The Labor Code requires the employer to pay the wages employees deserve at least twice a month. The first such payment is called an advance payment, since it is accrued before the month worked has expired.

- What proportion of the total salary should the advance be?

- When exactly does it need to be paid?

- What are the consequences for an employer of ignoring advance payments?

All questions regarding the advance are discussed below.

Question: Organizations are required to pay wages for the first half of the month, taking into account the time worked by the employee. Some companies apply a coefficient of 0.87 to the calculated advance payment. Does the employer underestimate the salary for the first half of the month in such a situation? View answer

What documents regulate the advance?

In no way, since the official term “advance” does not exist in labor legislation. This is a colloquial, established name for the first part of the salary, which must be paid at least twice a month (Article 136 of the Labor Code of the Russian Federation).

REFERENCE! The second part is traditionally called “pay” or “salary” itself, although in fact the salary is both payments together.

Question: Until recently, salaries in our organization were paid twice a month. Currently, they offered to write a statement refusing the advance payment and stated that the salary would be calculated once a month. Is this legal? View answer

Therefore, instead of the term “advance”, the legislation uses the expression “procedure for payment of wages”. And this procedure already has a strict documentary justification in the internal acts of the organization:

- collective agreement;

- internal rules of the company;

- individual employment contracts;

- Regulations on the enterprise.

Question: What type of income code should be indicated in the payment order when paying an advance (that is, from wage income for the first half of the month), if the employer withholds 70% of the salary from the salary once a month according to writs of execution, so that according to new writs the bank Didn't make the deduction yourself? View answer

What transactions should be used to reflect the offset of advances with the supplier?

Hello! LLC on the simplified tax system for income. Doubts arose about the correctness of the transactions generated by the program. Help, I really want to understand. November 07, 2021 - an offer agreement for access to the web service was concluded November 07, 2021 - Dt 60.02 - Kt 51 9326 rub. — Paid for access for the period until November 06, 2021 (write-off from the account. Let’s call it write-off No. 1) Then monthly acts were carried out, for each act the advance was offset and this amount was written off as expenses in parts, so that by the end of the period (by 6 November 2018) the entire amount was written off. Postings for each act were according to the principle: November 30, 2021 - Dt 60.01 - Kt 60.02 590 rub. — offset of the advance payment to the supplier (write-off from the account No. 1, act No. 1) November 30, 2021 - Dt 20.01 - Kt 60.01 590 rub. — Providing access to the web service for November 2021 by entry. 3810 dated November 30, 2017 (act No. 1) As of October 31, 2021, almost the entire amount was closed and the balance was 26 rubles (the act for November 2021 was supposed to be closed in November 2018). At the same time, in July 2021, the supplier offered discounts for the next period and we paid at a discount (same agreement): July 12, 2021 - Dt 60.02 - Kt 51 7020 rub. — Paid access for the period from November 07, 2021 to November 06, 2019 (write-off from the account. Let’s call it write-off No. 2) Act No. 31 in the amount of 7020 was issued to us on 11/02/2018, and act No. 28 for the balance of the first advance (26 rubles) issued on November 22, 2018. And here I have a question, have I formed the correct postings: according to act No. 31: November 02, 2018 - Dt 60.01 - Kt 60.02 - 26 rubles. offset of advance payment to supplier (write-off from account No. 1, act No. 31) November 02, 2021 - Dt 60.01 - Kt 60.02 - 6994 rub. offset of advance payment to supplier (write-off from account No. 2, act No. 31) November 02, 2021 - Dt 20.01 - Kt 60.01 - 7020 rub. The right to use 2 user connections. Subscription for 1 year for the period 07.11.2018 - 06.11.2019 by entry. 5150 from 02.11.2018 (act 31) according to act No. 28: November 22, 2021 - Dt 60.01 - Kt 60.02 - 26 rubles. offset of advance payment to supplier (write-off from account No. 1) November 22, 2021 - Dt 20.01 - Kt 60.01 - 26 rubles. Providing access to the web service for November 2018 by entry. 3810 from November 22, 2018 (Act 28) If you have the patience to read, then thank you!

When is the advance paid?

The date separating the payment terms is chosen by the enterprise arbitrarily. The law does not give strict instructions in this regard, however, there are recommendations from Rostrud, the Ministry of Social Development of the Russian Federation and the Federal Service for Labor and Employment, based on the logic of things.

When is the advance payment and the second part of the salary paid ?

Since remuneration for labor must be paid for the time actually worked and occurs twice a month, it is quite logical to divide the month approximately in half and choose the 15th-16th as the payment date.

FOR YOUR INFORMATION! With this choice of payment dates, it is recommended to divide the salary into approximately equal parts.

However, in the absence of strict legal requirements, the entrepreneur has some freedom in choosing dates for salary payments. You just need to take into account some nuances:

- it is allowed to divide payments not necessarily into 2 parts, you can split the salary into smaller shares, paying it three or four times a month, then the logic for setting dates will be different;

- if the gap between the advance and pay is more than 15 days, then according to the law, the employee theoretically has the right to complain about the delay in wages, suspend work and even go to court;

- the selected time periods must be recorded in the internal documents of the organization.

NOTE! The time for paying the advance must be a specific date, not a period. It is impossible to schedule advance payments, for example, from the 5th to the 10th, and paydays from the 25th to the 30th. Thus, the requirement to comply with the frequency of payments is violated.

If the appointed date coincides with a weekend or holiday, the employee will receive the required advance payment the day before.

Question: Is it necessary to calculate and transfer personal income tax to the budget from an advance payment of wages (clause 2 of Article 223, clause 6 of Article 226 of the Tax Code of the Russian Federation)? View answer

Advance share of salary

What amount or share will the first payment of part of the salary be? The law does not answer clearly here either. Of the documents, this issue is indirectly addressed only by the somewhat outdated, but not yet repealed, Resolution of the USSR Council of Ministers No. 566, which states that the amount is established by the organization and should not be lower than the tariff rate.

Is it necessary to withhold alimony from advance wages ?

In modern entrepreneurship, various methods of calculating the advance interest are used, all of them are legal, the choice is up to the employer.

- Payment for actual working hours. The advance is paid on a set date in an amount corresponding to remuneration for the number of days or hours worked. However, it may vary monthly. This method is recommended in the letter of the Ministry of Labor No. 14-1/10/B-660; it must be mentioned in internal documents.

- Fixed percentage of the salary amount. It is more convenient for calculations, since it will be the same at constant wages. It is attractive for employees because they always know how much they can count on by a certain date. If the monthly payments are divided in half, it is convenient to pay half of the due remuneration. A level of 40% is also acceptable; a smaller share is not accepted.

- Fixed amount. An entrepreneur has the right to pay not a share of the salary, but a part of it in the form of the same amount, and recalculate the rest in accordance with the time worked. With this method, the advance payment will remain unchanged, and subsequent payments may differ under different remuneration systems (they will be the same for a fixed salary, but may change for hourly or piecework wages).

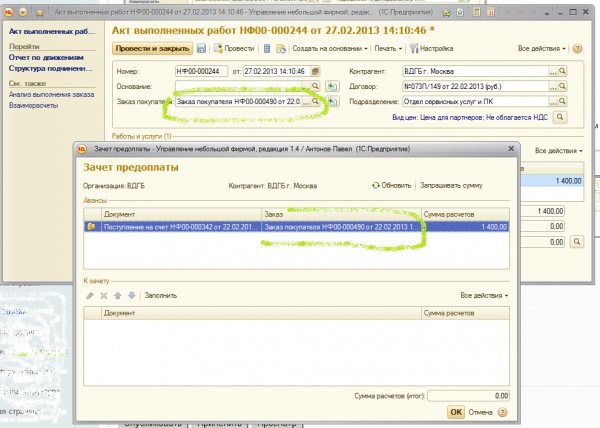

Error No. 2. Advance payment upon shipment was not credited

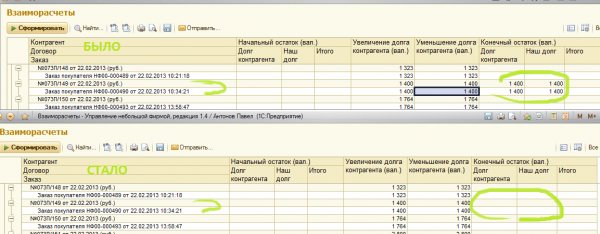

Again we see that the same amount for the order is in our debt and in the debt of the counterparty, and the total debt is 0.

in the transcript of the report we see that in this case the shipment occurred later than the payment, but for some reason the advance payment was still not credited (perhaps the payment document was recorded on a date earlier than the shipment, but was posted later than the shipment document)

it is necessary to open the shipment document (in the case of several documents, open them one by one, having previously unchecked them.)

we see in the document. that the settlement amount = 0, that is, the advance payment was not credited upon shipment, most often you just need to click the “post” button and the advance payment will be credited. but you can also count it manually for reliability; to do this, press the button (pointed to by the pink arrow)

we see that in the prepayment offset table, there is an advance payment exactly for the required amount for the same order. We count this amount.

After the transaction, we get the following picture: everything has been accounted for perfectly and there are no debts on debit or credit.

How to calculate the advance amount

The salary mass includes not only the tariff rate, but also compensation, social charges, allowances, bonuses, etc. They are taken into account when dividing the payment amount.

For an advance payment, you need to take into account part of the tariff rate (salary), bonuses for experience and qualifications, compensation charges, and social subsidies.

The bonus share, if it is due, may well not be included in the advance payment, since in most cases the bonus is accrued or not accrued depending on the results of the month, which has not yet expired at the time of payment of the advance payment.

Profit tax is required to be withheld from wages. How does it affect the amount of the advance? 13% of personal income tax is deducted at the end of the month, so the first payment occurs without this deduction. The same applies to contributions to social funds. They are deducted from the salary, and the advance is only part of it.

Results

Settlements with suppliers involve the use of account 60 with the opening of sub-accounts for it, provided for by the working chart of accounts of an economic entity. In addition to account 60, account 76 may also be involved in such operations. Payments to suppliers are reflected in the debit of these accounts. The choice of the account corresponding to the loan will depend on how the payment was made: non-cash (from a current, foreign currency or specialized bank account) or in cash.

When preparing documents in the 1C Accounting program, some accountants do not check the transactions that this document generates. In this article we will describe the main mistakes when accounting for settlements with suppliers and customers.

If you work with suppliers on an advance payment basis, turnover invariably appears in account 60.02 “Advances issued”.

After you post a document on the receipt of assets, be sure to generate SALT on account 60 and make sure that the advance payment to the supplier is offset. The program should generate the following transactions:

Dt 60.02 Kt 60.01 – offset of advance payment

Dt X (asset account) – Kt 60.01 – for the amount of the cost of the asset excluding VAT

Dt 19…. Kt 60.01 – for the amount of VAT

Related course

1C: Accounting 8.3

If, when generating SALT, you see the balance on the Credit of account 60.01 and exactly the same amount on the Debit of account 60.02, then the “Advance Offset” posting may not have been generated. This can happen for two reasons:

- Different agreements are indicated in the document for debiting funds from the current account and in the receipt document.

- Perhaps you unloaded the bank later than you posted the receipt document.

For exactly the same reason, you may not be able to generate a posting for offsetting the advance from the buyer on account 62. / “Accounting Encyclopedia “Profirosta” 10/01/2017

Information on the page is searched for by the following queries: Accountant courses in Krasnoyarsk, Accounting courses in Krasnoyarsk, Accountant courses for beginners, 1C: Accounting courses, Distance learning, Accountant training, Training courses Salaries and personnel, Advanced training for accountants, Accounting for beginners Accounting services, VAT declaration, Profit declaration, Accounting, Tax reporting, Accounting services Krasnoyarsk, Internal audit, OSN reporting, Statistics reporting, Pension Fund reporting, Accounting services, Outsourcing, UTII reporting, Bookkeeping, Accounting support, Provision of accounting services services, Assistance to an accountant, Reporting via the Internet, Drawing up declarations, Need an accountant, Accounting policy, Registration of individual entrepreneurs and LLCs, Individual entrepreneur taxes, 3-NDFL, Accounting organization

The employer does not pay an advance

If an employer neglects his obligation to pay remuneration for work at least twice a month, this is a direct violation of the law. Such an administrative offense is subject to punishment, according to Article 5.27 of the Code of Administrative Offenses of the Russian Federation:

- officials who established an unlawful procedure for calculating salaries will have to pay a fine in the amount of 1-5 thousand rubles, and in the event of a relapse of such a violation - 10-20 thousand rubles, and possibly receive disqualification for 1-3 years;

- Individual entrepreneurs are required to provide at least two-time payments, otherwise they face a fine of 1-5 thousand or 10-20 thousand in case of repetition;

- a legal entity is liable to its employees for a fine of 30-50 thousand rubles, and repeated involvement is fraught with amounts of 50-70 thousand rubles.

IMPORTANT! The amount of fines is paid to the budget. Additionally, an employee who has suffered from late payment of salary has the right to demand compensation for its delay (Article 235 of the Labor Code of the Russian Federation).

Also read: where to go if you don’t get paid

Postings for advances issued in favor of the supplier

To account for advances transferred by the enterprise to pay for services, work and finished products, account 60 is used. The organization carries out settlements with accountable persons using account 71.

Reflection of the prepayment transferred to the seller for raw materials and materials

Let's consider an example: I ordered raw materials for the production of products from the Atlet enterprise and paid 48,000 rubles in advance on 04/05/2015. 06/01/2015 Atlet supplied raw materials to the Sigma warehouse.

The customer’s accounting must reflect the following accounting entries for the advance:

| Dt | CT | Description | Sum | Base |

| 60.02 | 51 | The advance payment issued to the Atlet enterprise was transferred | 48,000 rub. | invoice |

| 10/1 | 60.01 | Atlet supplied raw materials and materials in full | RUB 39,360 | waybill |

| 19/3 | 60.01 | VAT (18% of the cost of the goods received) | RUB 8,640 | waybill |

| 60.01 | 60.02 | Crediting the supplier's advance upon delivery of goods | 48,000 rub. | waybill |

| 68.02 | 19.03 | VAT credit upon delivery of goods | RUB 8,640 | waybill |

How to reflect an advance to an employee for business needs

Inter LLC issued to its employee Sviridov V.P. advance payment in the amount of 5,200 rubles for the purchase of stationery. Sviridov purchased office supplies in the amount of 4,850 rubles, and returned the remaining unused funds of 350 rubles to the cash desk of Inter LLC.

| Dt | CT | Description | Sum | Base |

| 71 | 51 | Sviridov received an advance on his card account | 5,200 rub. | application for funds |

| 10 | 71 | Reflection of purchased goods | 4,850 rub. | expense report |

| 50 | 71 | Sviridov returned unspent funds to the cash register | 350 rub. | expense report |

Accounting entries for advance payment

Accounting arrangements depend on the method of payment of the advance. Most often, it is transferred, like the rest of the salary, to a bank card . In this case, you must correctly indicate the purpose of the payment, mentioning the month of calculation, for example, “salary for half of August 2021.” Two entries are required: for the transfer of advance funds - debit 70, credit 50, and for the bank commission - debit 91-2, credit 51.

The law allows advance payment in other ways:

- in cash: you need to fill out a statement of the T-53 form provided for this or a KO-2 cash order;

- in non-monetary equivalent: part of the salary can be in kind, Art. 131 of the Labor Code of the Russian Federation allows this, regulating that its share should not exceed 20%; Thus, according to accounting, “transfer of finished products to payroll” occurs, and postings take place in 5 stages: revenue from finished products (debit 70, credit 50-1), writing off the cost of production (debit 90-2, credit 43), accrual VAT (debit 90-3, credit 68), profit or loss from transfer to salary account (debit 90-9 or 99, credit 99 or 90-9, respectively).

Postings for advance received from buyer

If an enterprise receives an advance payment for services or work that have not yet been completed under the contract, then such an advance is accounted for in account 62. This account is also used when funds are received for any products that were not delivered to the customer at the time the money was received.

An example of a reflection of an advance received for goods (services, work)

Let’s say that “Factor” has entered into an agreement for the supply of printed products, where “Omega” is the supplier and “Factor” is the buyer. The contract amount is 321,000 rubles. On 10/01/2015 the customer makes full prepayment under the contract. On November 1, 2015, the supplier transfers part of the goods in the amount of 120,000 rubles.

This operation will look like this:

| Dt | CT | Description | Sum | Base |

| 51 | 62.02 | Receipt of advance payment from the buyer to the account | RUB 321,000 | invoice, bank statement |

| 62.02 | 68 | VAT accrual (18% of the advance amount) | RUB 48,966 | invoice, bank statement |

| 62.01 | 90/1 | Supply of printed products | 120,000 rub. | waybill |

| 90/3 | 68 | VAT accrual (18% of the delivery cost) | RUB 18,305 | waybill |

| 68 | 62.02 | VAT recovery | RUB 18,305 | waybill |

| 62.02 | 62.01 | Closing the received advance for the amount of goods delivered | 120,000 rub. | waybill |