Basic rules for filling out the Statement of Changes in Capital

The statement of changes in capital is completed for the calendar year from January 1 to December 31.

In addition, it provides data on the amount and changes in capital for the last year and the amount of capital for the year before last (clauses 10, 13 of PBU 4/99).

To fill out the Statement of Changes in Capital, you will need synthetic and analytical accounting data for accounts 80 “Authorized capital”, 81 “Own shares (shares)”, 82 “Reserve capital”, 83 “Additional capital”, 84 “Retained earnings (uncovered loss) "

If any data is missing, dashes are added to the lines of the Statement of Changes in Capital.

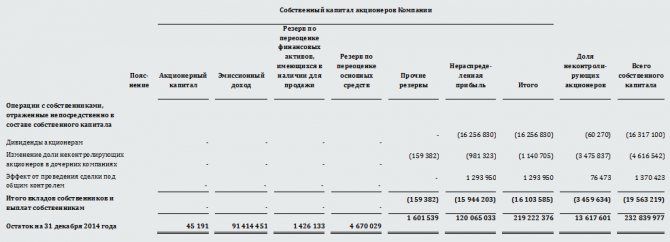

Statement of changes in capital (form 3) for 2014

Source: Glavbukh magazine

Statement of changes in capital (Form 3) includes:

- Section 1 “Movement of capital”;

- Section 2 “Adjustments due to changes in accounting policies and correction of errors”;

- Section 3 “Net Assets”.

In the standard form of the Statement of Changes in Equity, the lines are not numbered. The codes for the lines are given separately in Appendix 4 to the order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n.

Lines must be numbered in accordance with approved codes when an organization submits reports to statistical authorities and other executive authorities.

If reporting is prepared for shareholders or other users who are not executive authorities, it is not necessary to number the balance sheet lines. This follows from paragraph 5 of Order No. 66n of the Ministry of Finance of Russia.

Section 1

Section 1 of the report reflects information about the change:

authorized capital (account 80);

own shares purchased from shareholders (account 81);

additional capital (account 83);

reserve capital (account 82);

retained earnings (uncovered loss) (account 84).

Section 1 consists of two parts. The first part reflects the indicators for the previous year. The second part contains similar indicators for the reporting year.

Fill out the first part of section 1 based on the data that was reflected in the second part of this section in the Statement of Changes in Capital for the previous year.

Fill out the second part of section 1 based on accounting data for the reporting year.

Fill out the report lines depending on the type of transactions as a result of which the organization’s capital has changed. If there are no necessary lines to reflect any operations in the report form, add them yourself.

For example, the form does not provide lines to reflect the use of net profit to pay bonuses, financial assistance, pay for employee vouchers, etc.

Therefore, when preparing a report, an accountant can reflect these transactions in additionally entered lines.

Adjustment of indicators for previous years

The indicators of the statement of changes in capital (Form 3) for the reporting period and the two previous years must be comparable.

Incomparability of indicators may arise if significant errors from previous years were identified in the reporting year and (or) the organization’s accounting policies changed.

In this case, the indicators for previous years must be adjusted based on the conditions in force in the current year. At the same time, do not change the Statement of changes in capital for previous periods.

Sections 2 and 3

The amount by which the amount of capital has changed is reflected in section 2 “Adjustments due to changes in accounting policies and correction of errors.”

In Section 3 “Net Assets” you need to provide information on the amount of net assets as of December 31, 2014 and the previous two years.

The procedure for assessing net assets was approved by order of the Ministry of Finance of Russia dated August 28, 2014 No. 84n. This procedure applies to both JSC and LLC.

The procedure for calculating net assets has changed slightly compared to last year. Liabilities must be subtracted from the amount of assets reflected in the balance sheet, as before. But unlike previous rules, it is now required to include future income in the calculation. An exception is cases when these incomes arise from receiving government assistance or gratuitous property.

The new rules are effective from November 4, 2014. But in fact, companies need to take them into account for the first time when preparing financial statements for 2014.

Let's give an example of how to fill out a statement of changes in capital (Form 3).

Example

When preparing financial statements for the current year, the accountant of Hermes Trading Company LLC calculated the amount of the organization’s net assets. The calculation was made based on balance sheet indicators for the current year. As of December 31, 2014, the balance sheet assets reflected:

- on line 1130 “Fixed assets” – 100,000 rubles;

- on line 1210 “Inventories” - 400,000 rubles;

- on line 1230 “Accounts receivable” – 150,000 rubles. There are no debts of participants regarding contributions to the authorized capital;

- on line 1250 “Cash” – 200,000 rubles.

As of December 31, 2014, the liabilities side of the balance sheet reflected:

- on line 1310 “Authorized capital (share capital, authorized capital, contributions of partners)” - 50,000 rubles;

- on line 1370 “Retained earnings (uncovered loss)” - 100,000 rubles;

- on line 1520 “Short-term accounts payable” – 605,000 rubles.

All balance sheet asset indicators are taken into account when calculating net assets. Balance sheet liability indicators are taken into account only in terms of accounts payable. The net assets of Hermes as of December 31 of the current year are: 100,000 rubles. + 400,000 rub. + 150,000 rub. + 200,000 rub. – 605,000 rub. = 245,000 rub.

This amount was included in section 3 “Net assets” of the statement of changes in capital (Form 3).

Source: //otchetonline.ru/art/buh/44420-otchet-ob-izmeneniyah-kapitala-forma-3-za-2014-god.html

General requirements for completing the Statement of Changes in Capital

The statement of changes in equity consists of three sections.

Section 1 is devoted to the movement of capital of the company. It should reflect data on the authorized, additional and reserve capital, as well as on own shares purchased from shareholders, and on the amount of retained earnings (uncovered loss). The data in the form is indicated not only for the reporting year, but also for the two previous years. Thus, in the report for 2021, in addition to the data of the current reporting period, information is provided for 2015 and 2014.

The indicators of the reporting year and previous years, which are indicated in the report, must be comparable. This allows you to analyze them in dynamics. If the company’s accounting policy did not change significantly in the reporting year, then the indicators for the previous year will coincide with the data of the previous report. If the accounting policy has changed, then it is impossible to rewrite data from last year’s document into a new report. It is necessary to make adjustments, and the reasons for the discrepancies in the indicators relating to the previous year should be indicated in the explanatory note.

In Sect. 2 reports provide information on adjustments that are associated with changes in accounting policies and correction of errors. Indicators are reflected both before and after adjustment.

In Sect. 3 enter data on the company’s net assets in the reporting and two previous periods.

The statement of changes in capital is signed by the head of the company and its chief accountant.

The tabular part of the report is filled out in thousands or millions of rubles (codes 384 or 385).

Statement of changes in equity: Form 3

The last day of March 2021 is the deadline for submitting annual financial statements to the Tax Inspectorate and Rosstat.

Almost all Russian organizations are required to provide information about their financial and property status in established forms.

One of these forms of accounting is a report on changes in the company's capital. Let's talk about the key features of filling out the report.

Unified forms of financial reporting for economic entities of Russia were approved by Order of the Ministry of Finance No. 66n, which included the so-called form No. 3 (OKUD 0710003).

There are two forms available for this type of reporting.

1. Report on changes in capital - a form with line codes that must be filled out when sent to the regulatory authorities.

2. A form without line-by-line codes, which is used within an economic entity, for example, by management.

Please note that Form No. 3 is not mandatory for all economic entities. Thus, the report on changes in capital, who must submit it, is defined in Order of the Ministry of Finance No. 66n. These include organizations that carry out accounting using the main method. But companies that maintain simplified accounting may not submit these reports.

Report structure

The structure of the reporting form provides for the reflection of accounting data in the title page and three tables:

- The title page contains registration information about the reporting economic entity. Here you should indicate the reporting period, the full name of the organization, its INN, KPP, type of economic activity (code) and OKPO, register the organizational and legal form, and also indicate the form of ownership.

- The first table, “Capital Movements,” contains information grouped by type of capital and by methods of change in recent years. In this section it is necessary to reflect systematic information on turnover and balances on accounting accounts.

- The second table “Adjustments due to changes in accounting policies and correction of errors” provides information on changes in the size and structure of capital. Moreover, in the second block of the reporting form, not all changes should be indicated, but only those that are due to adjustments to the company’s accounting policies, which resulted in the recalculation of indicators. This block also reflects errors identified in accounting, the correction of which also adjusted the organization’s financial capital indicators.

- The third table, “Net Assets,” represents the sum of the financial assets of the enterprise that will remain at the disposal of the economic entity after the repayment of all debt obligations and debts. Read more about the calculation of this indicator in the article “Net assets on the balance sheet”.

Note that the second table is filled in only if there is appropriate data to reflect.

Features of filling out the statement of changes in capital 2021

When drawing up the reporting form, you should be guided by the rules and requirements approved by Order of the Ministry of Finance No. 66n. Let us note the key features of how to fill out a statement of changes in capital.

Fill out the title page of the form. We indicate the relevant information about the organization in accordance with the constituent documents.

We enter the data in section one.

The first table has a breakdown of indicators by reporting financial periods. The first part reflects data for the previous year, the second - for the reporting period. Please note that the indicators for these years must coincide; deviations are unacceptable.

Data for entry should be generated by type of capital according to the following synthetic accounts:

- according to account 80 - reflection of the authorized capital;

- sch. 81 - transactions with own shares that were purchased from shareholders;

- sch. 82 - when determining the volume of reserve capital;

- sch. 83 - when establishing the size of additional financial capital;

- sch. 84 - to calculate the amounts of undistributed profits or uncovered losses.

Negative values are entered without the minus sign; such indicators are indicated in parentheses. If there is no accounting data to be reflected in the table rows, a dash is placed or the field is left blank.

We register the information in the second section.

If during the reporting period the company made adjustments to its accounting policies or significant errors were identified that resulted in a change in the financial capital of the economic entity, information about these circumstances must be provided in the second part of the reporting form.

Data is entered line by line. First of all, the values before adjustments are recorded, then the corrections made are indicated by type, and only then the data after adjustments are made are recorded. Such transactions should be reflected separately by type of financial capital.

Let's fill out the third section.

The last table of reporting form No. 3 contains only one indicator, but for three reporting years. However, this indicator is calculated using a special formula. To calculate the amount of net assets, you will need balance sheet data (OKUD 0710001) for similar periods.

The calculation is carried out according to the formula:

NA = (line 1600 – DU) – (line 1400 + line 1500 – DBP).

Net assets = (line 1600 of the balance sheet – debts of the founders for the formation of the management company) – (line 1400 + line 1500 of the balance sheet – deferred income),

Where:

- line 1600 - the total value of non-current and current assets of the enterprise as of the reporting date;

- line 1400 - long-term liabilities and debt relationships;

- line 1500 - short-term debts and obligations assumed by the organization.

Let us recall that this indicator is calculated as the difference between the company’s assets and assumed liabilities, regardless of their duration.

Source: //ppt.ru/art/buh-uchet/izmenenie-kapitala

Movement of capital

This section is a table in which indicators characterizing the reasons for changes in capital are listed on the left line by line, and capital items are presented in columns on the right:

- column 3 “Authorized capital”;

- column 4 “Own shares purchased from shareholders”;

- column 5 “Additional capital”;

- column 6 “Reserve capital”;

- column 7 “Retained earnings (uncovered loss)”;

- Column 8 “Total”.

The first line of section (3100) is titled: “The amount of capital as of December 31, 20__.”

This line reflects the data from the year before last.

Let us show with an example what data needs to be shown in it.

Example

An organization reports for 2021.

In line 3100, the accountant will reflect the value of each part of capital as of December 31, 2014.

In line 3200 you need to reflect the amount of capital as of December 31 of the year preceding the reporting year.

If you're reporting for 2021, it's 2015.

General requirements and header part of the report

The statement of changes in equity consists of three sections.

Section 1 is devoted to the movement of capital of the company. It should reflect data on the authorized, additional and reserve capital, as well as on own shares purchased from shareholders, and on the amount of retained earnings (uncovered loss).

The data in the form is indicated not only for the reporting year, but also for the two previous years. Thus, in the report for 2012, in addition to the data of the current reporting period, information is provided for 2011 and 2010.

The indicators of the reporting year and previous years, which are indicated in the report, must be comparable. This allows you to analyze them in dynamics. If the company’s accounting policy did not change significantly in the reporting year, then the indicators for the previous year will coincide with the data of the previous report. If the accounting policy has changed, then it is impossible to rewrite data from last year’s document into a new report. Adjustments need to be made. And the reasons for the discrepancies between the indicators relating to the previous year should be explained in the Explanatory Note.

Section 2 of the report contains information about adjustments that are associated with changes in accounting policies and correction of errors. Indicators are reflected both before and after adjustment.

Section 3 includes data on the company’s net assets in the reporting period and in the two previous periods.

The statement of changes in capital is signed by the head of the company and its chief accountant.

The header part of the report is formatted similarly to the header part of the balance sheet.

The tabular part of the report is filled out in thousands or millions of rubles (code 384 or 385).

Important

The rules for filling out a statement of changes in capital are described in detail in the book “Annual Report 2012″, edited by Vladimir Meshcheryakov.”

Along with the useful book, you will receive a free access code to the Internet portal in support of submitting the annual report www.buhgod.ru and will be able to use the book in electronic format.

Column 3 “Authorized capital”

Here show changes in the authorized capital for the reporting and previous years.

If the company’s capital increased or decreased, then indicate the sources of the increase (reasons for the decrease) in the line-by-line transcripts.

Take the data for filling out this column from the accounting registers under account 80 “Authorized capital”.

Having shown the amount of the authorized capital, in the following lines “Increase in capital” reflect the amount of its increase.

Decipher the sources through which the authorized capital increased.

For this purpose, the report contains the following lines:

- “Additional issue of shares”;

- “Increase in the par value of shares”;

- "Reorganization of a legal entity."

The increase in the authorized capital is reflected in the credit of account 80 “Authorized capital”.

Line 3210 indicates its credit turnover for the past year. If during the last year the authorized capital decreased, then reflect the amount of the decrease in the lines “Decrease in capital”.

At the same time, it is necessary to disclose why such a decrease occurred.

For this purpose, the report contains the following lines:

- “Reduction in the par value of shares”;

- “Reducing the number of shares”;

- "Reorganization of a legal entity."

A decrease in the authorized capital is reflected in the debit of account 80 “Authorized capital”.

Line 3220 indicates its debit turnover for the past year. On line 3200, indicate the credit balance of account 80 at the end of last year.

Reflect the growth of the authorized capital in the reporting year in the same order as for the previous year.

- 3314 “Additional issue of shares”;

- 3315 “Increase in the par value of shares”;

- 3316 “Reorganization of a legal entity.”

In the form, indicate the credit turnover of account 80 “Authorized capital” for the reporting period.

If during the reporting year the company’s authorized capital decreased, fill in the lines in the “Decrease in Capital” section with the explanation:

- 3324 “Reduction in the par value of shares”;

- 3325 “Reduction in the number of shares”;

- 3326 “Reorganization of a legal entity.”

In the form, indicate the debit turnover of account 80 “Authorized capital” for the reporting period.

Reflect the amount of the authorized capital at the end of the reporting year on line 3300. This includes the credit balance of account 80 “Authorized capital” as of the end of the year.

Statement of changes in equity

Purpose of the statement of changes in equity

The procedure for preparing the Statement of Changes in Equity is set out in IAS 01 Presentation of Financial Statements. It also contains the key definitions used in compiling the Report:

Owners are the holders of instruments classified as equity instruments.

While all reporting in accordance with IFRS is sent to all interested users, the Statement of Changes in Equity, unlike the three other title forms of reporting, is addressed primarily to business owners (in the case of consolidated reporting, shareholders of the parent company).

Equity capital characterizes the share of the owners' funds in the total volume of its resources. Therefore, it is extremely important for them to know what part of the positive change in the value of net assets can be realized in the form of real cash payments - dividends. Accordingly, the disclosure of factors that determine the dynamics of equity capital plays the most important informational role of reporting. It is necessary to separate the change in equity as a result of the financial result of realized economic transactions from changes as a result of accounting estimates.

The total change in equity for a period is the total amount of income and expenses, including gains and losses, resulting from the activities of the enterprise during the reporting period. In addition, changes in capital include changes arising from transactions with owners (contributions to capital, repurchase of the enterprise's own equity instruments and payment of dividends) and the costs of such transactions.

The previous version of IAS 1 Presentation of Financial Statements required that items of income and expense that were recognized in a given period, but were not included in the income statement, were to be presented in the statement of changes in equity along with changes in equity involving owners.

Or an alternative option was used - in the statement of recognized income and expenses, reflecting the profit or loss of the reporting period (as a result of the income statement), other income and expenses, the effect of changes in accounting policies and error corrections.

IAS 1, as amended, requires all changes in equity resulting from transactions with owners as such (i.e. with owner participation) to be reported separately from changes in non-owner equity. Businesses can no longer present items of comprehensive income (i.e., non-owner changes in equity) in the Statement of Changes in Equity. This is due to the principle of aggregating information with similar characteristics and separating items with different characteristics.

All income and expenses must be presented in one statement (the statement of comprehensive income) or two statements (the income statement and the statement of comprehensive income) – separately from changes in equity involving owners. Items of other comprehensive income (i.e., other than those reported in the income statement) must be included in the statement of comprehensive income.

All of the above boils down to the conclusion that changes in the capital of an enterprise between two reporting dates reflect an increase or decrease in its net assets for this period.

Disclosures related to capital

The standard specifies what information must be disclosed in relation to changes in equity. Some of them are required to be presented in the Change Report Report (title report). For other disclosures, the standard allows the reporting entity to independently determine whether to disclose data in the title report or in the Notes to it.

This is important to consider when developing reporting content, as the reporting format must be consistent.

Specifically, in the Report on Changes in Capital itself, the following must be presented:

- total comprehensive income for the period, showing separately the total amounts attributable to the owners of the parent and to non-controlling interests;

- for each component of equity, the effect of retrospective application or retrospective restatement recognized in accordance with IAS 8;

- For each component of equity, a reconciliation of the carrying amount at the beginning and end of the period, disclosing separately changes due to:

(i) items of profit or loss;

(ii) items of other comprehensive income;

(III) transactions with owners acting in that capacity, separately reflecting contributions made by owners and distributions to owners, and changes in ownership interests in subsidiaries that do not result in a loss of control.

Either in the statement of financial position, statement of changes in equity or in the notes, an entity must disclose:

(a) in relation to each class of share capital:

(i) the number of shares authorized for issue;

(ii) the number of shares issued and fully paid, as well as the number of shares issued but not fully paid;

(III) the par value of the share or an indication that the shares have no par value;

(IV) reconciliation of the number of shares outstanding at the beginning and end of the period;

(v) the rights, privileges and restrictions of the class, including restrictions on the distribution of dividends and the return of capital;

(VI) shares of an enterprise owned by the enterprise itself or its subsidiaries or associated enterprises;

(VII) shares reserved for issue under options and share sales agreements, including terms and amounts.

(b) a description of the nature and purpose of each capital reserve within capital.

In practice, the above disclosures are generally provided as part of the Notes.

In addition, in the Report itself or in the notes thereto, the entity must disclose the amounts of dividends recognized as distributions to owners and the corresponding per share figures.

Capital components include:

- each class of contributed capital

- accumulated balance for each class of other comprehensive income

- accumulated balance of retained earnings.

An entity without share capital, such as a partnership or trust, must disclose information equivalent to that required by the standard as a whole, setting out changes in each category of equity interests that have occurred during the relevant period and the rights, privileges and restrictions of each category of interests. in capital.

An example of preparing a Statement of Changes in Capital

ABC's net profit for 2014 amounted to 225 million rubles.

At the beginning of 2014, ABC Company's equity included:

- Share capital – 400 million rubles.

- Share premium – 50 million rubles.

- Revaluation reserve – 200 million rubles.

- Retained earnings - 700 million rubles.

For 2013, shareholders were paid dividends in the amount of RUB 100 million.

As of December 31, 2014, ABC revalued fixed assets using the direct method, as a result of which the revaluation reserve increased by RUB 350 million. During 2014, real estate assets were sold for which the amount of previously accrued revaluation amounted to RUB 55 million. In addition, if ABC had calculated depreciation based on historical (original) rather than revalued cost, then the cost of depreciation of fixed assets would have amounted to 6 million rubles, while in the reporting period depreciation charges were equal to 16 million rubles.

In 2014, ABC made an additional issue of shares. Proceeds from the issue amounted to 450 million rubles, including the par value of the outstanding shares - 150 million rubles, and share premium - 300 million rubles.

In IFRS, the revaluation reserve for fixed assets is usually written off gradually to retained earnings, in particular, when a fixed asset is disposed of - in the amount of the revaluation previously accrued on it, when operating a fixed asset - gradually over the entire service life of the fixed asset in the amount of the difference between the depreciation calculated from the revalued value, and depreciation determined from the original cost.

Accordingly, based on the results of 2014, the Statement of Changes in Own Capital will look as follows:

| Share capital | Share premium | Revaluation reserve | retained earnings | Total | |

| Balance at the beginning | 400 | 50 | 200 | 700 | 1350 |

| Revaluation of fixed assets | 350 | 350 | |||

| Net profit | 165 | 165 | |||

| Dividend payment | -15 | -15 | |||

| Issue of shares | 150 | 300 | 450 | ||

| Transfer of revaluation: - for sold objects | -55 | 55 | 0 | ||

| - by operating facilities | -10 | 10 | 0 | ||

| Closing balance | 550 | 350 | 485 | 915 | 2300 |

Recognition of Combined Instruments

Where a reporting entity issues combined financial instruments (for example, bonds convertible into shares), it is necessary to follow the guidance in IAS 32 Financial Instruments: Presentation or IFRS 2 Share-based Payment. , separate the liability component from the total value of the instrument, define the remaining portion as an element of capital and reflect the instrument accordingly on the balance sheet.

Example

ABC issued bonds in the amount of 100 million rubles on 01/01/2014. at an annual interest rate of 5%. Interest is payable annually at the end of the period, and the principal amount of $100 million is due on December 31, 2021. At the discretion of investors, the debentures may be converted into shares until December 31, 2021. The annual market interest rate on non-convertible loans as of 01/01/2014 was 8%. Discount factors for 5 years: 5% - 0.78, 8% - 0.68. Present value cumulatively RUB 1 million payable at the end of the 5-year period: 5% - RUB 4.33 million. 8% - 3.99 million rubles.

Reflection Approach

The annual interest expense will be 5 million rubles. A bond loan is a combined financial instrument and includes debt and equity components. The debt component is calculated as the present value of potential future payments

5,000 x 3.99 = 19,950 thousand rubles 100,000 x 0.68 = 68,000 thousand rubles Total amount of liability at the end of 2014 = 87,950 thousand rubles.

The equity component is defined as the difference between the loan amount received and the debt component

The debt component is equal to 87,950 thousand rubles. Equity component (balancing figure) - 12,050 thousand rubles. Total received from the bond issue - 100,000 (100,000 - 87,950 = 12,050)

The debt component is recorded as a long-term financial liability.

Financial expenses for the year are equal to 87.950 * 8% = 7.036

The following information will appear in the statement of changes in capital:

| Share capital | Share premium | retained earnings | Total | |

| Balance at the beginning | 400 | 50 | 700 | 1150 |

| Net profit | 225 | 225 | ||

| Dividend payment | -100 | -100 | ||

| Issue of shares* | 5 | 7 | 12 | |

| Closing balance | 405 | 57 | 825 | 1287 |

*To simplify the example, data on the calculation of the amount of share premium is not provided; this is not related to the topic of the article.

Changes in accounting policies and correction of errors

IAS 8 requires retrospective adjustments to reflect changes in accounting policies (where feasible and unless the transition conditions in another IFRS require otherwise).

IAS 8 also requires retrospective restatements to correct material errors (where possible).

Retrospective adjustments and retrospective restatements do not represent changes in equity but are adjustments to the opening balance of retained earnings unless an IFRS requires a retrospective adjustment to another component of equity. IAS 1 requires that the statement of changes in equity disclose the total amount of adjustments for each component of equity separately as a result of changes in accounting policies and corrections of errors. Such adjustments must be disclosed for each prior period and at the beginning of the current period.

IFRS 8 provides two approaches to correcting fundamental errors.

The basic approach is to adjust the opening balance of retained earnings; comparative information is updated if necessary.

An acceptable alternative approach is adjusting the financial result of the reporting period; comparative information is not updated.

The following information must be disclosed in the notes to the financial statements:

- what is the error;

- the amount of the adjustment that affects all periods presented in the financial statements and prior periods;

- how the error was corrected, whether the comparative information was updated.

An example of reflecting adjustments as a result of changes in accounting policies

Since 2013, changes to the standard IAS 19 “Employee Benefits” came into force; according to the order of entry into force, it was required to reflect the effect of the change in policy as a result of the change in the standard.

Recalculation effect:

| As of December 31, 2013 (previously reflected) | Effect of changes in accounting policies | As of December 31, 2013 (restated) | |

| Employee Benefit Liabilities | 120 | -20 | 100 |

| Total liabilities | 745 | -20 | 725 |

| Deferred tax assets | 24 | -4 | 20 |

| Total assets | 2 140 | -4 | 2 136 |

| retained earnings | 775 | -16 | 759 |

| Total equity | 1 395 | -16 | 1 379 |

As a result, an additional line will appear in the Report of Changes in Equity:

| Share capital | Share premium | Revaluation reserve | retained earnings | Total | |

| Balance as of January 1, 2014 | 400 | 50 | 200 | 700 | 1350 |

| Impact of changes in accounting policies | 16 | 16 | |||

| Balance as of January 1, 2014 | 350 | 55 | 215 | 716 | 1336 |

| Revaluation of fixed assets | 350 | 350 | |||

| Net profit | 225 | 225 | |||

| Dividend payment | -100 | -100 | |||

| Issue of shares | 150 | 300 | 450 | ||

| Transfer of revaluation: - for sold objects | -55 | 55 | 0 | ||

| - by operating facilities | -10 | 10 | 0 | ||

| balance as of December 31, 2014 | 500 | 355 | 500 | 906 | 2261 |

Reflection of non-controlling interests

In accordance with the requirements of IFRS (IAS) 1, in the statement of financial position of the organization in the “Capital” section, the following should be reflected separately:

- issued capital and reserves attributable to the owners of the parent company;

- non-controlling interests in the capital of subsidiaries at the reporting date.

Obviously, this requirement applies only to consolidated financial statements. In its separate statements, the investor company does not reflect the assets and liabilities of subsidiaries, therefore there is no uncontrolled interest in its capital

It should be noted that previously the Minority Interest (as the non-controlling interest in capital was previously called, relating to minority shareholders of both the parent and subsidiaries) was not included in the capital, but was reflected in the balance sheet between the sections Capital and Long-term liabilities.

Given that the new version of IAS 1 recognizes non-controlling interests in equity, the Statement of Changes in Equity provides information for each type of change in equity that relates to non-controlling interests.

Example of reflecting non-controlling interests

Let’s say that on June 30, 2014, ABC company acquired 75% of the shares of DEF, whose profits grew evenly throughout the year. As of 01/01/2014, retained earnings DEF amounted to 200, profit for 2014 DEF amounted to 80 million rubles.

According to the algorithm for applying the acquisition method, only profit for the period of ownership of controlling interests will appear in the consolidated statements, i.e. for the 2nd half of 2014 in the amount of 40 million rubles, of which 30 million rubles. Accounted for by the owners, and 10 million rubles. – refers to non-controlling interest. As a result, the Consolidated Statement of Changes in Equity will appear as follows:

| ABC Company Shareholders' Equity | Non-controlling interest | |||||

| Share capital | Share premium | Revaluation reserve | retained earnings | Total | ||

| Balance as of January 1, 2014 | 400 | 50 | 200 | 700 | 1350 | |

| Revaluation of fixed assets | 350 | 350 | ||||

| Net profit | 255 | 10 | 265 | |||

| Dividend payment | -100 | -100 | ||||

| Issue of shares | 150 | 300 | 450 | |||

| Transfer of revaluation: - for sold objects | -55 | 55 | 0 | |||

| - by operating facilities | -10 | 10 | 0 | |||

| balance as of December 31, 2014 | 150 | 300 | 285 | 220 | 10 | 2315 |

Reflection of other transactions with shareholders

As part of other transactions, we will consider one-time non-refundable contributions from shareholders (increase in capital) and repurchase of own shares from shareholders (reduction in capital), combining these cases to simplify the presentation.

After the introduction of exemption from income tax on contributions from shareholders owning controlling shares in (Article 251 of the Tax Code of the Russian Federation), business owners use this “benefit” to instantly increase the net assets of controlled companies without the technical difficulties and costs associated with increasing the authorized capital.

In Russian accounting, this operation is reflected as other income, while in IFRS it is reflected as other contributions from shareholders or other equity capital, combining one-time contributions and share premium. This is a fairly common amendment when carrying out a transformation.

The repurchase of own shares, regardless of the grounds for such actions, leads to a decrease in equity capital and is accordingly reflected in the Statement of Changes in Capital.

| Share capital | Share premium | Shareholder contributions | retained earnings | Total |

| Balance at the beginning | 400 | 200 | 700 | 1300 |

| Redemption of own shares | -50 | -25 | -75 | |

| Other capital transactions | 70 | |||

| Net profit | 225 | 225 | ||

| Closing balance | 350 | 175 | 925 | 1450 |

In conclusion, it should be noted that the list of cases that are reflected in the Statement of Changes in Equity is open and includes:

- Change in revaluation reserve for financial assets held for sale

- Change in hedging reserve

- Change in actuarial profit

- Change in interests of non-controlling shareholders

- Effect of transactions under common control

- Translational adjustments from translation into foreign currency

- As well as changes due to other factors

The above examples clearly demonstrate the impact of various economic phenomena on the funds at the “disposal” of company owners.

Source: Press service of AKG " BUSINESS PROFILE " (GGI), magazine "IFRS in Practice" No. 9

Column 5 “Additional capital”

Column 5 reflects data on the movement of the company's additional capital.

It changes, for example, as a result of the revaluation of fixed assets. To fill out column 5, use the data reflected in account 83 “Additional capital”.

First, give the amount of additional capital at the end of the year that preceded the previous year (reporting year minus two years).

Then, in the lines “Revaluation of property”, indicate the amount of increase or decrease in additional capital after the revaluation of the company’s property.

Write down the final amount of capital (including revaluation) in line 3300.

Reflect the amount of the company’s additional capital at the end of the last year, that is, 2015, in line 3200.

In the next line - 3312 - show the amount of the increase in additional capital from the revaluation of property carried out at the end of the reporting year, that is, 2021.

If, as a result of revaluation, additional capital has decreased, then write down the amount of the decrease in line 3322.

On lines 3213 and 3313 “Income attributable directly to the increase in capital”, show the amount of VAT transferred to your company by the participant (shareholder) when paying for their shares (shares) in non-cash.

In accounting for this operation, the corresponding entry is Debit 19 Credit 83.

Reflect the amount of additional capital at the end of the reporting year in the final line 3300. This is the balance in account 83 “Additional capital” at the end of the reporting year.

Column 6 “Reserve capital”

The firm's reserve capital is formed from retained earnings.

All joint stock companies are required to do this.

In this case, the amount of reserve capital must be at least 5% of the authorized capital (clause 1, article 35 of the Law of December 26, 1995 N 208-FZ).

This means that the charter of a joint stock company can provide for reserve capital in a larger amount.

Limited liability companies are not required to create a reserve fund.

But at the request of the founders, enshrined in the charter and reflected in the accounting policies, such companies can also create a reserve fund.

Account 82 “Reserve capital” is used to account for it. Therefore, to fill out column 6 “Reserve capital” of the report, use data on transactions on this account.

Information on changes in reserve capital in the report is also provided for two years and is reflected similarly to authorized and additional capital.

Column 7 “Retained earnings (uncovered loss)”

Here they reflect information about the movement of retained earnings (uncovered losses) of the company.

It is formed from the profit remaining after paying income tax and contributions to reserve capital.

To fill out column 7, use the data from account 84 “Retained earnings (uncovered loss).”

If the company’s accounting policies changed during the previous and reporting years, this should affect the amount of retained earnings (clauses 14 and 15 of PBU 1/2008).

It should be noted that in 2021, there were no changes in regulatory legal acts that entail the need to revise accounting policies.

For the lines “Revaluation of property”, show the amount of retained earnings from the revaluation of fixed assets, intangible assets and exploration assets.

When non-current assets are disposed of, the amount of their revaluation is transferred from additional capital to the company's retained earnings.

In the final line 3300, show the credit balance of account 84 at the end of the reporting period.

Sample report (form No. 3)

So, how to fill out the document correctly? A detailed example is given in Order No. 66n. It can be filled out in two ways:

- With line codes if it is submitted to statistical authorities

- It is also possible not to indicate codes, but only if the document will be used for internal analytical data

Such reporting is precisely what is needed in order to reveal in more detail the changes that affected capital during the reporting period. Information is reflected in three blocks:

- in section

- according to the changes that have occurred

- in the form of a link to a specific year

The document must be completed by legal entities only. Exceptions are budget companies, credit organizations, insurance and small enterprises. The report should be submitted to the tax office where the company was registered.

Example of filling out a report in the video:

The document is filled out exclusively in monetary terms. If the amounts are negative, then a minus is not placed in front of them - the amounts are enclosed in parentheses. As for those sections that are not filled in, they should be marked with a dash.

As you can see, filling out the document does not take too much time. But the benefits of such a document as analytical information are undeniable.

Top

Write your question in the form below

Adjustment due to changes in accounting policies and correction of errors

In Sect. 2 statements reflect adjustments to equity as of December 31:

- the year preceding the reporting year (last year);

- the year preceding the previous one (the year before last).

Please note: fill out section.

2 is necessary only in cases where in the reporting year the company changed its accounting policies or corrected significant errors from previous reporting periods. First, indicate the amount of capital before adjustments (line 3400).

Then reflect the amount of adjustment due to changes in accounting policies (line 3410) and correction of errors (lines 3420).

After this, the amount of capital after adjustment is calculated (line 3500).

Lines 3401 - 3502 provide a breakdown of data on retained earnings (uncovered loss) and other capital items for which the adjustment is made.

Composition of the capital flow statement

If you are filling out paperwork for the previous reporting period, you must provide the following information:

- The balance of funds that fell on January 1 of the reporting period

- By what amount has the capital increased, and in what categories is net profit, revaluation, etc.

- In which sections, on the contrary, did the decrease occur?

- Were there any adjustments for additional capital, and what?

- Availability of adjustments to reserve capital

For the current year you must provide the following information:

- What amount remained with the company at the end of the previous year?

- In which area has there been an increase, and in which, on the contrary, has there been a loss?

- Changes in reserve and additional finances

- What capital remained at the end of the year

Net assets

In Sect. 3 of the report provides information on the size of the company’s net assets as of December 31:

- reporting year;

- previous (last) year;

- the year preceding the previous one (the year before last).

Net assets are determined by subtracting the amount of its liabilities from the sum of all assets of the company (with the exception of certain indicators of assets and liabilities).

In other words, net assets are the value of the enterprise’s current and non-current assets, secured by its own funds.

In addition to filling out the statement of changes in capital, the amount of net assets is also needed:

- to control the size of the authorized capital;

- to determine the estimated share price.