for the period actually worked;

- number of days worked (working days, if not sick or on vacation);

- duration of business trip;

- the amount of daily allowance entered by the employer.

All numbers must be entered in the fields provided. And the program itself will calculate the required amounts.

We will show you how to calculate travel allowances in 2021 with examples. Let's say employee Ivanov is sent on a business trip for 10 days. He worked in the organization for 6 months (from January to June 2021). Using the production calendar, we determine that it is 116 days. During this period (according to accounting data) he received 180,000 rubles. Daily allowance in the organization is 100 rubles per day. Enter the initial data.

Click on the “Calculate” button and get the amounts that need to be paid.

The program contains not only an algorithm for calculating travel allowances in 2021, it also calculates average earnings and daily allowances. All this data is accurate and can be used in your work.

Registration of foreign business trips

When an employee is sent on a business trip abroad, the employer issues a corresponding order in the T-9 form. It displays data about the location, target tasks, and information about the posted worker.

Documents for download (free)

- Form No. T-9

Before departure, an advance is issued - in cash or on a card, its amount is determined based on the duration of the trip. Upon return, the employee provides his employer with a detailed advance report of the amounts spent. All expenses are displayed in several accounts, and estimates are prepared.

How to calculate travel allowances yourself

To do this, you will need to calculate the average salary, then multiply it by the number of days of business travel. At first glance, it is not difficult. But we must take into account that the procedure for calculating the average salary is set out in Article 139 of the Labor Code of the Russian Federation, and the formula for calculating the average salary for business travelers is described in detail in Government Resolution No. 922 of December 24, 2007, which approved the Regulations on the specifics of the procedure for calculating the average salary .

In accordance with the algorithm for calculating average earnings for a business trip, the calculations take into account the employee’s income for one year or twelve months. If less than a year has been worked, the actual period of time worked is taken.

Step 1. Calculate the number of days actually worked. These do not include sick leave, periods of temporary disability, maternity leave, annual paid leave, etc. (the full list is set out in paragraph 5 of Decree No. 922 dated December 24, 2007).

Step 2. Determine your total earnings. All payments that the employee received during the pay period must be added up. When adding, check whether travel allowances are included in the calculation of average earnings in your case. Let us remind you that only payments that the employee received by force of law are not taken into account, and not for time worked (temporary disability, for example).

Step 3. We clarify the average daily earnings. We divide the total earnings by the number of days actually worked.

The next step for calculating travel allowances is to figure out how much to pay. There is a nuance here. Average daily earnings must be multiplied by the number of working days of a business trip, but weekends and holidays are not included if the person did not work on these days. If you worked, you have to pay them, and double the amount.

It is advisable to check all the numbers several times so that errors do not creep in. You can also use the online calculator for calculating travel allowances in 2021 - a free service that does not allow for inaccuracies.

We determine the days of departure and arrival

The amount of daily allowance for one day of a business trip can be any.

The amount is specified in a collective agreement or local regulation. If the nature of the employee’s activities involves regular business trips, then a table with daily allowances, depending on the location, can be attached to the employment contract. The Tax Code stipulates that daily allowances up to 700 rubles for domestic trips and 2,500 rubles for foreign trips are not subject to personal income tax.

If an employee goes on a business trip to an area from where it is possible to return home every day, then he is not paid per diem. The expediency of such trips is determined by the manager.

Per diem is paid to the employee for each day of business travel, including weekends and holidays, as well as forced delays (not through the employee’s fault). An employee has the right to daily allowance if he was on sick leave during a business trip. The start of the business trip duration report is the departure day.

The arrival date is calculated in the same way. For example, an employee finished his work on April 10 and left on the same day by train for his locality. The train arrives at 00.05 on April 11. This day is still considered a business trip period and a daily allowance is payable for it. It is also necessary to take into account the time required to travel from the airport, pier, train station, if they are located outside the city. This calculation procedure was approved by Decree of the Government of the Russian Federation No. 749 of October 13, 2008.

Did you know

The legislation provides for compensation of expenses for taxis and personal transport on a business trip. Documentary evidence of these expenses is required. Read more

Here

- for the period when the employee was in the country, daily allowances are paid at the rate for domestic business trips (including for the period necessary to arrive at the airport);

- for the period when the employee was in the territory of another country, he must be paid per diem according to the norms for a foreign business trip and in local currency.

The daily allowance on the day of arrival in another country is calculated according to the standards for a business trip abroad. On the day the employee returns to the country, he receives daily allowance according to the norms for a domestic business trip. Border crossing dates are verified by the stamp in the passport. On business trips to CIS countries, when crossing the borders of which there is no mark in the passport, the dates of departure and arrival are calculated according to travel documents.

If during a business trip an employee moves from one country to another, then for the day of crossing the border, the payment of daily allowance for business trips is made according to the norm of the country of arrival.

note

If departure or arrival falls on a weekend, then payment is made in an increased amount, since the legislation clearly establishes days of work and rest. However, employers often forget about such points, which is a violation of rights under the Labor Code. Read more in this

article

The employee was sent on a business trip to Germany. The plane takes off at 00.30 on April 4. In order to get to the airport, which is located outside the city, and register, he needs to leave by car no later than 22.00. The business trip ends on April 10, and the plane leaves France on April 10 at 23.

- The start of the business trip is April 3. For this day, the employee will receive 750 rubles.

- From April 4 to April 10, daily allowances are calculated at 2500 per day: 8 days *2500 = 20,000 rubles (these funds must be paid in euros).

- The last day of the trip is April 11. For this day, the employee is entitled to 750 rubles in travel allowance.

For example, a similar business trip was planned, but due to bad weather conditions the plane’s departure was delayed for a day. In fact, the plane took off at 23.00 on April 11 and arrived on April 12. In such a situation, the employee must be paid 2,500 rubles per diem for April 10 and 11, and 750 rubles for April 12.

Changes to the Tax Code came into force on January 1 of this year. If previously amounts over 750 and 2,500 rubles for domestic and foreign business trips, respectively, were subject to only personal income tax, now insurance contributions must also be paid on them.

A lawyer will advise you in the comments to the article

An employee of an organization who leaves to carry out an official assignment outside the place of permanent work (on a business trip) is compensated for the additional expenses incurred by him related to living outside his place of permanent residence, called daily allowances (Article 168 of the Labor Code of the Russian Federation, clause 11 of the Regulations on the specifics of sending employees to work business trip approved by Decree of the Government of the Russian Federation dated October 13, 2008 No. 749, hereinafter referred to as the Regulations).

Many believe that daily allowances are paid to an employee primarily for food on a business trip, so to speak, as compensation for the lack of homemade borscht and cutlets. But it is not so. The costs of food, clothing and other employee needs are his personal problems. He receives a salary and decides where and how to spend it.

The fact that he is on a business trip does not mean that his home office is obliged to feed him at this time. He is obliged to pay for travel to and from the place of business trip, accommodation and other documented expenses that he is forced to bear only because he performs work outside his place of residence, but not at all to feed him.

https://www.youtube.com/watch?v=79q-vjrA8ic

Daily allowances are issued to compensate for those expenses that cannot be taken into account in advance or that cannot be documented.

Costs for travel to the place of business trip, chocolate (according to the good old tradition) for the boss’s secretary with whom you will need to communicate, telephone conversations on work issues on a personal mobile phone, etc. All these expenses cannot be documented. They would not arise in a permanent place of work, but the employee must be compensated for them. After all, they are clearly aimed at solving those tasks for which the employee was sent on a business trip.

The day of departure on a business trip is the date of departure of the vehicle - train, plane, bus, ship, etc. – from the place (locality) of permanent work, and not the employee’s place of residence (clause 4 of the Regulations).

When leaving a vehicle before 24 hours inclusive, the day of departure is considered the current day, and from 00 hours and later – the next day.

If the train leaves on October 5 at 23:59, then the employee left on a business trip on October 5. If the train departs, for example, 4 minutes later, that is, at 00:03, then it is already October 6 - the next day.

When a station, pier or airport is located outside a populated area, you should take into account the time required to travel to the station, pier or airport.

At the same time, let us once again draw attention to the fact that a locality is the location of the organization, and not the place of residence of the employee.

That is, according to clause 4 of the Regulations, an employee (even at three o’clock in the morning) on a business trip formally leaves his place of permanent work, and not from home. And the time required to get to the airport is calculated based on the route: “Work - Airport”, not “Home - Airport”.

Before boarding the plane at the airport, you must go through registration and personal search. Check-in, as a rule, begins 2 hours before the departure time indicated on the ticket (the departure time, like the arrival time, is always local), and ends 40 minutes before the departure of the plane.

Passengers who are late for check-in or boarding the plane will not be allowed to board the flight. Consequently, to the time required to get to the airport (on average, it’s about an hour), you need to add another hour to go through check-in, security, and wait for the announcement to board the plane.

You can board the train three minutes before departure (train tickets indicate Moscow departure and arrival times), as well as board the bus.

If an employee goes on a business trip in official transport, in his own car (or in someone else’s car, driving it by proxy), then the period of departure for the business trip is determined by supporting documents. They can serve, in particular, as a car waybill, invoices, receipts, gas station receipts, or other documents confirming the route (clause 7 of the Regulations).

If travel documents are not available, then the period of stay on a business trip can be confirmed by documents for renting residential premises at the place of business trip (clause 7 of the Regulations).

But if an employee cannot present documents of residence, then he must confirm the length of stay on a business trip with an official (report) note or a document from the receiving party about his actual presence there (clause 7 of the Regulations). Such a document can be drawn up in any form. But in essence, it is a duplicate of a travel certificate, the mandatory presence of which was abolished on January 8, 2015 by Decree of the Government of the Russian Federation dated December 29, 2014 No. 1595.

Therefore, in our opinion, when sending an employee on a business trip, it is optimal to still issue him a travel certificate. An example, as before, can be form No. T-10, approved by Decree of the State Statistics Committee of Russia dated 01/05/2004 No. 1 “On approval of unified forms of primary accounting documentation for the accounting of labor and its payment,” which since 2013, we recall, is not mandatory for use.

The day of arrival from a business trip is calculated in a similar manner, that is, according to a travel document, which also indicates the time of stay. However, there is no time given to get from the airport to the place of permanent work.

If the plane lands at 23:59 (according to the ticket), then this day should already be considered the last for business travel purposes. Although getting there at night will probably be a little more difficult than in broad daylight. True, if necessary, theoretically you can get a certificate from the airport stating that the actual landing was at 00.07.

- consciousness of the subordinate;

- relations between the manager and the employee and, in general, between employees in the company;

- corporate culture;

- production situation, etc.

- expenses for travel to and from the place of business travel;

- living expenses;

- additional expenses for accommodation (per diem);

- average earnings;

- other expenses permitted by the employer.

We calculate daily allowances

For civil servants, calculating daily allowances for business trips in 2021 will not be difficult: for the day of a business trip, an official can receive only 100 rubles.

For employees of commercial organizations, the amount of daily allowance is, so to speak, unlimited. Before the entry into force of Federal Law No. 122 of August 22, 2004, Article 168 of the Labor Code of the Russian Federation stated that “the amount of compensation cannot be less than the amount established by the Government of the Russian Federation...”. Now this is no longer the case, and the daily allowance can start from one ruble, and is not limited by an upper limit.

The amount of daily allowance is determined by the local regulatory act of the organization, but when determining it, it is necessary to remember that daily allowance is not subject to personal income tax within the limits of 700 rubles in Russia and 2,500 rubles abroad for each day of a business trip. Amounts exceeding the specified values are subject to taxation in accordance with Article 217 of the Tax Code of the Russian Federation.

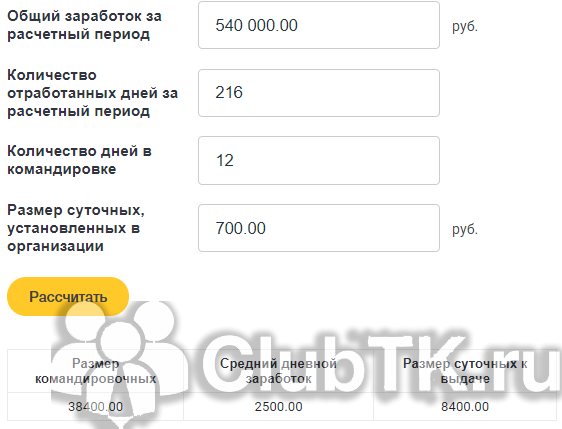

Example of calculating travel allowances

Let's say the head of the technical control department A.V. Vasiliev goes on a business trip on January 22, 2019 for 12 days. In the period from 01/22/2018 to 01/21/2019 there are only 246 working days. We exclude the period of being on annual paid leave - 20 working days, 10 working days for the period of temporary disability. Total 216 days worked.

During the reporting period, Vasiliev’s salary amounted to 540,000 rubles (45,000 rubles × 12 months).

The average daily earnings were 2,500 rubles (540,000 rubles / 216 days worked).

Vasiliev is leaving on a business trip for 12 days, therefore, he will receive a daily allowance of 8,400 rubles (700 rubles × 12 days).

Thus, the amount of travel allowance was 33,400 rubles (2,500 rubles × 10 days of business trip (because there are two days off during the business trip) and plus 8,400 daily allowances).

Just for fun, let’s check the calculations on a calculator.

The numbers match. Only with independent calculations we spent 10-15 minutes, and the calculator gave the results instantly.

Calculation of travel expenses

If the organization does not provide a procedure for ordering and paying for travel documents, the employee can independently organize his trip to the place of business trip and back by ordering and paying for tickets from the amount of the advance payment issued to him.

To prevent employees from flying business class or traveling on trains in sleeping cars, employers can set certain restrictions on expenses, as was done for civil servants in Government Resolution No. 729 of October 2, 2002.

Limitations on travel expenses to and from the place of business travel:

- by rail - only in the compartment carriage of a fast branded train;

- by water transport - in the cabin of the V group of a sea vessel of regular transport lines and lines with comprehensive passenger services, in the cabin of the II category of a river vessel of all lines of communication, in the cabin of the I category of a ferry vessel;

- by air - in the economy class cabin;

- by road - in a public vehicle, except for a taxi.

Calculation of travel allowances for renting residential premises

It is done in the same way with travel expenses. Government Decree No. 729 limits the expenses of civil servants for renting residential premises to 550 rubles per day.

However, the Government decided that expenses exceeding the specified amounts, as well as other expenses associated with business trips (provided that they were made by the employee with the permission or knowledge of the employer), can be reimbursed by saving the organization’s funds under the corresponding expense item.

Reflection in accounting

The document called the chart of accounts contains a special account 71, intended for settlement transactions with accountable persons. It is used for settlement actions with absolutely all accountable employees.

Debit account

The Debit of this account records all amounts that were issued to the employee. It turns out that the issuance of a certain amount to an employee is displayed as part of the Dt posting. 71 Kt. 50.

If the return employee has some amount left, then it is returned to the organization's cash desk, a cash order is filled out, and the corresponding entry Dt is generated. 71 Kt. 50.