Advice from practitioners that will help rid bonuses from the suspicions of tax authorities.

In accordance with Art. 129 of the Labor Code of the Russian Federation, wages are remuneration for work depending on the employee’s qualifications, complexity, quantity, quality and conditions of the work performed. But in addition to salary, many employers want to further stimulate their employees by paying them bonuses.

Often, the manager does not think about the structure and nature of these payments, which can lead to adverse consequences.

The most important thing in determining this payment is that it is calculated in addition to the employee’s salary.

In accordance with paragraph 2 of Art. 255 of the Tax Code of the Russian Federation, bonuses for production results that are paid to employees, the organization has the right to classify as labor costs for profit tax purposes. However, the tax consequences of certain aspects of the bonuses can be very burdensome for the company.

How to develop and what documents to support?

We note that rewarding employees with bonuses is enshrined in the norms of the Labor Code of the Russian Federation (paragraph 4, paragraph 1, article 22 of the Labor Code of the Russian Federation, paragraph 1, article 191 of the Labor Code of the Russian Federation).

But to justify the costs of bonuses for its employees, the employer is obliged to fulfill a number of conditions: 1. Provide this remuneration. To do this, it is necessary to supplement the regulations on remuneration and labor (collective) agreements with information on bonuses for employees, but it is advisable to issue a new local regulatory act of the organization, namely a regulation on bonuses.

2. It is necessary to identify and consolidate specific and differentiated bonus indicators in personnel documents. This is necessary to comply with the requirements of paragraph 1 of Art. 252 of the Tax Code of the Russian Federation. An important criterion when developing bonus regulations is the use of realistically measurable indicators. It is important to avoid vague language.

Thus, in order to take into account the bonuses in question for tax purposes, the employment (collective) agreement, bonus provision or other local regulatory act must contain the following criteria:

- grounds for payment of bonuses, specific measurable performance indicators for bonuses;

- sources of bonus payment;

- amounts of bonuses and the procedure for their calculation.

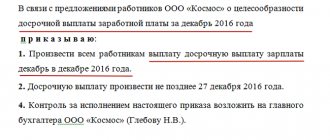

3. It is necessary to have documents confirming the basis for payment of bonuses (clause 1 of Article 252 of the Tax Code of the Russian Federation). Such documents can be a petition, a memo from the immediate supervisor, supported by actual performance indicators of the employee, etc. Also, in order to document the costs of bonuses to employees, the employer must make these payments on the basis of an order (instruction) on rewarding employees (form T-11, T-11a or according to a form developed by the employer).

An important circumstance is that the bonus should not be paid at the expense of the organization’s net profit, special-purpose funds or targeted income. Payments from these sources are not taken into account for tax purposes (clause 1, 22, article 270 of the Tax Code of the Russian Federation).

Point-based job evaluation system

The basis on which regulations on bonuses are developed in budgetary institutions is often a point bonus system, according to which the size of an individual employee’s bonus depends on the number of points he scored in the period under review. Points are assigned depending on the achievement of certain planned indicators. The criteria by which points are assigned and the conditions for assignment are established in advance.

The point bonus system is implemented in the following step-by-step order:

- The organization creates a special bonus fund from which bonuses will be paid.

- During work in a certain period - month, quarter, year - employees are assigned one or another number of points - each depending on individual achievements according to established criteria.

- At the end of the period, the total number of points received by all employees of the organization is calculated.

- The bonus fund is divided by the total number of points - the cost of one point is established.

- Each employee receives a bonus in an amount equal to the product of the cost of one point by the number of points received specifically by him based on the results of his work.

How much and what to pay for?

The size of the premium can be fixed, as well as differentiated (as a percentage of a certain amount).

A fixed percentage of the bonus can be set for the absence of defects and complaints, for the completion of work and services according to established deadlines, etc. For example, 20% of piecework earnings, 30% of the official salary. If the number of bonus indicators complicates the calculation of the final bonus amount, you can set a bonus limit with a gradation from minimum to maximum (the amount of the monthly bonus is from 20 to 50% of the employee’s salary).

You can also draw up a crisis sheet, which will indicate all bonus criteria. During the month, the head of the structural unit will evaluate the employee’s performance on a 10-point scale, and at the end of the month issue final grades. However, in such cases, accusations of subjectivity on the part of the employees being evaluated cannot be avoided, which can lead to an unfavorable environment within the team.

Bonus criteria deserve special attention for the reason that precisely due to their absence, ambiguity, and opacity, tax authorities may come to the conclusion that bonus payments are unjustified, which can lead to additional income tax charges.

In each company, bonus criteria differ depending on their functional purpose and the structural unit in which the employee is employed.

For employees who are directly involved in the production of products, the following bonus indicators are established: fulfillment of the production plan in a given volume, minimization of defects.

For the commercial department, important performance criteria are clearly: meeting KPI indicators, effective work with current clients, the absence of complaints and claims regarding the quality of products sold and services provided from buyers and customers. But here it is important to take into account that the monthly fulfillment of these indicators does not provide for bonus payments, since they are specified as functional responsibilities in employment contracts with employees of the commercial department. The basis for bonuses can only be exceeding KPI indicators, expanding the client base, etc.

It is important to take into account here that the use of the same bonus criteria for all structural divisions of the company is not applicable, and they must be established based on the job responsibilities of an individual employee.

Often, an employer has a question regarding the justification of bonuses for employees of the accounting department, human resources department, information technology department and other departments that are not related to the production and sale of products.

Indeed, the job responsibilities of these employees do not directly correlate with the main goal of the organization - profit maximization.

However, this does not serve as a basis for refusing bonuses to these categories of employees.

In this case, when developing bonus criteria, it is necessary to take into account job responsibilities and the effectiveness of their implementation.

For example, the basis for paying a bonus to an accounting employee may be:

- improving accounting methods through the effective implementation and use of new software;

- timely and high-quality preparation of reports on personalized data to pension and other funds, the Federal Tax Service and other regulatory authorities;

- absence of comments on the results of various inspections;

- high results when performing complex unscheduled work

- high speed while performing various functions simultaneously

- maintaining financial discipline, etc.

As for the information technology department, the employer can justify expenses here by specifying in the bonus regulations such criteria as: introduction of new technologies in order to increase the company’s information security, uninterrupted operation of infrastructure equipment, high speed of troubleshooting of computers and office equipment, development of new software equipment to improve the efficiency of various structural divisions, etc.

It is not recommended to use wording such as “for a conscientious attitude to work” or “for compliance with labor standards and labor discipline.”

Due to their “vagueness”, the company may face claims from regulatory authorities.

Payments to civil servants

In accordance with Art. 50 of Federal Law No. 79-FZ of July 27, 2004, in addition to the monthly salary paid, a civil servant receives additional payments:

- bonus for length of service, which, depending on the length of service, reaches 30% of the salary;

- allowance for work under special conditions;

- bonus for working with state secrets;

- bonus for completing particularly important or particularly difficult tasks;

- monthly cash incentive;

- annual one-time financial assistance, which is paid for the next vacation.

Is everything so simple with bonuses to management?

Bonuses to the company's management deserve special attention.

For top management, bonus indicators are primarily related to making a profit. Here you can take as a basis: exceeding the monthly sales plan as a percentage, effectively conducting marketing activities, reducing the number of complaints from customers, ensuring the uninterrupted operation of computer equipment and office infrastructure, increasing the volume of supplies and monitoring their uninterruption, as well as the number of new contracts with suppliers and customers. Let us remind you that when assigning a bonus to employees, a corresponding order from the head of the organization is required. But this rule does not apply when it comes to remuneration for the general director and this is due, first of all, to his special legal status.

In a company where the general director is not its sole founder, payment of a bonus cannot be made only on the basis of his order (Part 2 of Article 135, Article 191 of the Labor Code of the Russian Federation). This is due to the fact that this issue is regulated simultaneously by labor law and the norms of corporate legislation (part 2 of article 145 of the Labor Code of the Russian Federation, paragraph 4 of article 40 of Federal Law No. 14-FZ “On Limited Liability Companies”). Therefore, the amount of remuneration for the general director, including bonuses, is determined by agreement between him and the founders, the board of directors (supervisory board) of the company, and the decision to pay the bonus is made on the basis of the minutes of the general meeting of participants (shareholders) of the company, or on the basis of a decision of the board of directors or supervisory board advice.

In the case of an employment relationship between the general director, who is also the sole founder, and the organization, expenses associated with the payment of wages are taken into account according to the general rule (clause 1 of article 255 of the Tax Code of the Russian Federation, clause 6 of clause 1 of article 346.16 of the Tax Code of the Russian Federation).

But it is important to remember that the bonus was provided for in the employment contract, otherwise such payments do not reduce the taxable base for income tax (letter of the Ministry of Finance of the Russian Federation dated October 13, 2015 No. 03-03-06/1/58416, clause 21 of Article 270 of the Tax Code RF). The criteria for bonuses can be agreed upon jointly with the personnel service based on the activities of the enterprise, and the decision on payment in any case is made on the basis of the minutes of the general meeting of participants (shareholders) of the company, or on the basis of a decision of the board of directors or supervisory board.

If the director’s legal relationship with the organization is not formalized by an employment contract, then all payments in his favor cannot be accepted for tax purposes (Clause 21, Article 270 of the Tax Code of the Russian Federation).

It follows from this that the general director of the organization, who is also its sole founder, does not have the right to single-handedly calculate and pay wages, as well as make bonus payments. Consequently, the organization does not have the right to take such expenses into account for tax purposes (letter of the Ministry of Finance of the Russian Federation dated February 19, 2015 No. 03-11-06/2/7790).

What about bonuses for significant dates?

Some companies pay bonuses for significant dates (March 8 - International Women's Day, May 9 - Victory Day, 12 - Russia Day) or professional holidays (March 29 - Lawyer's Day, May 24 - Personnel Day, September 16 - Workers' Day forests).

The inclusion of these payments in expenses will definitely cause claims from regulatory authorities. It is important to take into account that, according to the Russian Ministry of Finance, these payments are not related to production results and are not incentives. Therefore, the employer does not have the right to take them into account when calculating income tax (letters of the Ministry of Finance of Russia dated July 22, 2016 No. 03-03-06/1/42954, dated July 9, 2014 No. 03-03-06/1/33167, etc. .).