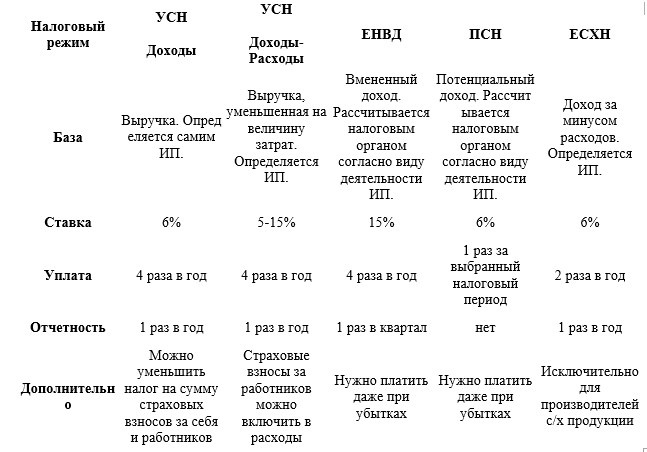

A single tax on imputed income

The use of UTII in 2021 as the basis for calculating payments does not imply the actual profit of the entrepreneur, but the income already preliminarily imputed by the state.

It is calculated according to special indicators. This is one of the special taxation systems (n/a).

Regarding UTII in 2021, changes and news for retail trade have occurred in a favorable direction: its terms have been extended, and the rules for deducting certain amounts have also been improved.

The table approved by regulations shows the coefficients for UTII for 2021 for each type of business.

It and the table of basic UTII profitability for 2021 are used for calculations and determining the parameters of the enterprise.

The amount of UTII in 2021 is directly dependent on them, as well as on the number of personnel, the volume of trading platforms and the region where the organization is located.

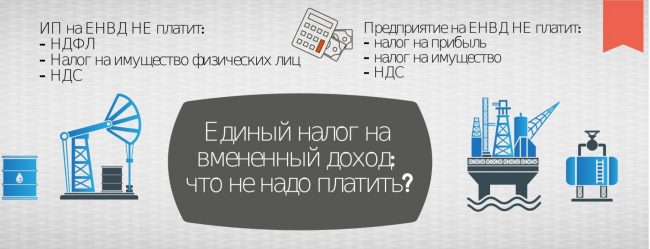

When using UTII in 2021, as before, an enterprise or businessman is exempt from other taxes.

The use of UTII in 2021 is voluntary, and the management of the organization decides for itself whether to switch to UTII in 2018 or choose other modes (STS, OSNO).

In 2021, a Decree was issued extending the use of UTII in 2021 for 3 years. This regime is legally regulated by Art. 26.3 NK.

back to menu ↑

Advantages

The use of UTII in 2021 has the following advantages:

| Parameter | Meaning |

| Profit Impact | The amount actually received does not matter - the amount of UTII in 2018 remains fixed. |

| Reports | Simplified as much as possible. The UTII declaration is submitted in 2018. |

| Amount of UTII in 2021 | Extremely low. Payments need to be compared with the simplified tax system when choosing a system, but, for example, UTII in 2021 for retail trade with large premises, the regime is not profitable. |

| Transition restrictions | There are no profitability limits for registration, but for example in the simplified tax system and PSNO they exist. There is no need to wait until the end of the year to switch to “imputation”; it is always available within a 5-day period, so UTII in 2018 for retail trade is in first place in terms of profitability. |

| Combination of systems | The use of UTII in 2021 is allowed to be combined with any type of non-taxable income. |

| Accounting | They are conducted at will according to simplified rules. |

| Other payments | The transition to UTII in 2021 eliminates other taxes, but the payment of insurance premiums is mandatory. UTII is reduced by their amount. The UTII declaration in 2021 must display the deduction. |

| Reduced payments | They use an adjustment: the table has UTII coefficients for 2021 for each activity, which allows you to take into account and change various factors in order to reduce payments. The amount of UTII in 2018 is adjusted using the K2 indicator if the activity was carried out in an incomplete tax period. |

| Possible benefit options | UTII in 2021 allows you to keep the money saved in circulation. In addition, this system allows for the combination of various types of information. In this case, you should carefully check whether such a combination will be beneficial. |

| Zero rate | UTII in 2021 changes and news for retail trade and for some types of commerce, for those who first received the status of individual entrepreneurs until 2020, include zero interest. However, they are introduced by local authorities quite rarely. |

| Cash registers | According to UTII in 2021, the changes did not affect deductions of funds spent on online cash registers. This is only possible for individual entrepreneurs worth 18 thousand rubles. The exemption from their mandatory establishment is valid until July 2019. |

back to menu ↑

Flaws

The disadvantages are:

- the amount of UTII in 2021 is independent of profit, and this may turn out to be a minus. If UTII for an LLC is established in 2021 and the organization is unprofitable, then it is obliged to pay it, the same applies to the period when there was no activity;

- This norm is not approved in all parts of the Russian Federation - it depends on the decision of local authorities. For example, in 2021 there are no changes to this item in UTII in Moscow and it cannot be used there;

- deduction of insurance payments is available only for the time when this information was used. Exception: when funds were deposited before the filing of the declaration for this time. That is, if an individual entrepreneur paid for the 1st quarter on April 15, and submitted the declaration on the 25th, then he has the right to deduct them. If the reports are submitted first, and then contributions are made, the inspectorate will recalculate the UTII.

- The transition to UTII in 2021 is feasible when the parameters of personnel and trading platforms are within certain limits. With “imputation” they are wider than that of PSN, so UTII in 2021 for retail trade and public catering will be more economical, but if there are a large number of employees, this regime will be inconvenient and then it makes sense to use OSNO;

- The deadline for submitting reports in 2021 is quarterly, this is a minus compared to the simplified version, in which it must be submitted once every 12 months.

back to menu ↑

Latest innovations

According to UTII in 2021, the changes are minor. As before, it has been extended until 2021 and there have been some improvements:

- You can deduct insurance premiums paid for yourself and for employees. For UTII in 2021, changes and news for retail trade on this item allow for significant savings;

- the UTII declaration in 2021 was changed in connection with the above, but the deadlines for submitting reports in 2021 UTII remained unchanged;

- the K1 indicator was increased;

- In 2021, UTII for retail trade has not changed on an issue important for individual entrepreneurs, whether it is possible to pay by bank transfer with legal entities: everything remains the same, you can do this with all counterparties;

- the deferment for online cash registers has been extended until the middle of the next 12 months.

back to menu ↑

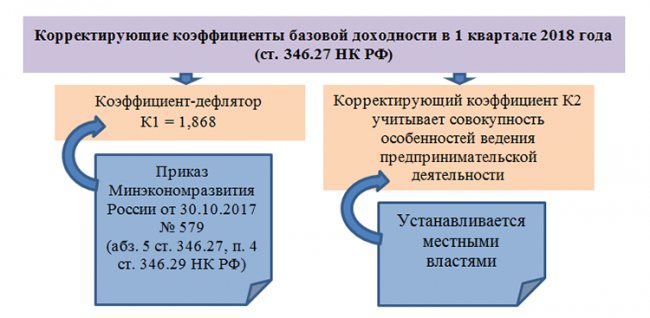

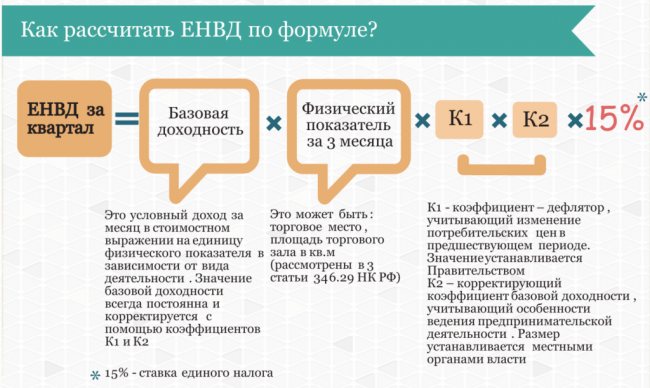

What are K1 and K2?

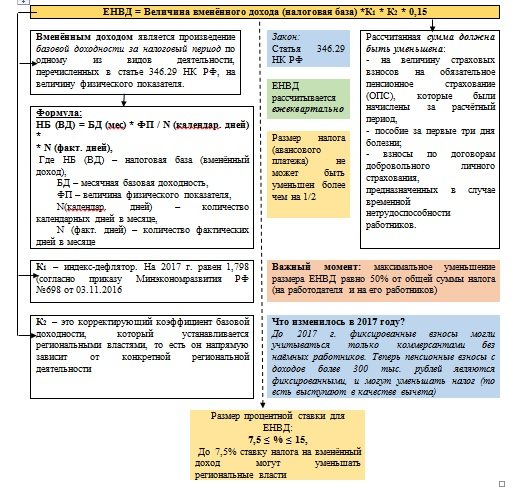

The coefficients K1 and K2 of UTII in 2021 are set at the State level. K1 is a deflator that is used to calculate UTII, is established at the federal level and is not subject to changes throughout the year. And the deflator coefficient K2 depends on the basic yield indicator and the local administration. Its goal is to reduce the tax rate. This coefficient cannot be higher than 1.0.

What does basic yield mean? This is the potential amount of income received by an entrepreneur in a certain business sector during one month of business. The Tax Code in Article 346.29 provides the amounts of basic profitability for calculating K2 for UTII for 2021, the table contains data based on one physical indicator.

So, to carry out independent calculations of UTII, an entrepreneur needs three indicators:

- Basic profitability (Article 346.29 of the Tax Code of the Russian Federation).

- Deflator coefficient K1.

- Deflator coefficient K2.

The first indicator has already been mentioned above, but we will tell you how to determine the last two indicators further in our article.

Sample of filling out UTII-2 for individual entrepreneurs 2017

What is needed to apply for UTII

According to UTII in 2021, there are no changes in requirements for enterprises. The ability to use this mode is available if the subject follows the following rules:

- UTII in 2021 for retail trade and other commerce is acceptable if the company’s staff is up to 100 people;

- the type of entrepreneurship must be provided for in legislation;

- the transition to UTII in 2021 limits the participation of third-party organizations in business to 25%;

- there should be no use of trust agreements and simple partnership agreements;

- the occupation should not be related to the rental of gas stations (including gas stations), as well as their locations;

- UTII for an LLC in 2021 is possible if there is no patent and unified agricultural tax;

- the organization is not a major payer.

back to menu ↑

Deflator coefficient for personal income tax

For personal income tax, the deflator coefficient is used to adjust payments of foreign citizens from “visa-free countries” working on the basis of a patent for hire from individuals (in particular, for personal, household and other similar needs not related to business activities). These foreign workers are required to independently make monthly fixed advance payments for personal income tax for the period of validity of the patent in the amount of 1,200 rubles (Clause 2 of Article 227.1 of the Tax Code of the Russian Federation). The size of the deflator coefficient for 2021 for these purposes was 1.623. And for 2021 it has increased and is 1.686

For whom is it available?

Activities on UTII in 2021 are possible if its parameters comply with the law:

| Entrepreneurship | Parameters that make it impossible to use |

| Household sphere | Activities on UTII in 2021 should not include the provision of land for use for commercial outlets and (or) gas station sites. |

| Veterinary | Large payers. |

| Transport repair and maintenance | Penalty parking lots. |

| Rental of parking spaces, including security services. | If trade fees apply |

| Cargo and passenger transportation, subject to the availability of up to 20 units of transport for such commerce. | In addition to that in agricultural production. |

| UTII in 2021 for retail trade can be applied if it has: 1 point up to 150 sq. m.; 2 points in stationary objects without halls (in covered markets, through tents, kiosks, vending machines) or through non-stationary objects (counters, vans, tanks). | In medical or social institutions. |

| Catering up to 150 sq. m., including those without halls. | The number of personnel last year was more than 100 people. |

| Placement of advertising outside objects on special structures, as well as on/in transport. | Activities on UTII in 2021 should not be carried out if there is a 25% contribution from another enterprise. This also applies to all types of UTII commerce. |

| Renting sites up to 500 sq. m. for rent, as well as points for retail trade, catering, including land plots. | Use of trust deeds or simple partnerships. |

| Hotel business with sleeping places up to 500 sq. m. |

Important: Local authorities are authorized to determine the compliance of UTII with commercial activities provided for in the law. If the type of entrepreneurship is in a regulatory act, but has not been introduced in a certain region of the country, then the subject does not have the right to use “imputation”.

back to menu ↑

How to transfer and deadlines

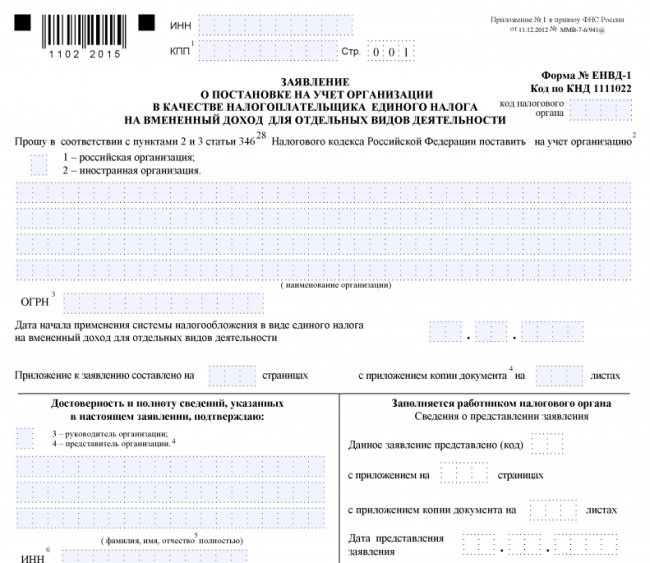

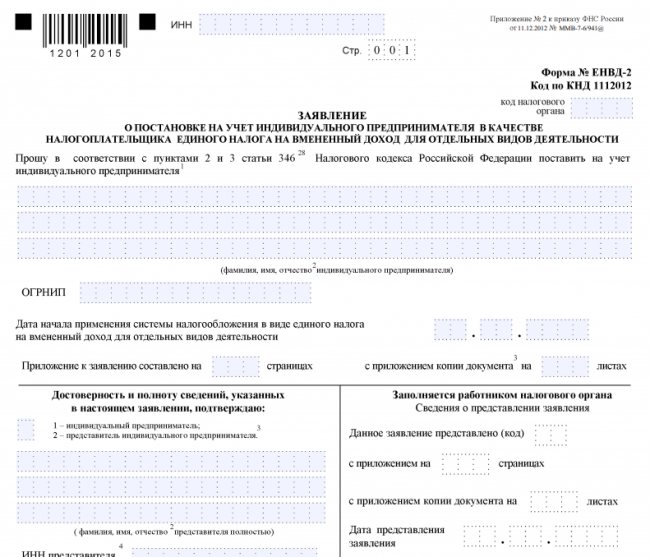

The transition to UTII in 2021 is permissible after submitting to the Federal Tax Service a completed application form in two copies, namely:

- UTII form No. 1 in 2021 for organizations;

- UTII form in 2021 No. 2 for individual entrepreneurs.

The specified templates, as well as the UTII declaration in 2021, are provided to the department at the address of the case.

For distribution/distribution commerce, transportation, transport advertising - the UTII form in 2021 is submitted at the place of registration.

At least 5 days must pass from the start of business to submit such an application.

If the case is being conducted in several regions, then it does not matter which inspection department to submit the notification to; it is enough to submit it to any office of the department in the area of doing business.

back to menu ↑

What to pay on "imputation"

One tax is an advantage of UTII in 2021. VAT, personal income tax, and payments on property are abolished (if the tax base is not considered as the cadastral value).

Activities on UTII in 2021 still involve several payments, namely: personal income tax deducted from employee salaries, insurance contributions (pension, medical, social). But they can be deducted from tax.

Important: If the property is included in a special list approved by the regional authorities and the tax regarding it is calculated according to the cadastre, and not according to the inventory value (typical of shopping centers and business centers), property tax must be paid.

back to menu ↑

A new rate will be charged. Tax legislation will be changed in Primorye

As KONKURENT.RU has learned, the government of Primorye is preparing to change tax legislation in connection with the abolition of UTII from January 1, 2021.

The White House has sent a bill to the Legislative Assembly of the Primorsky Territory to establish rates under a simplified taxation system. “The document “On the establishment of reduced tax rates when applying a simplified taxation system” was developed in order to reduce the tax burden on sectors of the economy that were most affected by the introduction of restrictive measures to prevent the spread of coronavirus infection COVID-19,” the explanatory note states ( available at KONKURENT.RU).

The bill proposes to establish a tax rate of 3% for such entrepreneurs in 2021 if the object of taxation of the entrepreneur is income.

The Ministry of Economic Development of the Primorsky Territory has calculated tax revenues in the event of the transition of all entrepreneurs from a single tax on imputed income to a simplified taxation system (if the object of taxation is income) based on the income received by the above entrepreneurs: by 6% - 3,288,029,910, 18 rub.; by 3% – RUB 1,469,428,901.09.

“There will be a decrease in the revenue side of the regional budget of the Primorsky Territory from the simplified tax system by 1,155,983,873.42 rubles, but at the same time, part of the lost income will be compensated by an increase in tax revenues from entrepreneurs who switched from the single tax on imputed income to the simplified tax system in in the amount of 672,466,732.11 rubles, which will ultimately reduce lost income by 2.4 times,” the explanatory note says.

In addition, the bill proposes to establish a tax rate of 1% under the simplified taxation system for social enterprises if the object of taxation is their income.

As of November 10, 2021, in the Primorsky Territory, 74 entrepreneurs have the status of a social enterprise, which indicates the weak interest of regional businesses in conducting activities aimed at achieving socially beneficial goals and contributing to solving social problems of society. Due to the lack of measures to support social enterprises, this category of business has no interest in confirming the status of a social enterprise (confirmed annually), according to the authors of the bill.

“Thus, the adoption of this bill will create a mechanism for supporting social enterprises in the region, contributing to the achievement of socially beneficial goals, as well as solving social problems of citizens and society; increasing the number of social enterprises in the Primorsky Territory,” the explanatory note notes.

UTII is abolished from January 1, 2021. According to the Ministry of Finance and the Federal Tax Service, the real tax burden on entrepreneurs united in large businesses is less than 1%, as a result of which the state budget does not receive significant funds. In fact, tax advantages in the form of special tax regimes are established only for small businesses and are inherently designed to create equal competitive conditions for all market participants. In this case, large retail chains are allowed to abuse advantages that neutralize the state’s efforts to provide tax support to small businesses.

It was the actions of large chains, expressed in the fragmentation of business, that led to the state’s reluctance to extend the special regime in the form of UTII.

Values K1 and K2

The table records the UTII coefficients for 2021 in exhaustive form; they are established by law. Calculation of UST in 2021 is carried out by multiplying the basic profitability by these two indicators and by the physical parameters in each month (Article 349.29 of the Tax Code). This is how the tax base is calculated.

back to menu ↑

Concept K1

UTII changes in 2021 for retail trade include correction through a deflator.

The 2021 UNDV calculation includes this figure. It has a direct impact on the basic profitability (BR) for a specific type of business.

From 2015 to 2017, K1 did not change and was equal to 1.798. In the current period, according to the order of the Ministry of Economic Development No. 579 K1 for 2021, the UNDV is 1.868.

This figure is constant and does not depend on the part of the country or the type of commerce.

With the increase in K1 for 2021, the amount of the single payment has also increased.

Despite this, this type of non-profit is still very profitable for a small enterprise.

When preparing documents for UTII in 2021, the described value is prescribed to be displayed on page 050 in R. No. 2.

back to menu ↑

What is K2 for?

Calculation of the UNDV in 2021 uses the previous value as an increasing constant.

It is unchanged for the entire country and any type of commerce, and K2 is a figure for correcting the database to reduce it.

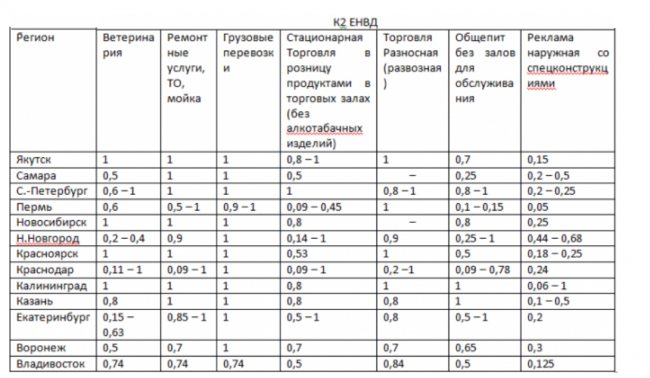

The table provides these UTII coefficients for 2021 for each type of business activity.

The table enters K2 for UTII for 2021 for 12 months, and its range is from 0.005 to 1.

If it is changed, then the new figures apply only in the following year.

At the same time, it is assumed that if K2 according to UTII for 2021 the table improves for the subject, then it can be taken into account from the date specified in the relevant act until the end of the year.

Municipal authorities are vested with the authority to change K2 for UTII in 2021.

It is by their decision that it is introduced in a specific part of the country.

Important: If the coefficient has not undergone transformations before the beginning of the year, then it remains the same throughout it. In reality, K2 rarely undergoes correction and in 2018 it remained unchanged.

back to menu ↑

Specifics of K2

The table may show different UTII coefficients for 2021 for one city.

This depends on the type of business, the place where it is run, as well as on physical indicators and the range of products sold.

UTII for LLCs in 2021 and for individual entrepreneurs has the features of K2: it may have deviations, the purpose of which is to take into account specific physical indicators of entrepreneurship (for example, seasonality).

During the calculation process, these subvalues are multiplied, and the result is K2.

If the table does not display the UTII coefficients for 2021, that is, they have not been established, but the UTII is applied, then it is assigned indicator 1.

This is the reason that in such regions the “imputation” base is stably at a constant level.

For K2 on UTII for 2021, the table and usage standards are published regularly on the regional resources of the Federal Tax Service in sections for this type of taxation.

There is also a current UTII form for 2021 and all the necessary digital values for today - payers can easily track the K2 correction for UTII for 2021.

For points of interest to business entities, you can also contact the consulting departments of tax departments.

In UTII declarations in 2021, the applied K2 is displayed on page 060 in R. No. 2. The deadline for submitting reports in 2021 UTII is at the end of the quarter.

back to menu ↑

K2 today

For K2 according to UTII for 2021, the table may have different indicators for each territory - as we wrote above, this depends on the decisions of the local authorities, approved in local acts.

All the information on the country regarding this issue is very voluminous, so here we will describe only part of it for some settlements

back to menu ↑

Deflator coefficient for UTII

“Imputers” use a deflator coefficient (another name is the K1 deflator coefficient, Article 346.27 of the Tax Code of the Russian Federation) to adjust the values of the basic profitability of a particular type of activity. The deflator coefficient for UTII for 2021 was set at 1,868 rubles. Compared to the previous value in 2021 (1.798), it increased by 3.4%. This means that even if the value of the physical indicator by type of activity remains the same and the size of K2 is set by local authorities at the same level, the “imputed” tax that you will pay to the budget will increase in 2021.

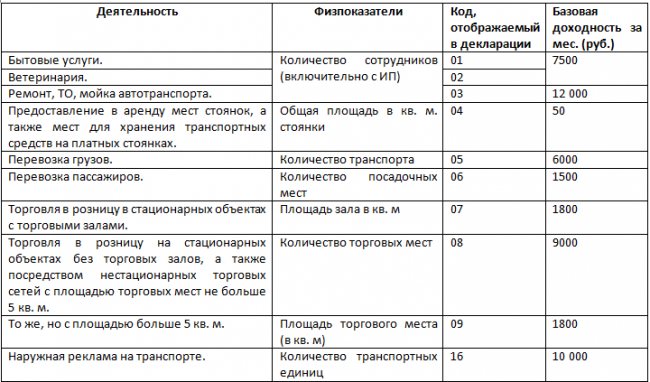

Codes and database

The calculation is carried out using the data provided by the table of basic UTII yield for 2021. DB is a conditional income based on the physical indicator. These two parameters are established by law.

The table of basic UTII yield for 2021 displays constant constants, adjusted by K1 and K2.

Let's display it along with the business codes for the declaration:

All codes and meanings are displayed in the tax code and in by-laws.

They must be strictly observed, since in case of an error, the Federal Tax Service will not accept declarations and other documents.

back to menu ↑

More about practice

Not only existing enterprises can study K2 for 2021 UTII in Murmansk. Often, clarification of current deflators is required by citizens who plan to start a business. Through simple calculations, you can come to the conclusion that providing photographic services, for example, is more profitable than sewing and repairing shoes.

Similar articles

- Basic profitability of UTII-2018 by type of activity

- UTII tax rate in 2018

- Coefficients K1 and K2 for UTII for 2021

- Value K1 for UTII from 2021

- Deflator coefficient for UTII for 2016-2017

Calculation

There are special formulas for calculation. You can also use online calculators.

To determine how much you need to pay the “imputed” person for the quarter, there is the following equation:

Basic UTII yield for 2021 x physical indicator x K1 x K2 x 15% x 3.

The figure 15% is the percentage of UTII, 3 is the duration of the period in months.

The table, partially given above, contains UTII coefficients for 2021 for each region; it is available in full on the tax authorities’ website.

back to menu ↑

Calculus example for trading

Let us give, as an example, a typical set of parameters (for UNDV in 2021, changes for retail trade are taken into account):

- type of commerce: stationary retail with halls;

- point area – 30 sq. m.;

- There are no employees, the entire business is handled by the individual entrepreneur alone.

Calculation of USTV in 2021 according to the given parameters is as follows:

- basic income for UTII for 2021 – 1800 rubles. (see table);

- FP – 30 sq. m.

- K1 for 2021 UNDV – 1.868. This is a stable value;

- K2 according to UNDV for 2021, the table for city A displays as 1;

- we substitute the values into the equation and get the result 45392.40;

- insurance premiums amounted to 7500, we deduct them: 45932.40 – 7500 = 37892 rubles. 40 kopecks

back to menu ↑

For advertising on transport

Situation parameters:

- external transport areas, number 3 pcs. This figure will be a physical indicator;

- the basic yield on UTII for 2021 is constant - 10,000 rubles. (see table above);

- K1 for 2021 UNDV – 1.868;

- K2. Local authorities have the right to differentiate different advertisements placed on transport, depending on its dimensions and other parameters, therefore the table may contain different coefficients for UTII for 2021 for each region. In our situation, advertising is commercial and has a value of 1.

Calculation of UTII in 2021 for this set of parameters: 10,000 x 3 x 1.868 x 3 x 15% = 25218.

back to menu ↑

For cargo transportation

The UTII tax in 2021 is calculated by an individual entrepreneur or an organization engaged in cargo transportation in the same way as indicated above.

The values that we indicated and the basic yield on UTII for 2021 are substituted into the formula.

Important: The basic UTII yield for 2021 may change every year, so it is highly advisable to clarify them. This can be done by going to the websites of tax departments and selecting the appropriate region of business activity.

Let's consider an example when the activity on UTII in 2021 consists of providing freight transportation services through three units of transport.

The table of basic UTII income for 2021 shows a value of 6,000 rubles, the physical indicator is 3, that is, as much as the equipment is available, while its brand and dimensions do not matter. K1 for 2018 UNDV is 1.868 and K2 in our region is 1.

We substitute all values into the equation: 6000 x 4 x 1.686 x 3 x 15% = 20,174 rubles. 40 kopecks.

Important: In all cases, if an individual entrepreneur paid insurance premiums for himself and his employees, they can be deducted from the UTII tax.

back to menu ↑

For household services

Activities on UTII in 2021 for household services are a commercial group that occupies a very significant part of the market and is especially popular for small organizations and individual entrepreneurs.

It includes repair shops, warranty centers, hairdressers, plumbing specialists and the like.

Activities on UTII in 2021 are beneficial for such entrepreneurs, as they do not involve maintaining complex reporting and at the same time have reduced rates.

Let's consider the parameters for a workshop for performing household work:

- DB is equal to 7500 rubles. We remind you that this value is stable;

- The FP for all kinds of ateliers, shoe shops, and technical workshops is equal to the number of workers. If there are 5 of them, then the value is equal to this figure. In our case, the citizen takes care of everything himself, so the value is 1;

- K1 is a constant parameter, we described this deflator above in the article, it is equal to 1.868;

- K2. This figure can be found on the website of the administration or local government where the entrepreneur runs his business. Let's say that for our city it is 0.8.

- we substitute all values into the equation: 7500 x 1 x 1, 868 x 0.8 x 15% = 1681.2. We multiply the result by the number of months in the quarter and get the final figure of 5043.6 rubles.

back to menu ↑

What is K2 UTII?

Article 346.27 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation) establishes the term for the K2 coefficient - this is an adjustment coefficient of basic profitability, which combines taking into account various features of doing business. These features include: the list of works, services or goods provided, seasonality and operating hours, the amount of income received, certain features depending on the place of business, the usable area of electronic information boards, the usable area of outdoor advertising boards, regardless of the type of image applied, the same area with a removable automatic surface, the number of cars of any type, various types of trailers and river boats that are used for placing and distributing advertising, other features. The value of this coefficient is approved by each municipal entity separately - districts, city districts, federal cities, except Moscow (the UTII system has not been used since 2014).

These values are used to calculate the UTII formula. In the UTII tax return, coefficient K2 is reflected in line 060 of section 2 of the form under KND 1152016, approved by Order of the Federal Tax Service of the Russian Federation dated July 4, 2014 N ММВ-7-3/ [email protected]

Usually, the duration of the K2 coefficient is not established, but in some cases, municipal authorities can set it for a specific year.

Sometimes it happens that K2 for UTII is not approved. In this case, it is necessary to take into account the basic profitability coefficients, which are approved by Art. 346.29 of the Tax Code of the Russian Federation for a specific type of activity, in accordance with the definition of the Supreme Arbitration Court of the Russian Federation dated May 29, 2009, No. VAS-3703/09. If, however, the coefficient has been approved, but the normative act has not yet entered into force, you can use the value of last year (this rule applies in accordance with the norms of clause 7 of Article 346.29 of the Tax Code of the Russian Federation).

Local authorities may establish a division of the K2 coefficient into sub-coefficients. In this case, to determine the value of K2, you need to multiply all the subcoefficients with each other, and then round the resulting result according to arithmetic rules to 3 decimal places, so you can get a number equal to or located between the numbers 0.005 and 1. These numbers are limit values of K2 (clause 7 of Article 346.29 of the Tax Code of the Russian Federation).

How can you reduce

For UNDV in 2021, changes for retail trade are minimal, so, as before, it can be adjusted using several techniques:

- UTII tax in 2021 for individual entrepreneurs directly depends on physical indicators - the number of personnel, space, transport units - therefore, if they are reduced, it will also decrease. One of the methods regarding retail space is to transfer some of it to utility rooms;

- combination with “simplified”;

- The UTII for an LLC in 2021 can be lowered if you submit documents stating that commercial activities have not been carried out for some time;

- deduction of insurance paid for yourself and for employees, but not more than half of the amount of the fee. The UTII tax in 2021 can be adjusted by an individual entrepreneur in this way only if it is paid before filing the declaration;

- if an online cash register was installed, then the payment can be reduced by its cost, but up to 18,000 rubles.

back to menu ↑

PRO

Vera Shcherbina, Vice-Governor of the Primorsky Territory:

— A decrease in the size of the regional coefficient implies an increase in salaries by ten percent at the expense of federal funds for workers in the compulsory medical insurance system, as well as for powers transferred from the federal level - in the field of forestry, wildlife protection, employees of military registration and enlistment offices, civil registry offices, jurors and others. At the same time, regional funds are freed up and can be used to improve the social sphere. I can responsibly declare that there will be no reduction in wages. There is a separate clause in the document that guarantees that this will not happen.

The total amount of funds that will be compensated to us from the federal budget in connection with changes in wages is estimated at 1.5 billion rubles. We will be able to use the released regional money for kindergartens, schools, courtyards, and roads.

Svetlana Krasitskaya, acting Director of the regional department of labor and social development:

— Subventions are given by the federal government for the exercise of its powers, but we cannot pay a coefficient of 1.3 from this money, since the increased obligations of the subject of the Federation in the field of remuneration are provided by the subject itself. The decision proposed by the regional administration to reduce the regional coefficient applies only to regional budgetary institutions, that is, those where the employer is the governor. Employers of companies of other different forms of ownership may still apply the coefficient of 1.3.

From a legislative point of view, we can already adopt this legal act, because two parties to the social partnership supported it (the administration of the Primorsky Territory and a number of employers. - Ed.). After finalization, it is quite possible that we will accept it. All this must be done before November 15, because employees must be warned [about the changes] two months in advance.

Reports

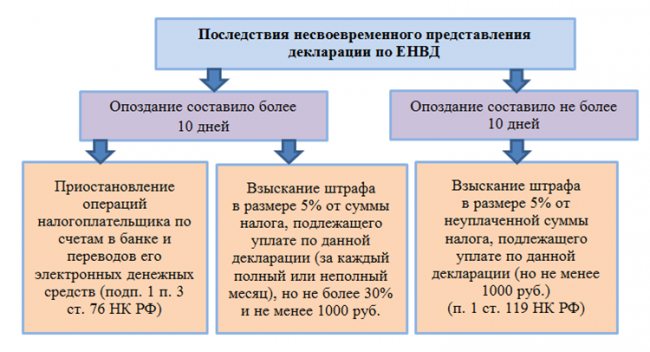

The UTII declaration in 2021 is submitted 3 months in advance, so the deadlines for submitting UTII reports in 2021 imply their preparation quarterly within a 20-day period from the date of its completion.

If the deadline falls on a weekend or holiday, it is moved to the first working day after them.

back to menu ↑

What does the deflator take into account?

Unlike K1, K2 UTII in 2021 in Perm and other regions takes into account a whole range of features of doing business:

- type of goods or services;

- list of performed works;

- K2 for 2021 UTII for the Lipetsk region takes into account the seasonality of business;

- place of services provided;

- the size of the area in which commercial activity is carried out.

The specific value of the coefficient can be found on the website of the tax service. Thus, K2 for 2021 UTII Kursk with links to resolutions is available at the address with the prefix 46. It is established by the heads of municipalities and cities of federal significance. K2 parameters for 2021 UTII in the Moscow region have not been applied since 2014.

Value K1 for UTII from 2021

What documentation is maintained?

Entities on UTII in 2021 enjoy relaxations, one of which is simplified reporting.

It is not necessary to maintain it, like accounting, but this does not mean that control and recording tools are completely abolished.

They make it possible to monitor changes in the enterprise by the relevant authorities.

"Impostors" maintain the following documentation:

- accounting of physical indicators;

- tax return (due dates for submitting reports in UTII 2021 are quarterly);

- As a rule, they also maintain a balance sheet and employee reports;

- discipline at the cash desk.

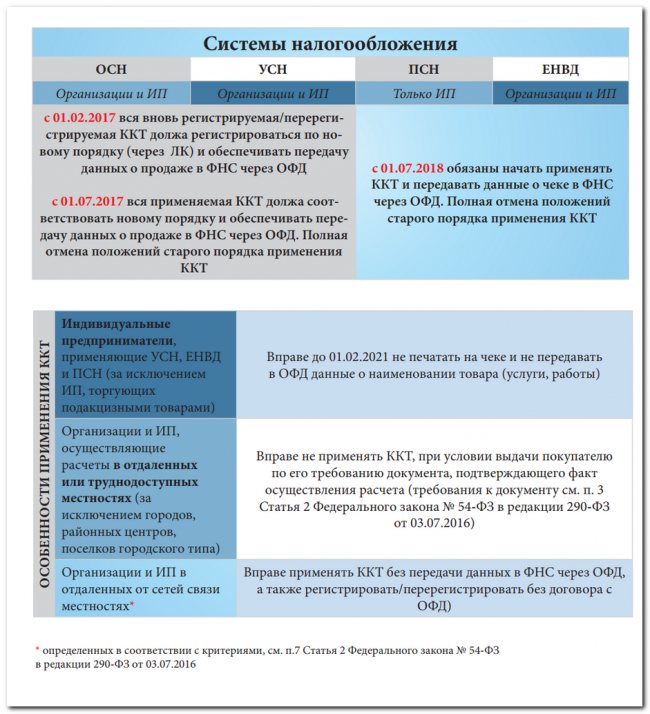

Important: In 2021, those enterprises that make payments to clients, both in cash and electronic money, are required to install and register online cash registers.

back to menu ↑

K1 and K2 in the calculation of UTII

Coefficient K1 and K2 are always involved in the calculation of UTII. The established amount of basic profitability for a certain type of activity is multiplied by these indicators.

Knowledge of the coefficients allows the entrepreneur to independently make calculations for the single tax, as well as compare the data obtained with the results of calculations by tax officials. In case of discrepancies, the error can be identified in a timely manner and possible disputes can be resolved.

Similar articles

- Deflator coefficient for 2021 for UTII

- Basic yield

- Basic profitability of UTII-2018 by type of activity

- Latest changes in the Tax Code of the Russian Federation on UTII

- Deflator coefficient for UTII for 2016-2017

Rules for cash registers

In 2021, UTII changes regarding cash registers are as follows.

In order to take advantage of the benefit of deducting their cost, an individual entrepreneur must register a cash register from 02/01/2017 to 07/01/2019.

If this is catering or retail trade, then the device must be registered from 02/01/2017 to 07/01/2018.

Individual entrepreneurs can reduce the UTII tax in 2021 by these amounts when calculating for 2018-2019, but not earlier than the year the cash register is registered.

back to menu ↑

Deflator coefficient for trade tax

Trade fee payers use a deflator coefficient to adjust the fee rate determined for activities related to the organization of retail markets (clause 4 of Article 415 of the Tax Code of the Russian Federation). The basic value of this rate is 550 rubles per 1 square meter of retail market area. The coefficient value for 2021 was 1.237. For 2018, the coefficient will increase to 1.285. Accordingly, the fee rate for this type of activity in 2021 will increase and amount to 706.75 rubles (550 rubles × 1.285).

When the right is lost

The right to UTII in 2021 disappears if the entity ceases to meet the parameters specified in the law, namely: if the number of employees has become more than 100 people, trust management agreements are used, with an increase in the share of other organizations (over 25%).

And also, if the activity changes and it is not on the list as one for which this right is provided.

UTII in 2021 for retail trade according to these parameters has not undergone any changes.

After losing the right, a businessman can close his business or immediately switch to a different taxation system, choosing it from among those available according to his parameters, for example, the simplified tax system and submitting the appropriate documents to the tax authorities.

back to menu ↑

How to deregister

If the imputed activity under UTII for an LLC is terminated in 2021, then the payer, within 5 days after its completion, must submit a UTII form in 2021 to the tax authorities in the form (organization). The same applies to individual entrepreneurs (form No. 4).

The filing rules are standard: at the place of registration or at the place of registration for distribution trade and transportation.

The payer is removed from the form within a 5-day period from the date of submission of the notification to the inspection.

It should be noted that all actions can be carried out through the MFC; applications can also be submitted through the government services website.

In these cases, you need to take into account the time required to transmit information to the Federal Tax Service, so the period may increase by several days.

Important: You can change UTII to another regime only from the beginning of the next year, except in situations where an “imputed” business is terminated, an individual entrepreneur or organization is liquidated, and also when the conditions do not meet the requirements for this type of taxation.

A single tax on imputed activity is ideal for small businesses.

Its advantages: simple reporting, the amount of UTII in 2021 is stable and it is possible to deduct insurance premiums from it.

It is planned to abolish it and remove it from the n/o system, but this has not yet been done.

Regarding UTII in 2021, the changes and news for retail trade are encouraging - this regime has been extended until 2021.

back to menu ↑

How to calculate UTII. Calculation of the amount of tax on UTII

Buh-Ved.RU

IP » IP accounting » K2 UTII in St. Petersburg

See also the features of K2!!

* Law of St. Petersburg dated June 17, 2003 N 299-35 (as amended on November 21, 2008) “ON THE INTRODUCTION OF A TAX SYSTEM IN THE TERRITORY OF ST. PETERSBURG IN THE FORM OF A UNIFORM TAX ON IMPLIED INCOME FOR CERTAIN TYPES OF ACTIVITY” (adopted by the Legislative Assembly of St. Petersburg 06/04/2003 )

* Law of St. Petersburg dated June 30, 2005 N 411-68 “On the territorial structure of St. Petersburg” link subparagraph 1 clause 1, subclause 2, clause 1

| № | Type of business activity | The meaning of K 2 in St. Petersburg, subparagraph 1, paragraph 1, article 2 | The meaning of K 2 in St. Petersburg, subparagraph 1, paragraph 2, article 2 |

| 1 | Provision of household services, incl. | ||

| 1.1 | Shoe repair, painting and sewing, incl. | ||

| 1.1.1 | Sewing orthopedic shoes (OKUN 011305) | 0,2 | 0,2 |

| 1.1.2 | Other types of household services for repair, painting and sewing of shoes ( OKUN 011100-011410, with the exception of 011305) | 0,4 | 0,2 |

| 1.2 | Repair and sewing of clothing, fur and leather products, hats and textile haberdashery products, repair, sewing and knitting of knitwear ( OKUN 012100-012605 ) | 0,6 | 0,4 |

| 1.3 | Repair and maintenance of household radio-electronic equipment, household machines and household appliances, repair and manufacture of metal products ( OKUN 013100-013451 ) | 0,8 | 0,6 |

| 1.4 | Furniture repair ( OKUN 014201-014210, 014301-014305, excluding furniture manufacturing 014307-014309) | 0,6 | 0,4 |

| 1.5 | Dry cleaning and dyeing, laundry services ( OKUN 015100-015421 ) | 0,4 | 0,2 |

| 1.6 | Repair and construction of housing and other buildings ( OKUN 016100-016314, except 016201 ) | 1,0 | 1,0 |

| 1.7 | Services of photo studios and photo and film laboratories, transport and forwarding services ( OKUN 018100-018331 ) | 0,6 | 0,4 |

| 1.8 | Services of baths and showers, hairdressing salons. Rental services. Ritual, ceremonial services ( OKUN 019100-019752, with the exception of 019701-019712 ) | 0,6 | 0,4 |

| 1.9 | Performing translations from one language to another, including written translations made by modifying automatic translation ( OKUN 019753) | 1,0 | 1,0 |

| 2 | Provision of veterinary services, incl. | ||

| 2.1 | In veterinary hospitals | 0,6 | 0,6 |

| 2.2 | Outside veterinary hospitals | 1,0 | 1,0 |

| 3 | Providing repair, maintenance and washing services for vehicles | 1,0 | 1,0 |

| 4 | Provision of services for the provision of temporary possession (for use) of parking spaces for vehicles, as well as for the storage of vehicles in paid parking lots (with the exception of penalty parking lots) | 1,0 | 1,0 |

| 5 | Provision of motor transport services for the transportation of goods | 1,0 | 1,0 |

| 6 | Provision of motor transport services for the transportation of passengers | 0,25 | 0,25 |

| 7 | Retail trade carried out through objects of a stationary retail chain that do not have sales floors, as well as through objects of a non-stationary retail chain, the area of a retail space in which does not exceed 5 square meters, including: | ||

| 7.1 | Retail trade in milk and dairy products, bread and bakery products | 0,4 | 0,2 |

| 7.2 | Retail trade of other types of products | 1,0 | 0,5 |

| 7.3 | Sale through vending machines of goods and/or catering products manufactured in these vending machines | 0,4 | 0,2 |

| 8 | Retail trade carried out through objects of a stationary retail network that do not have trading floors, as well as through objects of a non-stationary retail network, the sales area of which exceeds 5 square meters, including: | ||

| 8.1 | Retail trade in milk and dairy products, bread and bakery products | 0,2 | 0,1 |

| 8.2 | Retail trade of other types of products | 0,3 | 0,2 |

| 9 | Delivery and distribution retail trade | 1,0 | 0,8 |

| 10 | Provision of public catering services through public catering facilities that do not have visitor service areas | 1,0 | 0,8 |

| 11 | Advertising on vehicles | 1,0 | 1,0 |

| 12 | Distribution of outdoor advertising using advertising structures (except for advertising structures with automatic image changes and electronic displays), including: | ||

| 12.1 | With an information field area of no more than 18 square meters | 0,25 | 0,25 |

| 12.2 | With an information field area of more than 18 square meters | 0,2 | 0,2 |

| 13 | Distribution of outdoor advertising using advertising structures with automatic image changes, including: | ||

| 13.1 | With an information field area of no more than 18 square meters | 0,25 | 0,25 |

| 13.2 | With an information field area of more than 18 square meters | 0,2 | 0,2 |

| 14 | Distribution of outdoor advertising through electronic displays, including: | ||

| 14.1 | With an information field area of no more than 18 square meters | 0,25 | 0,25 |

| 14.2 | With an information field area of more than 18 square meters | 0,2 | 0,2 |

| 15 | Provision of services for the transfer for temporary possession and (or) use of retail spaces located in facilities of a stationary retail chain that do not have trading floors, facilities of a non-stationary retail chain, as well as public catering facilities that do not have customer service areas, if the area of each they do not exceed 5 square meters | 1,0 | 0,8 |

| 16 | Provision of services for the transfer for temporary possession and (or) use of retail spaces located in facilities of a stationary retail chain that do not have trading floors, facilities of a non-stationary retail chain, as well as public catering facilities that do not have customer service areas, if the area of each exceeds 5 square meters | 0,7 | 0,55 |

| 17 | Retail trade carried out through stationary retail chain facilities with trading floors, including: | ||

| 17.1 | Objects of a stationary retail chain that have trading floors in which the volume of sales of one group of goods is determined on the basis of GOST R 51303-99 “Trade. Terms and definitions”, approved by Decree of the State Standard of Russia of August 11, 1999 N 242-st, is at least 80 percent in value terms of the total volume of sales of goods selling: | ||

| 17.1.1 | Products subject to excise taxes | 1,0 | 1,0 |

| 17.1.2 | Computer equipment, television and radio products, musical instruments; means of communication; porcelain, crystal, jewelry; vision correction products | 1,0 | 0,8 |

| 17.1.3 | Bread and bakery products; milk and dairy products, baby food and diabetic products, children's products; fresh flowers, seeds, seedlings, seedlings, planting materials | 0,3 | 0,1 |

| 17.1.4 | Goods accepted from citizens on commission terms (except for audio and video equipment, computers and communications) | 0,07 | 0,07 |

| 17.1.5 | Other types of products | 0,5 | 0,4 |

| 17.2 | Other objects of a stationary retail chain that have trading floors that are open at least 20 hours a day | 1,0 | 0,8 |

| 17.3 | Other facilities of a stationary retail chain with trading floors operating less than 20 hours a day | 0,5 | 0,4 |

See also the features of K2!!

* Law of St. Petersburg dated June 17, 2003 N 299-35 (as amended on November 21, 2008) “ON THE INTRODUCTION OF A TAX SYSTEM IN THE TERRITORY OF ST. PETERSBURG IN THE FORM OF A UNIFORM TAX ON IMPLIED INCOME FOR CERTAIN TYPES OF ACTIVITY” (adopted by the Legislative Assembly of St. Petersburg 06/04/2003 )

* Law of St. Petersburg dated June 30, 2005 N 411-68 “On the territorial structure of St. Petersburg” link subparagraph 1 clause 1, subclause 2, clause 1