Count 20

All direct expenses are accumulated on active account 20 “Main production”, reflected in the debit of its account in correspondence with accounts 02, 05, 10, 11, 21, 60, 69, 70 and others. Expenses of auxiliary production are first collected in the debit of accounts 23, 25, 26 and 28, from where they are then transferred to account 20.

The actual production cost of finished products, work performed, services provided in correspondence with the accounts is written off from the credit of account 20:

- 43 “Finished products” - if the products are delivered to the warehouse;

- 45 “Goods shipped” - if the products are shipped to the buyer directly from production, the proceeds from the sale of which cannot be recognized immediately;

- 90 “Sales” - if products are sold from production.

Account balance 20 accounts - reflects the cost of the main work in progress.

Account 25 “General production expenses”

Let us recall that general production costs are the costs of servicing the main and auxiliary production facilities of the organization.

General production expenses are accounted for on account 25 “General production expenses” (Order of the Ministry of Finance dated October 31, 2000 No. 94n).

General production costs are collected in the debit of account 25 from the credit of accounts for accounting for inventories, settlements with employees for wages, etc. In fact, accounting for general production and general business expenses in terms of reflection in the debit of accounts 25 and 26 “General business expenses” is similar. The difference is only in the composition of costs, which can be included in the composition of general production or general economic costs of the organization.

The most typical example of overhead costs is the costs of a workshop in which several types of products are produced.

Here are the most typical transactions for general production expenses:

| Operation | Account debit | Account credit |

| Accrued depreciation of general production equipment | 25 | 02 “Depreciation of fixed assets” |

| Materials written off for general production purposes | 25 | 10 "Materials" |

| Wages accrued to general production employees | 25 | 70 “Settlements with personnel for wages” |

| Insurance premiums have been calculated for the wages of general production employees. | 25 | 69 “Calculations for social insurance and security” |

| Reflected expenses for insurance of general production property | 25 | 76 “Settlements with various debtors and creditors” |

| Provided third-party general production services | 25 | 60 “Settlements with suppliers and contractors” |

Why is count 25 needed?

For the answer, please refer to the Instructions for using the Chart of Accounts. It states that this account is intended to summarize information on the costs of servicing the organization’s main and auxiliary production facilities. Consequently, costs from account 25 are distributed to accounts 20 and 23. Let us highlight expenses that can be taken into account in the overhead costs account, as well as the corresponding corresponding accounts.

| Types of costs accumulated on account 25 | Sources of financing costs |

| For the maintenance and operation of machinery and equipment, including: | 10, 70, 69 |

| – depreciation charges for property used in production | 02 |

| – costs for repairs of fixed assets and other property | 10, 70, 69 |

| Costs of insuring this property | 76 |

| Costs for heating, lighting and maintenance of premises | 60 |

| Rent for premises, machinery, production equipment | 60, 76 |

| Remuneration of workers engaged in production maintenance | 70, 69 |

The table shows the main expenses accumulated on account 25. In fact, there are more of them - the text of the Instructions for using the Chart of Accounts states that correspondence on the debit of the account includes more than two dozen accounts. The credit of account 25 corresponds to half as many accounts, of which there are only three main ones: 20 “Main production”, 23 “Auxiliary production”, 29 “Service production and farms”. Accounts 10 “Materials”, 23 “Defects in production”, 76 “Settlements with various debtors and creditors”, 99 “Profits and losses” can become additions to them. Analytical accounting for account 25 is carried out for individual divisions and expense items.

The reader has the right to say that the Instructions for the Application of the Chart of Accounts are not the document on the basis of which the accounting policy of the organization can be based. The author agrees with this and therefore suggests turning to the so-called costing documents, which provide for calculating the cost of products based on the costs of the enterprise.

Account 25 in accounting

Like all expense accounts, it is active and has no balance at the end of the reporting period. Expenses on account 25 are indirect, that is, it takes into account costs the cost of which cannot be directly attributed to specific types of products.

The list of expenses collected on account 25 contains the following expenses:

- employee salaries;

- administrative expenses;

- business trips;

- insurance premiums;

- maintenance of production equipment;

- maintenance and repair of buildings, production systems;

- maintenance of production facilities;

- production losses, etc.

Analytical accounting of overhead costs is broken down by department and cost item.

The account may not be used if the organization has a limited number of items produced. In this case, it is sufficient to use accounts 20 and 23. But for many organizations, the use of indirect costs is more profitable from the point of view of calculating profit.

To calculate the profit, direct and indirect costs are taken. Indirect expenses, including account 25, are written off completely, which reduces income tax.

Amounts on account 25 do not participate in the formation of cost; they are written off to accounts 20, 23 and 29. The write-off methodology and distribution procedure are fixed by the enterprise in its accounting policies.

Subaccounts

Sub-accounts can be opened to the “General production expenses” account:

- 25.01 — “Maintenance and operation of equipment”;

- 25.02 — “General shop expenses.”

In this case, the first subaccount takes into account and monitors the implementation of the cost estimate for maintaining and ensuring the operability of the equipment. For construction organizations, this equipment is construction machines and other mechanisms.

Get 267 video lessons on 1C for free:

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- Good course on 1C Trade Management 11.

General production (general shop) expenses include the costs of management and maintenance of structural units of the main and auxiliary production.

Cost Allocation

Costs of account 25 are distributed to accounts 20, 23 and 29 by type of product in proportion to the established base. The distribution base for indirect costs is determined in accordance with methodological recommendations developed for various industries.

The choice of distribution methodology from an accounting perspective is selected depending on the reporting purposes. The least labor-intensive method is most often used - the distribution of indirect costs by a common base.

Typical postings for account 25

What applies to general production expenses (account 25)

Account 25 in accounting is active, and its debit accumulates the costs of servicing the main and auxiliary production.

| What is going to the account? 25 | Sources of costs |

| Depreciation of property occupied in the process | 02 |

| Costs for repairing OS and other property | 10, 70, 69 |

| "Utilities", transport and other costs from suppliers and sellers | 60 |

| Rental payments for premises, machinery and equipment used in the production process | 60, 76 |

| Employees' salaries with deductions | 70, 69 |

| Equipment insurance | 76 |

The loan shows the distribution of the expenses collected per month on the account. 20, 23 and 29.

Analytical accounting is organized for each division and type of expense.

What relates to account 25 can be found out from the basic provisions on the calculated cost at industrial enterprises, according to which ODA is divided into:

- production - this is the maintenance of the management staff and other workshop personnel, depreciation, maintenance and ongoing repairs of buildings, labor protection, etc.;

- non-productive - losses from downtime, shortages and damage to material assets, etc.

What are overhead costs

Production of products involves direct expenses (for raw materials, equipment, wages, etc.), as well as indirect expenses. In addition to the costs directly for the manufacture of products, funds must be spent on the organization of this process itself; it must be continuously managed, regulated, and at all production levels (management of a team, workshop, department, site, line, etc.).

Funds spent on organizing and managing the production process in all structural divisions of the organization are considered general production expenses. Previously, this type of expense was called “shop expenses.”

IMPORTANT INFORMATION! In the current situation, the national accounting system is gradually being brought in line with international market standards. Related to this is the revision of the mechanisms for the formation of ODA in domestic accounting. In this article we consider only current provisions.

A little about the classification of costs.

All production costs are included in the cost of individual types of products, works and services (including products manufactured to individual orders) or groups of homogeneous products. Depending on the methods of inclusion in the cost of certain types of products, costs can be direct and indirect. Direct costs are understood as expenses associated with the production of certain types of products (raw materials, basic materials, purchased products and semi-finished products, basic wages of production workers, etc.), which can be directly and directly included in the cost of goods. Indirect costs are those associated with the production of several types of products (maintenance and operation of equipment, workshop, general plant expenses, etc.), included in the cost of goods using special methods.

In the Basic Provisions for Calculating Product Costs at Industrial Enterprises[1], shop and general plant expenses are identified in the grouping of costs by item. Which of them should include “modern” general production costs? To answer the question, we will give a comparative description of these expenses.

| Expenses included in the cost of manufactured products | |||

| ⇓ | ⇓ | ||

| Shop expenses | Factory overhead | ||

| ⇓ | ⇓ | ||

| Costs of industrial and production structural divisions of the enterprise | Costs of enterprise management and production organization in general | ||

| ⇓ | ⇓ | ||

| Salaries of shop management staff; depreciation and costs of maintenance, current repairs of buildings, structures and equipment for general workshop purposes; costs of experiments, research, rationalization and invention of a workshop nature; costs of labor protection measures; other workshop costs associated with production management and maintenance | Salaries of plant management personnel with deductions; expenses for business trips and lifting expenses when moving employees, for official travel and maintenance of passenger vehicles; telephone expenses; costs of maintenance and ongoing repairs of buildings, structures and general plant equipment; taxes, fees and deductions, enterprise security costs | ||

It is clear from the diagram that general production expenses correspond to shop expenses in the interpretation of the Basic Provisions for Calculating Product Costs at Industrial Enterprises, while general general business expenses are indicated in the Instructions for the Application of the Chart of Accounts. Therefore, we will further consider shop expenses in the “calculation” document.

General running costs

Costs associated with managing an organization, organizing its economic activities, and maintaining its common property are classified as general business expenses.

For example, expenses associated with running an organization (administrative expenses) include:

- administrative and managerial;

- for the maintenance of general business personnel not related to the production process;

- depreciation charges and expenses for repairs of fixed assets for management and general economic purposes;

- rent for general business premises;

- expenses for payment of information, auditing, consulting, etc. services;

- taxes paid by the organization as a whole (property tax, transport tax, land tax, etc.);

- other expenses similar in purpose that arise in the process of managing an organization and are associated with its maintenance as a single financial and property complex.

What is it for?

Within account 25, the following expenditure areas are reflected:

- maintenance and operation of machinery and equipment;

- depreciation and repair of fixed assets;

- insurance;

- utilities related to heating, lighting, maintenance of premises;

- rent for premises, vehicles, equipment and other fixed assets used during the production process;

- remuneration of employees who are employed in production services.

This account is used by industrial, agricultural and other organizations that have a workshop management structure. If we are talking about companies with a functioning scheme without a workshop, production can take into account these same expenses in account 26, which is called “General business expenses”.

Write-off of general production expenses

Since there should be no balance on account 25 at the end of the month, at the end of the month overhead expenses are written off by posting:

Debit account 20 “Main production” - Credit account 25

Similarly, general production costs can be written off as part of the costs of auxiliary production or service industries and farms.

So, when writing off general production expenses, the posting may be as follows:

Debit account 23 “Auxiliary production” - Credit account 25

And if general production expenses are written off for the costs of service facilities, the posting will be as follows:

Debit of account 29 “Service production and facilities” - Credit of account 25

Subscription to electronic publications

Situation: how to reflect in accounting the costs associated with subscriptions to electronic periodicals?

Accounting for expenses for periodical electronic publications depends on the type of contract.

Subscription to electronic periodicals can be issued:

- an agreement for the provision of paid information services for the provision of a copy of a periodical in electronic form (clause 2 of Article 779 of the Civil Code of the Russian Federation);

- a license agreement under which non-exclusive rights to use the electronic resources of the publishing house are transferred (Article 1367 of the Civil Code of the Russian Federation).

In the first case, pay for the subscription to the electronic publication in accounting as an advance payment (clause 3 of PBU 10/99). Reflect the advance payment using the following entries:

Debit 60 subaccount “Settlements for advances issued” Credit 51 – advance payment for subscription to an electronic magazine (newspaper) is transferred.

After receiving the issue of the magazine (newspaper) in electronic form, make the following entries:

Debit 26 (44) Credit 60 subaccount “Settlements with publishing houses” – the cost of the next issue of an electronic magazine (newspaper) is written off as expenses;

Debit 60 subaccount “Settlements with the publishing house” Credit 60 subaccount “Settlements for advances issued” - the amount of the advance is offset against repayment of accounts payable.

This procedure is based on the provisions of the Instructions for the chart of accounts (accounts 60, 44, 26), paragraphs 3, 18 and 19 of PBU 10/99.

In the second case, for accounting purposes, intangible assets received for use are accounted for on an off-balance sheet account in the valuation established by the agreement (clause 39 of PBU 14/2007). The chart of accounts does not provide for a separate off-balance sheet account for accounting for intangible assets received for use. Therefore, the organization needs to independently open an off-balance sheet account and consolidate this in its accounting policies for accounting purposes. For example, account 012 “Electronic subscription publications”.

The one-time payment for the granted right to use the electronic publication should be reflected in accounting in account 97 “Deferred expenses” and included monthly in expenses for ordinary activities during the validity period of the license agreement (paragraph 2, clause 39 of PBU 14/2007).

In accounting, reflect the prepayment by posting:

Debit 60 Credit 51 – the cost of the right to use the electronic publication has been paid.

After gaining access to the electronic publication, make notes:

Debit 012 “ Electronic subscription publications ” – the cost of the right to access an electronic publication is taken into account;

Debit 97 Credit 60 – the cost of the right to access the electronic publication is charged to deferred expenses.

Determine the mechanism for transferring future expenses to cost yourself. The following expenses can be written off:

- evenly;

- in proportion to the income received from sales;

- in other ways.

Determine the period for writing off expenses by the period for which access to the electronic subscription publication was provided. The beginning of this period (the beginning of the period of use of the subscription publication) is determined by the format of the software provided. For example, for the Internet version - from the moment the code is activated.

The period of use of the subscription publication is specified in the contract.

The established procedure for writing off future expenses should be fixed in the accounting policy for accounting purposes (clause 4, 8 of PBU 1/2008, letter of the Ministry of Finance of Russia dated January 12, 2012 No. 07-02-06/5).

Monthly during the period of access to the electronic subscription publication, make the following entries:

Debit 26 (44) Credit 97 – part of the payment for using the electronic publication has been written off.

This procedure is based on the provisions of the Instructions for the chart of accounts (accounts 97, 60, 44, 26), paragraphs 18 and 19 of PBU 10/99.

Attention: many write off deferred expenses at a time. They want to understate large profits of the current period or simply out of ignorance. Officials will be fined for this. In some cases, the organization will also suffer. However, you can avoid trouble.

In accounting, reverse the entry that was written off by the RBP at a time. Remember, this can only be done within the year in which the mistake was made.

r />

For example, the Alpha organization received a certificate of conformity for its products valid for five years. The cost of the certificate was 50,000 rubles. According to the accounting policy at Alfa, RBP is written off evenly.

Error!

Debit 20 Credit 76 – 50,000 rub. – the fee for the certificate is taken into account as part of expenses for ordinary activities.

Correctly like this:

Debit 97 Credit 76 – 50,000 rub. – the fee for the certificate is included in deferred expenses.

Monthly:

Debit 20 Credit 97 – 833 rub. (RUB 50,000: (5 years × 12 months)) – deferred expenses are written off.

Here's how to fix the error in this situation:

Debit 20 Credit 76 – 50,000 rub. – the amount previously erroneously included as expenses for ordinary activities is reversed;

Debit 97 Credit 76 – 50,000 rub. – the fee for the certificate is included in deferred expenses.

At the same time, expense the amounts written off for the past months. For example, if three months have passed since costs were accepted for accounting:

Debit 20 Credit 97 – 2500 rub. (3 months × (50,000 rubles: (5 years × 12 months))) – deferred expenses are written off.

How are overhead costs distributed?

The organization determines the methods for distributing general production and general business expenses independently based on the characteristics of its activities and the procedure established in the Accounting Policy.

In general, to determine the distribution coefficient of overhead costs, the formula can be presented as follows:

KOPR = OPR / B,

where KOPR is the coefficient of distribution of overhead costs;

OPR - the amount of general production expenses for the month;

B – base for distribution of general production expenses.

The specified coefficient can show how many rubles of overhead costs are per 1 ruble of the distribution base. This coefficient can also be presented as a % by multiplying the resulting indicator by 100.

We gave an example of the distribution of indirect costs reflected in account 25, in proportion to the direct wages of the main production workers.

However, the basis for the distribution of general production costs may be different. For example, the cost of basic raw materials and supplies, the number of employees, the cost of fixed assets and other indicators.

When determining a particular method for distributing overhead costs, the basis is chosen that most closely shows the relationship between overhead costs and the cost of the final product.

You can find more complete information on the topic in ConsultantPlus.

Free access to the system for 2 days.

Typical transactions for account 20

By debit of the account

| Contents of a business transaction | Debit | Credit |

| Depreciation was calculated on fixed assets used in the main production | 20 | 02 |

| Depreciation was calculated on intangible assets used in the main production | 20 | 05 |

| Materials are written off as costs for production of products (performance of work, provision of services) | 20 | 10 |

| The cost of slaughtered animals is written off as main production costs | 20 | 11 |

| The amount of deviations in the cost of inventories transferred to the main production was written off | 20 | 16 |

| VAT on works (services), not reimbursed from the budget, is included in the costs of main production | 20 | 19 |

| Costs of main production were transferred from subaccount to subaccount | 20 | 20 |

| Semi-finished products from the main production were transferred for processing | 20 | 21 |

| Included in the costs of main production are the costs of auxiliary production | 20 | 23 |

| The share of general production costs is included in the costs of main production | 20 | 25 |

| The share of general business expenses is included in the costs of main production | 20 | 26 |

| Losses from defects are included in the costs of main production | 20 | 28 |

| Finished products are transferred for the needs of the main production (using account 40) | 20 | 40 |

| Purchased goods and components were transferred for the needs of the main production | 20 | 41 |

| Finished products were transferred for the needs of the main production; finished products were returned from the warehouse for processing to the main production | 20 | 43 |

| The cost of work (services) performed (rendered) by contractors is taken into account in the costs of main production | 20 | 60 |

| The amounts of accrued taxes and fees are taken into account in the costs of main production | 20 | 68 |

| Insurance contributions to extra-budgetary funds are calculated from the wages of workers engaged in primary production | 20 | 69 |

| Wages accrued to employees engaged in primary production | 20 | 70 |

| Expenses for the needs of the main production were paid by accountable persons | 20 | 71 |

| Work in progress included in the contribution to the authorized capital | 20 | 75-1 |

| Insurance payments are taken into account in the costs of main production | 20 | 76-1 |

| Claims made to contractors for defects and downtime caused by them, which are not subject to recovery, are taken into account in the costs of main production | 20 | 76-2 |

| A work-in-progress item was received from the head office (posting in branch accounting) | 20 | 79-1 |

| An item of work in progress was received from a branch allocated to a separate balance sheet (posting in the accounting of the head office) | 20 | 79-1 |

| Services related to the main production, branch and head office were provided (posting in branch accounting) | 20 | 79-2 |

| Services related to the main production, the head office and the branch were provided (posting in the accounting of the head office) | 20 | 79-2 |

| An item of work in progress was received as a contribution under a joint activity agreement (on a separate balance sheet of the joint activity) | 20 | 80 |

| A work-in-progress facility was received as targeted financing | 20 | 86 |

| The amount of main production costs that was erroneously written off has been adjusted | 20 | 91-1 |

| Excess work in progress discovered during inventory was capitalized | 20 | 91-1 |

| Shortages and losses from damage to valuables within the limits of natural loss norms are taken into account as part of the costs of main production | 20 | 94 |

| The accrued amount of the reserve for future expenses is included in the costs of main production | 20 | 96 |

| Future expenses related to the current period are taken into account in the costs of main production | 20 | 97 |

By account credit

| Contents of a business transaction | Debit | Credit |

| Materials returned to main production were capitalized | 10 | 20 |

| Own-produced materials have been capitalized | 10 | 20 |

| The offspring of animals have been registered. The cost of animals has been increased by the amount of expenses for raising and fattening them. | 11 | 20 |

| Inventories manufactured in the main production are capitalized (if account 15 is used) | 15 | 20 |

| Semi-finished products of our own production were capitalized | 21 | 20 |

| The costs of the main production for correcting defects were written off | 28 | 20 |

| The actual cost of manufactured finished products of the main production was written off | 40 | 20 |

| Finished products released by the main production were capitalized | 43 | 20 |

| The cost of work (services), the proceeds from the sale of which cannot be recognized immediately, has been written off. | 45 | 20 |

| Part of the main production costs was written off from insurance compensation | 76-1 | 20 |

| The costs of main production were reduced by the amount of the recognized claim presented to contractors | 76-2 | 20 |

| An object of work in progress was transferred by the head office to a branch allocated to a separate balance sheet (posting in the accounting of the head office) | 79-1 | 20 |

| The object of work in progress was transferred by the branch, allocated to a separate balance sheet, to the head office (posting in the accounting of the branch) | 79-1 | 20 |

| The cost of services provided to a branch allocated to a separate balance sheet was written off (posting in the accounting of the head office) | 79-2 | 20 |

| The cost of services provided by the head office was written off (posted in the branch accounting) | 79-2 | 20 |

| An object of unfinished production was transferred to a participant in a simple partnership upon termination of the agreement on joint activity (on a separate balance sheet of the joint activity) | 80 | 20 |

| The cost of work (services) sold has been written off. | 90-2 | 20 |

| Included in other expenses are costs associated with obtaining additional income | 91-2 | 20 |

| Included in other expenses are costs associated with the disposal of other assets of the organization (fixed assets, materials, etc.) | 91-2 | 20 |

| Loss of work in progress due to extraordinary circumstances is written off as other expenses | 91-2 | 20 |

| Deficiencies identified in the main production are reflected | 94 | 20 |

What do industry guidelines say?

Let us turn to the Guidelines for calculating the cost of production at non-ferrous metallurgy enterprises[2]. In accordance with them, general mine and general shop expenses of mining departments, individual processing plants and metallurgical plants that are part of mining and processing and mining and metallurgical plants (associations) as workshops (without settlement accounts) are considered and accounted for as shop

expenses

.

They directly relate to individual types of products manufactured in workshops, or are distributed between individual types of products and work in proportion:

- processing costs (for auxiliary materials, fuel and energy for technological purposes, for wages of production workers, for the maintenance and operation of equipment, as well as contributions for social needs);

- expenses for remuneration of production workers, maintenance and operation of equipment;

- labor costs for production workers;

- the amount of waste (industrial gases and wastewater) sent for neutralization (this method is only suitable for the costs of a workshop intended for waste neutralization).

According to the method chosen in the accounting policy of the organization, shop expenses are distributed between mines and processing plants that are part of the mining departments of non-ferrous metallurgy enterprises.

Example 1

At a non-ferrous metallurgy enterprise, the following shop (general production) expenses were incurred: for the maintenance of general shop buildings (150,000 rubles), for labor protection measures (150,000 rubles), for the salaries of shop managers (300,000 rubles), for bonuses for innovation (RUB 200,000). The listed expenses are distributed among three mines, in which during the reporting period the salary amounted to 200,000, 300,000, 100,000 rubles, and direct costs for the maintenance and operation of equipment - 50,000, 100,000 and 50,0000 rubles. According to the accounting policy, shop expenses are distributed in proportion to the costs of labor and maintenance and operation of equipment.

The total amount of shop expenses for the reporting period will be 800,000 rubles. (150,000 + 200,000 + 300,000 + 150,000). The distribution indicators will be equal (calculations in rubles):

1) first mine – 31.25% ((200,000 + 50,000) / (200,000 + 300,000 + 100,000 + 50,000 + 100,000 + 50,000));

2) second mine – 50% ((300,000 + 100,000) / (200,000 + 300,000 + 100,000 + 50,000 + 100,000 + 50,000));

3) third mine – 18.75% ((100,000 + 50,000) / (200,000 + 300,000 + 100,000 + 50,000 + 100,000 + 50,000));

Accordingly, shop costs will be distributed among mines as follows:

1) 250,000 rub. (800,000 x 31.25%) – for the first mine;

2) 400,000 rub. (800,000 x 50.00%) – for the second mine;

3) 150,000 rub. (800,000 x 18.75%) – for the third mine.

The following entries will be made in the company's accounting:

| Contents of operation | Debit | Credit | Amount, rub. |

| Reflects the costs of maintaining general purpose buildings, including depreciation | 25 | 02, 10, 60 | 150 000 |

| The salaries of shop managers and contributions are reflected | 25 | 70, 69 | 300 000 |

| Prizes awarded for innovation | 25 | 70, 69 | 200 000 |

| Expenses for labor protection measures are shown | 25 | 70, 69, 60 | 150 000 |

| The salary of the workers of the first mine and the costs of maintaining and operating the equipment are shown. | 20-1 | 70, 69, 60, 02 | 250 000 |

| The salary of workers of the second mine and the costs of maintaining and operating equipment are shown. | 20-2 | 70, 69, 60, 02 | 400 000 |

| The salaries of workers at the third mine and the costs of maintaining and operating equipment are shown. | 20-3 | 70, 69, 60, 02 | 150 000 |

| Distributed costs for the first mine are reflected | 20-1 | 25 | 250 000 |

| Distributed costs for the first mine are reflected | 20-1 | 25 | 400 000 |

| Distributed costs for the third mine are reflected | 20-1 | 25 | 150 000 |

Let us pay attention to some more instructions from the above-mentioned industry “calculation” document. The shop expenses of such mines and processing plants will consist of two parts - their own shop costs and a share of the general shop costs of the mining departments. General shop expenses of the above-mentioned individual processing plants and metallurgical plants that are part of mining and processing and mining and metallurgical plants (associations) are reflected in the same order. What does it mean?

Let's return to the example: in account 25, the general shop expenses of the mine administrations were actually taken into account, while account 20 showed the shop's own expenses, in particular, the salaries of the main workers with contributions to funds and equipment costs. That is, the mines are considered the main production departments, and not auxiliary units, in which direct and indirect costs are further divided. It turns out that the wording of the old instructions should not always be taken literally; it is necessary to adapt it to the specific situation in modern realities.

On a note

Shop expenses, in addition to the main products, are also distributed for work and services performed for their own capital construction (including capital mining and geological exploration work financed from the republican budget), housing and communal services, for non-industrial enterprises and externally. For comparison, let us turn to more modern Methodological provisions for calculating the cost of production at enterprises of the chemical complex. The document uses the same names of costs as in the current Instructions for using the Chart of Accounts. Let us recall: in the context of the article, we are interested in general production costs caused by the management of production divisions, with their reflection in analytical accounting for each division.

General production costs of each division are included only in the cost of those products that are manufactured by this division, including the cost of work (services) performed for other divisions or non-industrial farms. The cost of chemical goods includes general production costs:

1) completely - in workshops (divisions) specialized in the production of these goods;

2) partially - in the manufacture of such goods in non-specialized workshops along with the main products of the enterprise. Moreover, the cost of chemical consumer goods includes the corresponding share of only those general production costs that are associated with the production of these goods. For this purpose, a special calculation of overhead costs of non-specialized departments (shops) is compiled.

Indirect costs when calculating product costs can be distributed in various ways, chosen by the enterprise, taking into account the characteristics of production and the cost structure. The following methods are recommended as the main ones for chemical and petrochemical enterprises:

1) in proportion to the basic salary of production workers or all industrial production personnel of the workshop;

2) in proportion to conditional coefficients calculated and accepted by the enterprise itself on the basis of estimates of relevant overhead costs;

3) in proportion to the “sales prices” adopted by the enterprise to distribute the costs of complex production (shops);

4) natural (weight) method, that is, in proportion to the weight of the products produced or another natural measurement (in m, sq. m, etc.);

5) in proportion to direct costs – in industries with a high level of material costs;

6) in proportion to direct labor costs - in labor-intensive industries (with the share of labor costs and other costs associated with its use in total direct costs exceeding 50%).

You can use other methods of allocating costs that best reflect their relationship with the product.

Example 2

The plant's workshop is engaged in the production of main and by-product chemical products. Indirect costs between these types of products are distributed using the natural (weight) method - in proportion to the weight of the products produced. For the selected period, this mass ratio of manufactured products based on production reports was 80% to 20% (main products to by-products). Direct costs associated with the production of these types of products amounted to 500,000 and 100,000 rubles, indirect (general production) costs – 200,000 rubles.

According to the ratio of natural indicators, indirect costs related to the production of basic chemical products will amount to 160,000 rubles. (RUB 200,000 x 80%), while by-products will account for RUB 40,000. (RUB 200,000 x 80%) of such expenses. To account for direct costs for main products, we use subaccount 20-1, and secondary costs - 20-2.

The following entries will be made in the company's accounting:

| Contents of operation | Debit | Credit | Amount, rub. |

| Direct costs for main products are reflected | 20-1 | 10, 70, 69 | 500 000 |

| Reflects direct costs of by-products* | 20-2 | 20-1 | 100 000 |

| General production costs reflected | 25 | 02, 10, 60 | 200 000 |

| Indirect costs are distributed among the cost of main chemical products | 20-1 | 25 | 160 000 |

| Indirect costs are distributed among the cost of chemical by-products | 20-2 | 25 | 200 000 |

* The article “By-products” includes costs related to the production of by-products in the production of the main one. These costs are excluded from the costs of production of main products, since by-products are independent in nature and are calculated separately, which explains the entry Debit 20-2 Credit 20-1

. Moreover, the amount of such costs is determined based on the mass ratio of manufactured products (500,000 rubles x 20%), that is, the costs of by-products are relatively direct.

Subaccounts

The chart of accounts establishes that it is recommended to open two sub-accounts for this account:

- 25 subaccount 1 – “Maintenance and operation of equipment”, which summarizes the costs of operating the organization’s equipment;

- 25 subaccount 2 – “General shop expenses”, which is supposed to summarize the costs of managing and servicing the main production facilities.

However, since account 25 can accumulate expenses of various natures, to analyze them it will be more convenient to open a separate sub-account for each type:

- Salaries of general production workers;

- Contributions to social funds;

- Raw materials and materials;

- fuels and lubricants;

- Depreciation of fixed assets;

- Depreciation of intangible assets;

- Public utilities;

- Etc.

Attention! With this type of accounting, a “Closing” subaccount must be opened. Its essence is that during the closing procedure, first the costs of all subaccounts are written off to it, and then distribution from it to the accounts of other productions begins.

Subaccounts of account 25

The main subaccounts of this account are: 25-1 “Maintenance and operation of equipment”, 25-2 “General shop expenses”.

The first subaccount is used to ensure ongoing accounting and control activities to implement cost estimates associated with the maintenance and operation of equipment in the main workshops.

Within construction organizations, this subaccount records the costs of using construction machinery and mechanisms.

Within the framework of subaccount 25-2, expenses for servicing production and managing workshops, as well as similar structural divisions of main and auxiliary production, are accounted for.

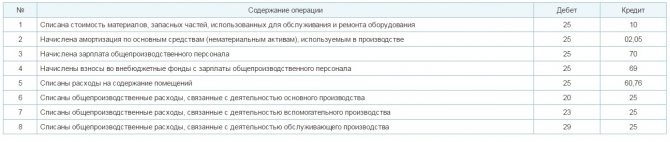

Examples of typical postings

Let's look at what typical operations are made with a score of 25.

| Debit | Credit | Operation description |

| 25 | 60, 76 | Receipt of services from the supplier is reflected |

| 25 | 10 | Materials and fuels were written off |

| 25 | 02 | Accrued depreciation of fixed assets for general production purposes |

| 25 | 05 | Depreciation of intangible assets accrued |

| 25 | 70 | Salaries accrued to general production employees |

| 25 | 69 | Social contributions are accrued for employee salaries |

| 25 | 97 | Future expenses were written off |

| 20 | 25 | At the end of the period, accumulated expenses are written off to main production |

| 23 | 25 | The expenses for auxiliary production were written off |

| 29 | 25 | Expenses for service facilities were written off |

Help us promote the project, it's simple: Rate our article and repost!

(

1

ratings, average:

5,00

out of 5)

List of accounts involved in accounting entries:

|

|

More detail.

On account 25 many of the costs of a production enterprise can be collected. Appendix 4 to the Basic Provisions for Calculating Product Costs at Industrial Enterprises provides a fairly detailed list of shop costs. Moreover, both production and non-production costs are highlighted.

| Shop costs (overhead costs) | |||

| ⇓ | ⇓ | ||

| Production costs | Non-production expenses | ||

| ⇓ | ⇓ | ||

| Maintenance of the workshop management apparatus and other workshop personnel; depreciation, maintenance, current repairs of buildings, structures, equipment; innovation, inventions; tests; occupational Safety and Health; wear and tear of low-value equipment | Losses from downtime, damage to material assets in workshops, underutilization of parts, components and technological equipment; shortage of material assets and work in progress (less surplus); etc. | ||

The following recommendations apply to both types of shop costs. Their total value is included in the cost of gross and marketable output of the enterprise through the cost of work and services performed by auxiliary shops for the main production. That is, some indirect expenses are included in others ( Debit 23 Credit 25

), located closer to direct costs (

Debit 20 Credit 23

) for production. In fact, this is not entirely true, because depending on the specifics of production, costs can be attributed from account 25 directly to account 20 without using account 23.

This is partly confirmed by the Basic provisions for calculating the cost of production at industrial enterprises. Shop costs, as a rule, are distributed among various types of products in proportion to the sum of the basic salary of production workers (without additional payments under progressive bonus systems) and the costs of maintaining and operating equipment. In certain industries, shop costs can be distributed in proportion to the amount of basic costs without the cost of raw materials, materials and semi-finished products. The conditions for using one of the above methods at enterprises in the relevant industries are established in industry instructions.