In what cases do Payment based on average earnings and additional payment up to average earnings apply?

In some cases, an employee may be transferred to a lower-paid job while maintaining average earnings:

- when transferring pregnant women to “light labor” (Article 254 of the Labor Code of the Russian Federation);

- for health reasons in accordance with a medical report (Article 73 of the Labor Code of the Russian Federation);

- without his consent for a period of up to one month in cases provided for in Art. 72.2 Labor Code of the Russian Federation;

- by agreement with the employer;

- in other cases provided for by the Labor Code of the Russian Federation.

ZUP 3.1 provides two payment options for such periods:

- Additional payment up to average earnings;

- Payment according to average earnings.

Let's consider both options in more detail.

Costs for calculating income tax

Expenses are recognized as justified and documented expenses (and in cases provided for in Article 265 of the Tax Code of the Russian Federation, losses) incurred (incurred) by the taxpayer.

Justified expenses mean economically justified expenses, the assessment of which is expressed in monetary form.

Documented expenses are expenses that are confirmed by documents drawn up in accordance with the legislation of the Russian Federation, or drawn up in accordance with business customs applied in the foreign state in whose territory the corresponding expenses were incurred, and (or) documents indirectly confirming the expenses incurred. expenses (including customs declaration, business trip order, travel documents, report on work performed in accordance with the contract). Any expenses are recognized as expenses, provided that they are incurred to carry out activities aimed at generating income.

According to paragraph 2 of Art. 252 of the Tax Code of the Russian Federation, expenses, depending on their nature, as well as the conditions for implementation and areas of activity of the taxpayer, are divided into expenses associated with production and sales, and non-operating expenses.

Based on Art. 255 of the Tax Code of the Russian Federation, the taxpayer’s expenses for wages include any accruals to employees in cash and (or) in kind, incentive accruals and allowances, compensation accruals related to working hours or working conditions, bonuses and one-time incentive accruals, expenses associated with the maintenance of these employees who are provided for by the legislation of the Russian Federation, labor agreements (contracts) and (or) collective agreements.

Thus, the list of labor costs given in Art. 255 of the Tax Code of the Russian Federation is open.

According to paragraph 6 of Art. 255 of the Tax Code of the Russian Federation, labor costs include, in particular, the amount of average earnings accrued to employees, retained for the duration of their performance of state and (or) public duties and in other cases provided for by the labor legislation of the Russian Federation.

In accordance with Art. 166 of the Labor Code of the Russian Federation, a business trip is recognized as a trip by an employee by order of the employer for a certain period of time to carry out an official assignment outside the place of permanent work.

Article 167 of the Labor Code of the Russian Federation establishes that when an employee is sent on a business trip, he is guaranteed to retain his place of work (position) and average earnings, as well as reimbursement of expenses associated with the business trip.

Billing period and number of days in it

As we said above, the billing period includes 12 full calendar months preceding the month in which the employee should be paid based on his average earnings. The company has the right to establish any other duration of the billing period. For example, 3, 6 or 24 months preceding payment. The main thing is that a different calculation period does not lead to a reduction in the amounts due to the employee (that is, does not worsen his situation compared to the 12-month calculation period).

If the company decides to change this period, the corresponding provisions must be enshrined in collective agreements or in the wage regulations.

Example

Employee of Salyut JSC Ivanov is going on a business trip. He is paid an average salary for the days of his business trip. Let's assume that this year Ivanov left:

– in February - the settlement period from February 1 of last year to January 31 of the current year;

– in March - the settlement period from March 1 of last year to February 28 (29) of the current year;

– in April - the billing period from April 1 of last year to March 31 of the current year;

– in May - the settlement period from May 1 of last year to April 30 of the current year;

– in June - the settlement period from June 1 of last year to May 31 of the current year;

– in July - the billing period from July 1 of last year to June 30 of the current year.

Next, you need to calculate the number of working days in the billing period during which the person worked. The optimal, but rather rare option is if all working days in the billing period were worked out in full. In this case, counting does not cause any difficulties.

Example

ZAO Salyut has a five-day, 40-hour work week (8 working hours per day) with two days off (Saturday and Sunday). In November of this year, company employee Ivanov was sent for training in order to improve his skills and maintain his average earnings. The billing period is 12 months - from November 1 of the previous year to October 31 of the current year.

Suppose that the number of working days in the billing period according to the production calendar

is (all days worked in full by Ivanov):

| Month included in the billing period | Number of working days in the billing period |

| Last year | |

| November | 21 |

| December | 22 |

| This year | |

| January | 16 |

| February | 20 |

| March | 21 |

| April | 21 |

| May | 21 |

| June | 20 |

| July | 22 |

| August | 23 |

| September | 20 |

| October | 23 |

| Total | 250 |

We have given a perfect example. As a rule, no company employee works 12 months (payroll period) in full. Employees get sick, go on vacation, receive various releases from work while maintaining average earnings, etc. All these periods are excluded from the calculation. Also, the amounts accrued in favor of the employee during these days will not be included in the calculation. The list of time periods excluded from the calculation is given in paragraph 5 of the Regulations. These are the periods during which:

– the employee retained his average earnings in accordance with Russian legislation (for example, the employee was on a business trip, on annual paid leave, was sent for training, etc.) (with the exception of breaks for feeding a child provided under Article 258 of the Labor Code of the Russian Federation; such periods are included in the calculation, as well as the amounts accrued for them);

– the employee did not work and received temporary disability benefits or maternity benefits;

– the employee did not work due to downtime due to the fault of the employing company or for reasons beyond the control of the employer and employee;

– the employee did not participate in the strike, but due to it he could not perform his work;

– the employee was provided with additional paid days off to care for disabled children and people with disabilities since childhood;

– the employee in other cases was released from work with full or partial retention of salary or without it (for example, while on leave at his own expense) in accordance with Russian legislation.

Holidays or weekends on which the employee worked must be taken into account when calculating average earnings in the general manner.

Example

ZAO Salyut has a five-day, 40-hour work week (8 working hours per day) with two days off (Saturday and Sunday). In December of this year, company employee Ivanov was sent on a business trip. The billing period is 12 months. Therefore, it includes the time from December 1 of the previous year to November 30 of the current year.

The following data is reflected in the work time sheet for Ivanov.

Situation 1

| Month of billing period | Number of working days in the billing period according to the production calendar | Number of working days actually worked by the employee | The time during which the employee did not work or the average salary was maintained (in working days) | Note |

| Last year | ||||

| December | 22 | 22 | – | – |

| This year | ||||

| January | 16 | 16 | – | – |

| February | 20 | 15 | 5 | The employee was sick and received temporary disability benefits |

| March | 21 | 21 | – | – |

| April | 21 | 14 | 7 | The employee was on a business trip |

| May | 21 | 21 | – | – |

| June | 20 | 20 | – | – |

| July | 22 | 19 | 3 | The employee was sick and received temporary disability benefits |

| August | 23 | 3 | 20 | The employee was on annual paid leave |

| September | 20 | 20 | – | – |

| October | 23 | 21 | 2 | The employee was on vacation at his own expense |

| November | 21 | 21 | – | – |

| Total | 250 | 213 | 37 | – |

When determining Ivanov’s average earnings, 37 days and the payments accrued for them are excluded from the calculation period. Therefore, 213 (250 – 37) days worked in the payroll period are included in the calculation.

Situation 2

| Month of billing period | Number of working days in the billing period according to the production calendar | Number of days actually worked by the employee | The time during which the employee did not work or the average salary was maintained (in working days) | Working on holidays or weekends | Note |

| Last year | |||||

| December | 22 | 22 | – | – | – |

| This year | |||||

| January | 16 | 19 | – | 3 | The employee worked on holidays |

| February | 20 | 15 | 5 | – | The employee was sick and received temporary disability benefits |

| March | 21 | 21 | – | – | – |

| April | 21 | 14 | 7 | – | The employee was on a business trip |

| May | 21 | 21 | – | – | – |

| June | 20 | 22 | – | 2 | The employee worked on weekends |

| July | 22 | 19 | 3 | – | The employee was sick and received temporary disability benefits |

| August | 23 | 3 | 20 | – | The employee was on annual paid leave |

| September | 20 | 21 | – | 1 | The employee worked on a day off |

| October | 23 | 21 | 2 | – | The employee was on vacation at his own expense |

| November | 21 | 21 | – | – | – |

| Total | 250 | 219 | 37 | 6 | – |

When determining Ivanov’s average earnings, 37 days and the payments accrued for them are excluded from the calculation period. At the same time, days worked on a holiday or day off and payments accrued for them are taken into account (6 days). Therefore, 219 (250 – 37 + 6) days worked in the payroll period are included in the calculation.

There are situations when an employee gets a job within the reporting period. That is, at the time when the accountant needs to determine his average earnings, he has not worked for the company for a billing period (for example, 12 months). There is no procedure for calculating average earnings for situations not related to paid vacations. Therefore, the company has the right to define it in the employment contract with the employee or in the salary regulations. Then in the billing period you can include the time from the first day of work of the employee until the last day of the month that precedes the payment of average earnings.

Example

ZAO Salyut has a five-day, 40-hour work week (8 working hours per day) with two days off (Saturday and Sunday). The billing period is 12 months.

In December of this year, company employee Ivanov was sent on a business trip. At the same time, he got a job at the company on August 22 of this year. In this situation, the calculation period includes the time from August 21 to November 30 of the current year.

The following data is reflected in the work time sheet for Ivanov.

| Month of billing period | Number of working days in the billing period according to the production calendar | Number of days actually worked by the employee | The time during which the employee did not work or the average salary was maintained (in working days) | Working on holidays or weekends | Note |

| August | 23 | 8 | – | – | From August 1 to August 21, the employee did not work for the company |

| September | 20 | 22 | – | 2 | The employee worked on a day off |

| October | 23 | 19 | 4 | – | The employee was on vacation at his own expense |

| November | 21 | 21 | – | – | – |

| Total | 87 | 70 | 4 | 2 | – |

In this case, from the total number of working days according to the production calendar (from the moment the employee was hired to the month preceding the month of payment of the average salary), the time when he did not work at the company (15 days of August) and 4 days of unpaid leave are excluded. At the same time, days worked on a holiday or day off and payments accrued for them are taken into account (2 days). Therefore, 70 (87 – 15 + 2 – 4) days worked are included in the calculation.

How to calculate average earnings when paying benefits

Calculate the average monthly salary when paying vacation pay, various benefits - days off, unemployment, temporary disability, pregnancy and childbirth, as well as during the training period of employees. For this:

- determine the billing period;

- determine payments that exceed the official salary or salary according to the tariff in the billing period (above-tariff payments);

- divide the above-tariff payments by the number of months of the billing period;

- add the resulting amount to the official salary (or to the salary according to the tariff) on the day of calculation. This will be the average monthly salary.

You can use the following formula:

Average monthly salary = Official salary (salary according to tariffication) on the day of calculation + 1/12 (or 1/11, 1/10, 1/9, 1/8, 1/7, 1/6, etc.) payments, exceeding the official salary (salary according to tariffs) in the billing period

Example Calculation of average monthly wage as the sum of salary and average additional payments

The employee was ill in April 2021 and has a certificate of temporary incapacity for work. His salary in April 2021 is 3,500,000 soums. For the billing period - from April 2021 to March 2021 - the employee was additionally accrued in addition to the salary:

(in total)

| Months of the billing period | Payments in excess of the official salary, for which insurance premiums are calculated (from January 1, 2021 - income in the form of wages)* |

| April 2021 | – |

| May 2021 | – |

| June 2021 | – |

| July 2021 | – |

| August 2021 | 1 000 000 |

| September 2021 | – |

| October 2021 | – |

| November 2021 | 1 000 000 |

| December 2021 | 1 200 000 |

| January 2021 | – |

| February 2021 | – |

| March 2021 | 1 600 000 |

| Total | 4 800 000 |

* Payments in excess of the official salary, on which insurance contributions are calculated, should be understood as income in the form of wages, subject to social tax (insurance contributions have been abolished since 2021).

The average monthly salary is calculated as follows:

3,500,000 + 4,800,000: 12 = 3,900,000 sum.

When you may need to pay extra to average earnings

The maximum amount of disability benefits is limited by the maximum base for contributions to VNIM. In addition, its size is influenced by the employee’s insurance period. As a result, the benefit amount cannot be more than the amount calculated using the formula:

(Amount of the maximum base value for calculating insurance premiums for VNiM for the calculated calendar years / 730) × Sick leave percentage, depending on length of service |

Thus, a situation where the amount of sick leave is lower than the employee’s usual earnings is possible under the following conditions:

- lack of insurance period necessary for 100% payment;

- annual income exceeds the maximum size of the base for contributions to the Social Insurance Fund;

- the simultaneous presence of both of these conditions.

In such circumstances, the employer is given the right to decide on additional payment up to average earnings.

Concept

Supplementation to average earnings is a procedure in which, if the employee’s income level decreases, the employer pays him an additional amount of money, thanks to which the employee’s salary will reach the average value.

For example, when paying for sick leave, it often turns out that payment is due for temporary disability benefits, the amount of which is significantly lower than the regular salary of a working citizen.

It is for this purpose that some employers transfer an additional amount to the employees’ account.

The decision on additional payment is made by the company’s management independently.

Money paid in addition to sick leave is not compensated by the Social Insurance Fund - the money is taken from the company’s budget.

A similar situation may arise when an employee is transferred to a position in which the citizen’s salary will change for the worse.

It is important to remember that the salary cannot be lower than the minimum wage. Failure to comply with this rule may be considered a violation of the Labor Code of the Russian Federation.

Additional sick pay up to average earnings

Often, sick pay is significantly less than earnings. The employer company can compensate for the resulting difference at its own expense. Such an action is not the responsibility of the employer and is carried out solely on his initiative.

In order for additional payments for sick leave to be taken into account as part of costs, it is necessary to stipulate an obligation to compensate for the difference between the actual benefits and average earnings in the collective agreement. It should clearly indicate the cases in which additional payment will be made. For example, an employer can pay the difference only if the employee was sick himself and was not caring for a child or a sick family member. The terms of compensation must also be set out in the employment contract.

What happens if you don’t pay extra to the “minimum wage”

If the management of an organization does not have the desire or ability to make an additional payment to an employee up to the minimum wage when it is obliged to do so, it automatically puts itself at risk. An employee has the right to complain about such an employer to the labor inspectorate, prosecutor's office or court.

As a punishment for violating the current labor legislation, an administrative fine is provided for the enterprise and senior officials.

Thus, increasing wages to the “minimum wage” in situations established by law is absolutely necessary. And for this you need to carry out a number of mandatory procedures.

Let's understand the situation

The amount of payment for sick leave (SL) depends not only on the employee’s length of service and income level over the last two years. The reason for the illness also affects the amount of payment. So, for example, a maternity leaver is entitled to pay 100% of the amount, but an ill employee with less than 5 years of work experience will be paid only 60% of the average daily earnings.

To further encourage specialists or support them during illness, some employers establish an additional payment up to the average salary on sick leave. What is the essence of this payment? In other words, if, when calculating sickness benefits, an employee is entitled to payments less than his average earnings, then additional charges are made from the employer’s wage fund.

This additional payment up to the average salary for sick leave is the sole expense of the employer. That is, it will not be possible to receive compensation from the Social Insurance Fund for such additional charges.

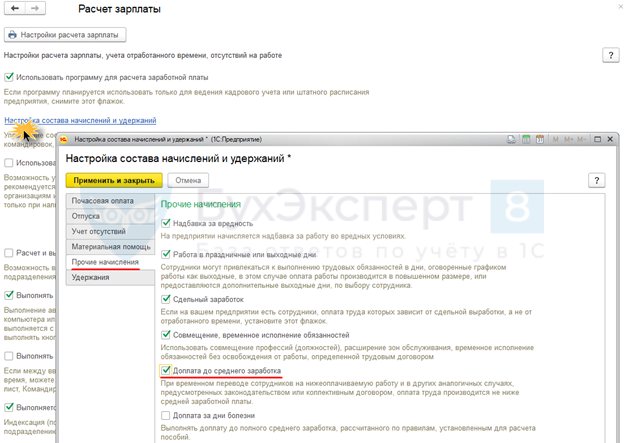

Additional payment up to average earnings

The feature is enabled by checking the Additional payment up to average earnings in the salary calculation settings (Settings - Payroll calculation - Setting up the composition of accruals and deductions - Other accruals tab).

An additional payment is assigned using the document Order for additional payment based on average earnings (HR - Changes in employee pay - Order for additional payment up to average earnings):

Features of working with the document:

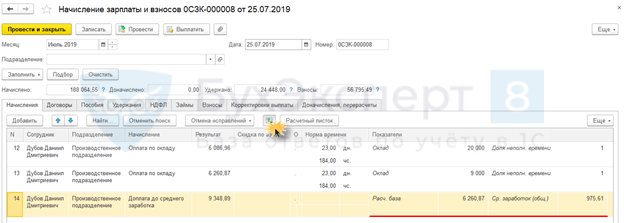

The calculation of the Supplement up to average earnings occurs in the document Calculation of salaries and contributions :

By clicking the Show calculation details , you can see the data used in the calculation:

Features of calculating Additional payments up to average earnings :

- The calculation base for the Supplement to Average Earnings includes all accruals for the period of validity of the surcharge that are included in the average earnings;

- If the surcharge is NOT valid for a full month, and there is an accrual for a full month, then it will be included in the calculation base in proportion to the period;

- The additional payment up to the average earnings is itself included in the average earnings;

- Average earnings are calculated monthly and may change accordingly;

- “Eats up” accruals for overtime work: they are included in the calculation base, but do not increase the number of days/hours for which additional payment occurs.

Let's consider the last point in more detail.

The problem of paying for work on a holiday or day off with additional payment up to average earnings

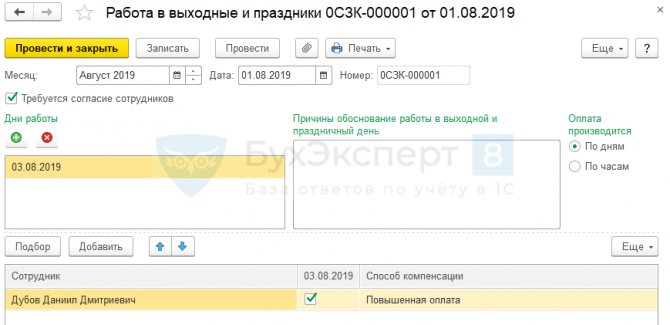

Modeling the problem of paying for work on a holiday or day off with “Additional payment up to average earnings”

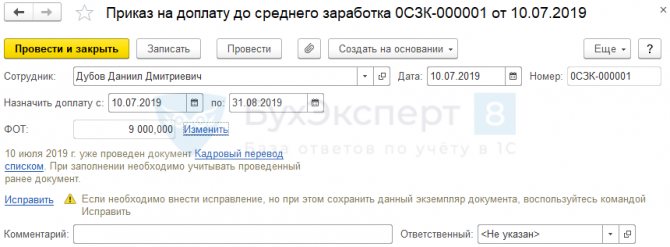

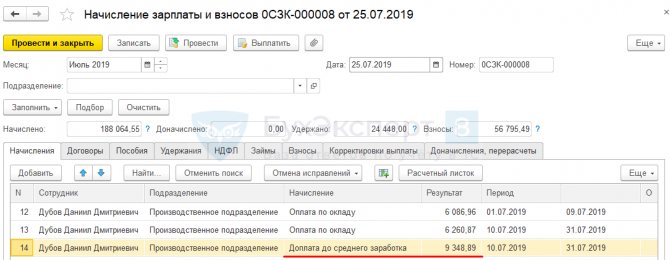

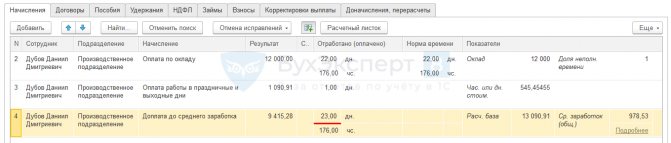

Employee Dubov D.D. was introduced for additional payment up to average earnings for the period from 07/10/2019 to 08/31/2019. On August 3, 2021, the employee is required to work on his day off. This fact is registered in the program by the document Work on weekends and holidays (Salary – Work on weekends and holidays – Work on weekends and holidays):

At the same time, the cost per day to pay for work on a weekend or holiday for an employee is 545.45455 rubles, and the average daily earnings is 978.53 rubles.

August Dubov D.D. worked completely. In the document Calculation of salaries and contributions, the following calculations were made for the month:

The salary was equal to:

- 12,000 (Salary for a full month) /22 (Normal days) *22 (Working time in days) = 12,000 rubles.

Payment for work on holidays and weekends was:

- 545.45455 (Day cost) * 1 (Number of days off worked) = RUB 1,091.91.

The supplement to average earnings was calculated in the amount of:

- 978.53 (Average daily earnings) * 22 (Number of days worked) - (12,000 (Amount of payment based on salary) + 1,091.91 (Amount of payment for work on holidays and weekends) = 8,436.75 rubles.

Thus, the amount of remuneration for work on holidays and weekends was included in the calculation base of the additional payment up to the average earnings and the amount of the additional payment decreased. As a result, the total amount of accruals for the month turned out to be the same as if the employee had not worked on a day off.

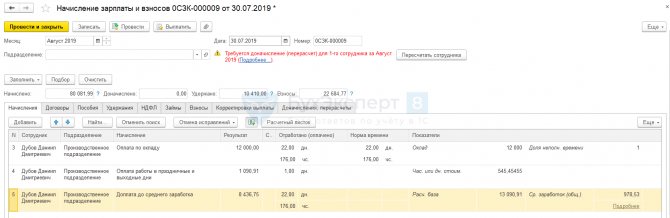

Adjusting the “Additional payment up to average earnings” accrual settings to correct the situation

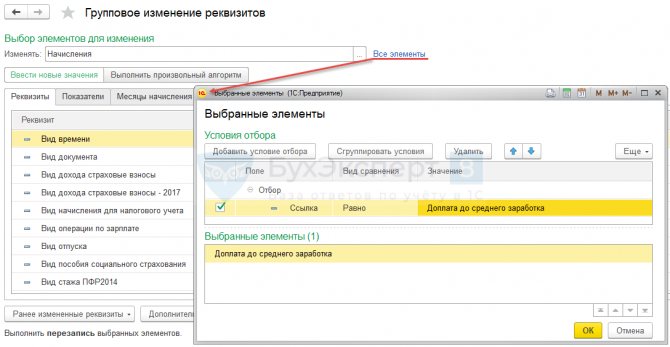

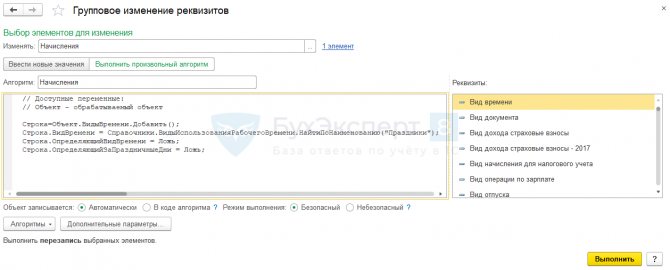

Let's adjust the accrual settings for Additional payments to average earnings using the Group change of details (Administration - Maintenance - Data adjustment - Group change of details).

In processing, in the Change Accruals as an object Link field to change only the Additional payment to average earnings :

Then click on the Run custom algorithm :

We need to add the time type Holidays to the Time Types . This can only be done through an arbitrary algorithm.

In the text field you should write the following text:

Row = Object.TimeTypes.Add(); Line.Type of Time = Directories.Types of Use of Working Time.Find By Name("Holidays"); String.DefiningTimeType = False; String.DefiningForHolidays = False;

And then click the Run .

As a result, when calculating the Supplement to average earnings, the time worked on a day off will be taken into account:

Setting up the accrual type

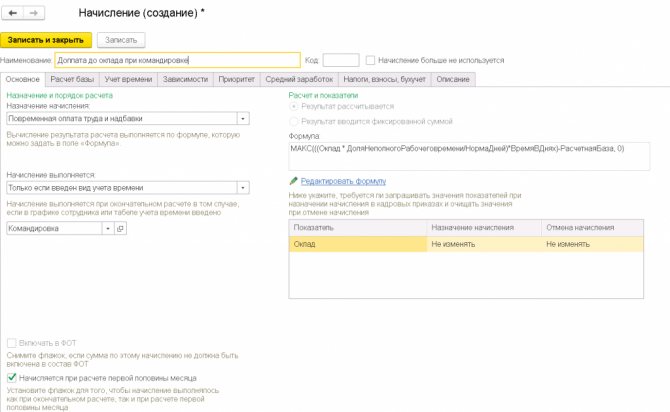

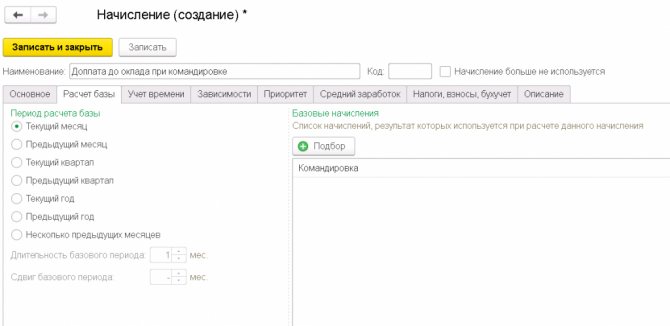

To calculate an additional payment before salary during a business trip, you need to create a new type of accrual in the ZUP. 1. Section Settings – Accruals.

2. Click on the

Create

.

3. In the Name

, fill in the name of the accrual type: Additional payment to salary for a business trip.

4. In the Code

, enter the accrual type code (it must be unique).

5. On the Main

:

- in the section Purpose and calculation procedure, in the Purpose of accrual field, select the value Time-based wages and allowances. In the Accrual is performed field, select the value Only if the type of time recording is entered (select the Business trip type from the Types of use of working time directory). This means that the additional payment up to the salary will be automatically accrued to the employee when calculating the salary in the document Calculation of salaries and contributions in case of registration of the document Business trip for this employee

- In the Calculation and indicators section, the switch is set to the Result is calculated position by default. Click the Edit formula link to open the formula editor and describe the calculation formula:

MAX(((Salary*Share of Part-time Working Time/NormDays)*TimeInDays)-CalculatedBase, 0)

Where:

Salary * Share of Part-Time Worker / NormDays - payment based on salary for one day TimeInDays - the number of days on a business trip CalculationBase - the sum of the results of accruals for the current month indicated on the Calculation of the base tab. . This formula compares salary and payment based on average earnings during the business trip. If the salary is greater than the average earnings during the business trip, then the additional payment is equal to their difference; if not, the value is zero. 6. The tabular part is filled in automatically with the Salary

.

7. On the Base calculation

(the tab is available if the formula uses the CalculationBase indicator, i.e., when calculating accruals, the results of calculating other accruals are assumed): 8. In the

Base calculation period

, indicate the period for which the results of calculating base accruals should be used.

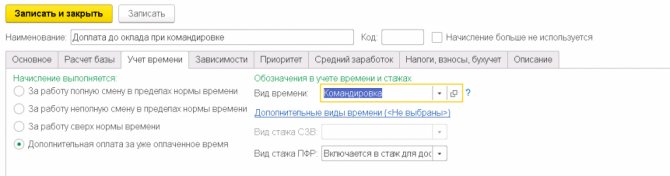

9. On the Time Tracking

set the switch to the

Additional payment for already paid time

and specify the type of time Business trip.

10. On the Dependencies

indicate the accruals and deductions (depending on this accrual), the calculation base for which includes this accrual.

11. On the Priority

, specify which accruals should be performed instead of the current one, or indicate the accruals instead of which the current one is performed. As a rule, these tables are filled in automatically by the program based on the results of an analysis of the main accrual parameters. By default, the accrual type Business trip has high priority and supersedes other accruals. From the list of Accruals whose priority is higher, remove the accrual type Business trip. Otherwise, the business trip will displace the additional payment to the salary for the business trip when it is calculated in the document Calculation of salaries and contributions. In turn, from this list (it will be offered at the time of recording the accrual type), it is necessary to remove accrual types for which the accrual type Business trip is specified as a displacing accrual type (the list will be available via the link Accrual priority is incorrectly configured).

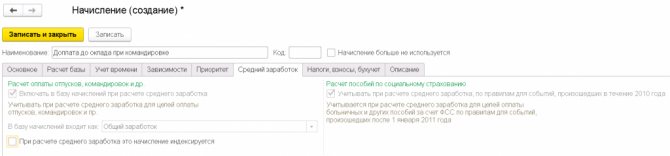

12. On the Average earnings

sections Calculation of payment for vacations, business trips, etc. and Calculation of social insurance benefits are not available for editing.

Uncheck the box When calculating average earnings, this accrual is indexed. According to the letter of the Ministry of Labor of Russia dated August 13, 2015 No. 14-1/B-608, when calculating average earnings, accruals made during a business trip are not taken into account. In the future, when calculating average earnings, this accrual and the period for which it was accrued will not be taken into account. If a business trip is canceled or corrected in future periods, then the accruals that fell during its original period will still not be taken into account in calculating average earnings. 13. On the Taxes, fees, accounting

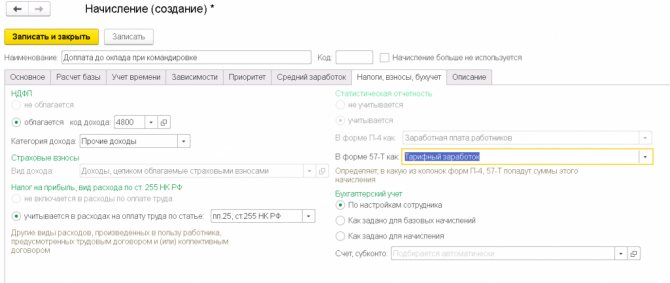

:

- in the personal income tax section, the switch is set by default to the taxable position and in the income code field the code 4800 “Other income” is indicated

- in the Insurance premiums section, the Type of income field by default indicates the type of income from the point of view of taxation of insurance premiums - Income entirely subject to insurance premiums, which also corresponds to this accrual

- in the Income Tax section, type of expense under Art. 255 of the Tax Code of the Russian Federation, set the switch to the position taken into account in labor costs under the item and select paragraphs. 25, art. 255 of the Tax Code of the Russian Federation, if additional payment to the salary during a business trip is provided for by the organization’s remuneration system (how), see letter of the Ministry of Finance of Russia dated 06/03/2013 No. 03-03-06/1/20155, etc.

- in the Statistical Reporting section in the field In Form 57-T, indicate Tariff Earnings

- in the Accounting section - if an additional payment before salary during a business trip is provided for by the organization’s remuneration system, then accrual expenses are taken into account in the “usual” way - As specified for the employee (i.e., the posting for this accrual will be generated similarly to that generated for the main accrual employee, for example, Dt 26 Kt 70). The method of reflection is indicated in the form called up by clicking the Payments, cost accounting link from the employee’s card (section Personnel - Employees). The switch should be set to the As specified position for accrual only when accrual is reflected in accounting in the same way for all employees. In this case, in the Account, subconto field, you need to select a value from the Methods of reflecting salaries in accounting directory (section Settings - Method of reflecting salaries in accounting). If the corresponding method of reflection is not available in the directory, it must be created. Elements of the directory Methods for reflecting salaries in accounting are synchronized with the elements of the directory of the same name in the 1C: Accounting 8 program (rev. 3.0). In the program “1C: Salaries and Personnel Management 8” (rev. 3), the elements of this directory are characterized only by name; in the program “1C: Accounting 8”, for each method of reflection in accounting, the debit of the account and the analytics are additionally indicated, on the basis of which in the accounting program accounting and tax accounting entries are generated.

14. On the Description

In the

Short name

, you can specify a short name for the accrual. It will be displayed in various accrual reports. On the same tab you can also fill out a custom description of the accrual for reference.

Paying taxes on surcharges and reflecting them in accounting

The amount of additional payment up to average earnings fully subject to personal income tax and insurance contributions (clause 1 of Article 209, subclause 1 of clause 1 of Article 420 of the Tax Code of the Russian Federation).

If the procedure for its formation is fixed in the local act of the company, it can be taken into account in its entirety in income tax expenses.

In accounting, the additional payment should be reflected as expenses for ordinary activities in correspondence to the debit of the expense account (26, 44, 20, 23, 25 ) and the credit of account 70 .

When is it necessary to calculate the additional payment up to the average monthly earnings?

The procedure for remuneration of workers temporarily transferred due to health damage as a result of an insured event to easier, lower-paid work is determined by the Regulations on insurance activities in the Republic of Belarus, approved by Decree of the President of the Republic of Belarus dated August 25, 2006 No. 530 (hereinafter referred to as Regulation No. 530).

An insured person who is temporarily transferred due to health damage as a result of an insured event to an easier, lower-paid job is paid the difference between the average monthly earnings at the previous job and the earnings at the new job until his professional ability to work is restored or its permanent loss is established (clause 297 of Regulation No. 530) .

A conclusion on the need for such a temporary transfer to another job, its duration and the nature of the recommended work is issued by a medical advisory commission (MCC).

Important! If the policyholder has not provided the insured employee with relevant work during the specified period, then he pays him the average monthly earnings received before the insured event, at the expense of the policyholder’s own funds.

How is average monthly earnings determined?

To determine the amount of the insurance payment - an additional payment up to the average monthly earnings - the average monthly earnings are determined from earnings for the 2 months preceding the month in which the insured event occurred, in the manner prescribed by law (part four, clause 297 of Regulation No. 530).

In this case, the procedure established by law is Instruction No. 47. In general, to determine the average monthly earnings for the previous job (when all working days have been worked), it is necessary to determine the accounting earnings for the billing period and divide it by 2.

When calculating average earnings, the accrued wages are taken into account, taking into account the payments provided for in clause 1 of the List of payments taken into account when calculating average earnings (Appendix to Instruction No. 47) (hereinafter referred to as the List).

What payments are included in the calculation of average monthly earnings?

Of the payments provided for in clause 1 of the List, only those types of actually accrued income for which contributions to Belgosstrakh were calculated are included in the calculation of average monthly earnings (part three of clause 12 of the resolution of the Plenum of the Supreme Court of the Republic of Belarus dated December 22, 2005 No. 12 “On some issues application by courts of legislation on compulsory insurance against accidents at work and occupational diseases").

Payments not taken into account when calculating include average earnings saved for unworked time (period):

- during vacations;

– time for performing government duties;

– additional day off from work, etc. (clause 2 of the List).

Thus, when calculating the additional payment up to the average monthly earnings, it is necessary to take into account only the payments included in clause 1 of the List. An exception is the payments provided for in clause 3 of the List, for which contributions to Belgosstrakh were (should have been) accrued.

For reference: List of payments that are not subject to contributions for state social insurance, including professional pension insurance, to the budget of the state extra-budgetary fund for social protection of the population of the Republic of Belarus and for compulsory insurance against industrial accidents and occupational diseases to the Belarusian Republican Unitary Insurance the Belgosstrakh enterprise was approved by Resolution of the Council of Ministers of the Republic of Belarus dated January 25, 1999 No. 115 (hereinafter referred to as List No. 115).

Payments are taken into account in the month in which they are accrued, i.e. reflected in the employee’s personal account and payslip.

Example

Temporary transfer as a result of an insured event to an easier job and calculation of additional payment

An employee who suffered an accident at work on November 13, 2021, starts work on December 18, 2021. The conclusion of the High Work Commission indicates the need for a temporary transfer for a period of 2 months to another, easier job due to damage to health caused by the accident in production. By order of the manager, the employee was transferred to a lower-paid job, the conditions of which correspond to the conclusion of the Higher Quality Commission.

The employee works on a 5-day workweek schedule and worked all working days in September and October 2021.

He was credited:

- in September:

according to the established salary - 440 rubles;

one-time payment in connection with the 40th anniversary - 70 rubles;

- in October:

according to salary - 440 rubles.

The amount of accrued salary for lower-paid work for the period December 18–31, 2021 is 150 rubles.

The amount of earnings taken into account when calculating average monthly earnings is 880 rubles. (440 + 440). A one-time payment in connection with the 40th anniversary is not included in the calculation, since it is of a social nature (clause 3 of the List). The average monthly salary from my previous job is 440 rubles. (880 / 2). Average earnings for 9 days in December – 198 rubles. (440 / 20 working days × 9 days).

The amount of additional payment up to average earnings is 48 rubles. (198 – 150).

Accounting and Taxation

Calculations for insurance of property and employees of the organization (except for calculations for social insurance and security) are reflected in subaccount 76-2 “Calculations for property and personal insurance”.

The amounts of additional payments paid by the policyholder up to the average monthly earnings of the insured are counted towards the payment of insurance premiums or are reimbursed by the insurer in the manner established by it.

In the accounting records of an organization, correspondence is compiled:

D-t 76-2 – K-t 70 – 48 rub. – the amount of the accrued surcharge;

D-t 70 – K-t 51 – 48 rub. – transfer of additional payment to the employee.

When determining the tax base for income tax, is not taken into account (subclause 1.1.1, clause 1, article 158 of the Tax Code of the Republic of Belarus).

are not charged from the amount of the surcharge (clause 6 of List No. 115).