Step-by-step instruction

If, as of 01/01/2021, special clothing and special equipment (account 10.11.1) are in use, then it is permissible not to change the method of maintaining accounting records, incl. ways to repay the cost. We do not write off balances manually, we leave everything as is (Letter of the Ministry of Finance of the Russian Federation dated March 12, 2021 N 07-01-09/17431).

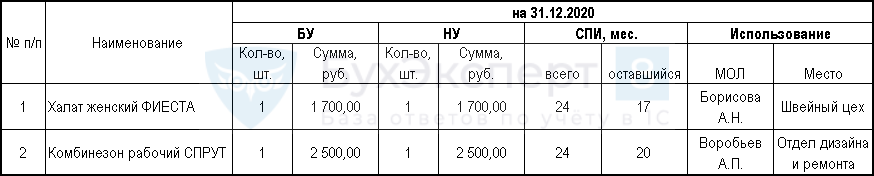

As of December 31, 2020, the accounts reflect the remains of workwear with a service life of more than 12 months.

Account 10.10 “Special equipment and special clothing in the warehouse” includes special clothing returned to the warehouse by a dismissed employee:

Account 10.11.1 “Special clothing in use” includes special clothing in use by employees:

Until 2021, in BU and NU, the costs of purchasing workwear were taken into account in a linear manner according to the useful life (SPI).

From 01/01/2021, the accounting policy for accounting has been amended:

- costs for the purchase of workwear are recognized as expenses for the period in which they are incurred;

- the consequences of changes in accounting policies in connection with the transition to FAS 5/2019 “Inventories” are reflected prospectively.

From 01/01/2021, the following changes have been made to the accounting policy for NU:

- costs of purchasing workwear worth no more than 100 thousand rubles. are taken into account as expenses in full at the time of commissioning.

Let's look at step-by-step instructions for creating an example. PDF

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Recognition in accounting expenses of the remaining cost of workwear in connection with the transition to FSBU 5/2019 | |||||||

| January 01 | 91.02 | 10.11.1 | 4 200 | Recognition in accounting expenses of the remaining cost of workwear in connection with the transition to FSBU 5/2019 (in value and quantitative terms) | Manual entry | ||

| 91.02 | 10.10 | 1 125 | Recognition in accounting expenses of the remaining cost of workwear in connection with the transition to FSBU 5/2019 (only in value terms) | ||||

| Repayment of the cost of workwear in use at NU for January | |||||||

| January 31 | 20.01 | 10.11.1 | 225 | 225 | Repayment of the cost of workwear at NU | Manual entry | |

| Repayment of the cost of workwear in use at NU for February | |||||||

| 28th of February | 20.01 | 10.11.1 | 225 | 225 | Repayment of the cost of workwear at NU | Manual entry | |

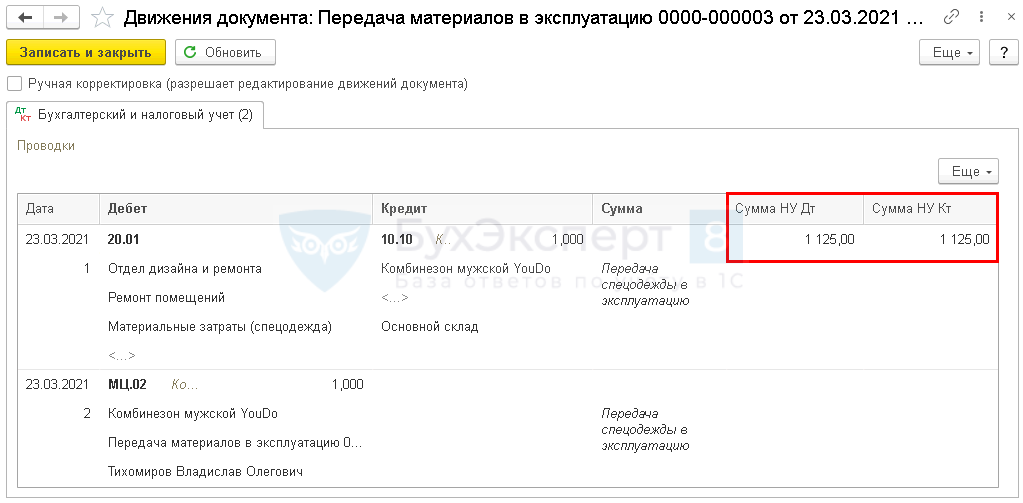

| Transfer of special clothing into service | |||||||

| March 23 | 20.01 | 10.10 | 1 125 | 1 125 | Repayment of the cost of workwear in NU upon re-transmission into operation | Transfer of materials into operation | |

| MC.02 | Reflection of workwear off-balance in quantitative terms | ||||||

| Repayment of the cost of workwear in use at NU for March, etc. | |||||||

| March 31 | 20.01 | 10.11.1 | 225 | 225 | Repayment of the cost of workwear at NU | Manual entry | |

Accounting

Accounting for special clothing must be kept on account 10 “Materials”, broken down into subaccounts 10-10 “Special equipment and special clothing in warehouse” and 10-11 “Special equipment and special clothing in operation.”

The purchase of workwear is reflected on the date of its acceptance for accounting by the following entries:

Debit 10 “Materials”, subaccount “Special equipment and special clothing in warehouse”, Credit 60 “Settlements with suppliers and contractors”

— the purchase of workwear is reflected;

Debit 19 “Value added tax on acquired assets” Credit 60

— reflects the amount of VAT presented by the seller of workwear;

Debit 68 “Calculations for taxes and fees”, subaccount “Calculations for VAT”, Credit 19

— the amount of VAT presented by the seller is accepted for deduction;

Debit 60 Credit 51

— settlement has been made with the seller of workwear.

EXAMPLE 1. HOW TO ACCOUNT FOR SPECIAL CLOTHING

He is engaged in car washing.

In January, 10 pairs of rubber gloves were purchased for car wash employees at a price of 590 rubles. (including VAT - 90 rubles) and 10 pairs of rubber boots at a price of 4720 rubles. (including VAT - 720 rubles). In the same month, clothes and shoes were issued to the car wash employees. The manager's order established a useful life: for gloves - two months, for boots - 18 months. The accountant in January must do the following postings: Debit 10-10 Credit 60

- 500 rub.

(590 – 90) – gloves received; Debit 10-10 Credit 60

- 4000 rub.

(4720 – 720) – boots received; Debit 19 Credit 60

- 8100 rub.

((90 rub. + 720 rub.) × 10 pairs) – VAT reflected; Debit 60 Credit 51

- 5310 rub.

(590 + 4720) – special clothing is paid for; Debit 68 Subaccount “Calculations for VAT” Credit 19

- 810 rub.

– tax deduction has been made; Debit 10-11 Credit 10-10

- 500 rub.

– gloves were provided to employees; Debit 10-11 Credit 10-10

- 4000 rub.

– boots were issued to employees; Debit 20 (26) Credit 10-11

- 500 rub.

– the cost of the gloves issued is written off. Every month for 18 months, the accountant will make the following entries: Debit 20 (26) Credit 10-11

- 222.22 rubles. (4000 rubles: 18 months) – the cost of boots has been partially written off. Thus, by the end of the year 2666.64 rubles will be written off. (222.22 rubles × 12 months). The cost of workwear listed on account 10 at the end of the year will be 1333.36 rubles. (500 + 4000 – 500 – 2666.64). This amount will be indicated in the annual balance sheet on line 1210.

Transfer into operation

The commissioning of workwear is reflected depending on whether its cost is written off as expenses at a time or not.

The transfer of workwear into service with a one-time write-off on the date of issue to employees is reflected as follows:

Debit 20 “Main production” (08 “Investments in non-current assets”, 23 “Auxiliary production”, 25 “General production expenses”, 44 “Sales expenses”) Credit 10, subaccount “Special equipment and special clothing in warehouse”

— special clothing was issued to employees;

Debit 012 “Working clothes put into operation”

— protective clothing issued to employees is reflected on the balance sheet.

The transfer of workwear into service with a straight-line write-off on the date of issue to employees is as follows:

Debit 10, subaccount “Special equipment and special clothing in operation”, Credit 10, subaccount “Special equipment and special clothing in warehouse”

— special clothing was issued to employees.

Then in equal monthly installments during the wearing period:

Debit 20 “Main production” (08, 23, 25, 44) Credit 10, subaccount “Special equipment and special clothing in use”

— the repayment of part of the cost of workwear is reflected.

In case of disposal (for example, damage or loss) - on the date of disposal:

Debit 94 “Shortages and losses from damage to valuables” Credit 10, subaccount “Special equipment and special clothing in use”

— the residual value of the workwear is written off.

Adjustment of remaining workwear and special equipment as of 01/01/2021

Since 2021, FSBU 5/2019 has come into force, which introduced new rules for accounting for workwear and special equipment. Previously, according to PBU 5/01, these assets were recognized as inventories and were accounted for according to the rules specified in the Guidelines for accounting for special equipment and workwear, approved. By order of the Ministry of Finance of the Russian Federation dated December 26, 2002 N 135n.

Now, depending on the period of use of special clothing and special equipment, they should be taken into account as:

- OS, if the service life is more than 12 months;

- inventory if the service life is less than 12 months.

The organization has the right to approve in its accounting policy for objects with insignificant value, regardless of the period of use, that the costs of purchasing workwear and special equipment are recognized at the time they are incurred (clause 4 of Recommendation BMC R-122/2020-KpR dated 12/11/2020).

If the accounting policy from 2021 establishes such a procedure for accounting for assets with insignificant value, which will also include work clothes and special equipment, then in the accounting (BU) the balances of accounting accounts 10.10 and 10.11 must be written off from the balance sheet.

The write-off procedure depends on which method of transition to FAS 5/2019 is chosen in the accounting policy - prospective or retrospective.

With the retrospective method, postings are reflected through account 84. This is a very labor-intensive process that entails recalculating the balances in the accounting records as of 12/31/2020, 12/31/2019. Despite the fact that the standard allows all organizations, not only those using simplified accounting and reporting, to apply FAS 5/2019 prospectively (clause 47 of FAS 5/2019).

When choosing a promising method, reflect in:

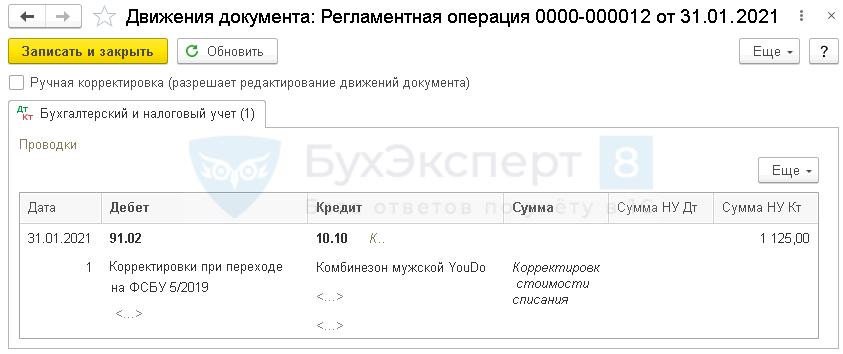

- BU - Dt 91.02 Kt 10.10 for the amount of the remaining cost of workwear;

- Well, accounting for workwear will not change. If the cost of workwear was written off linearly, continue writing it off in parts (clause 3, clause 1, article 254 of the Tax Code of the Russian Federation).

Recognition in accounting expenses of the balance of the cost of workwear in the warehouse as of 01/01/2021

Determining the remaining cost of workwear in the warehouse as of 01/01/2021

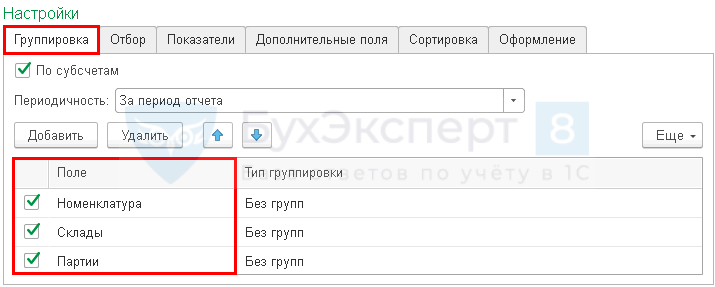

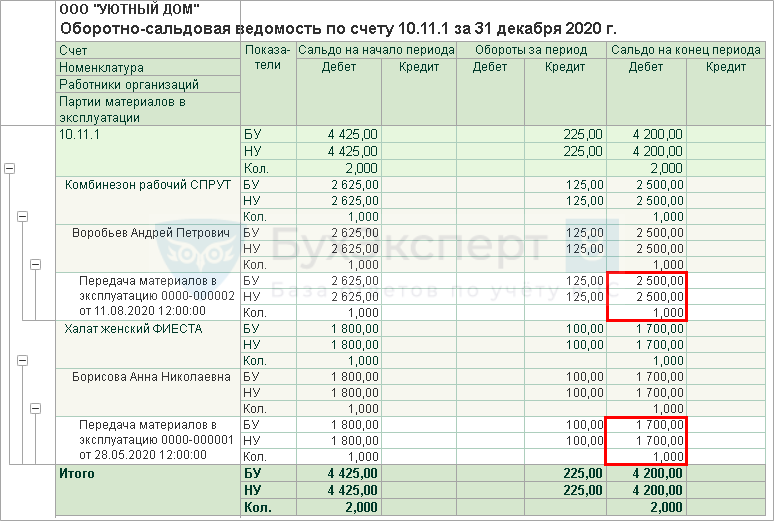

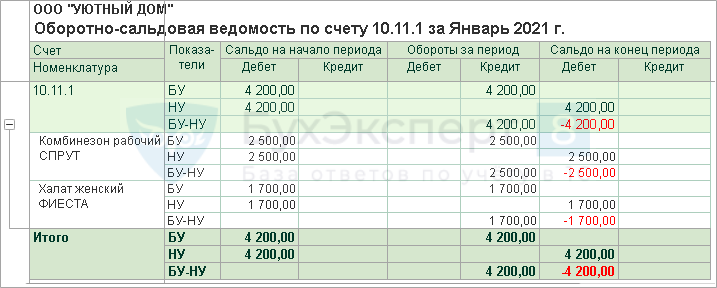

To determine the remaining cost of workwear in the warehouse, generate the report Balance sheet for account 10.10 in the Reports .

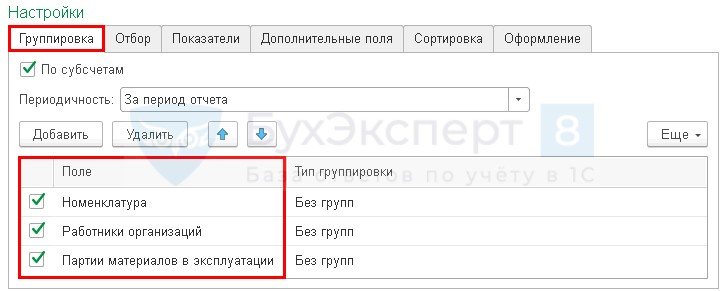

To display all data in OSV, in Show settings , set the grouping by Items , Warehouses , Batches . The settings will allow you to correctly fill out the document when recognizing the balance of the cost of workwear in the warehouse as an BU expense.

Recognition in accounting expenses of the balance of the cost of workwear in the warehouse

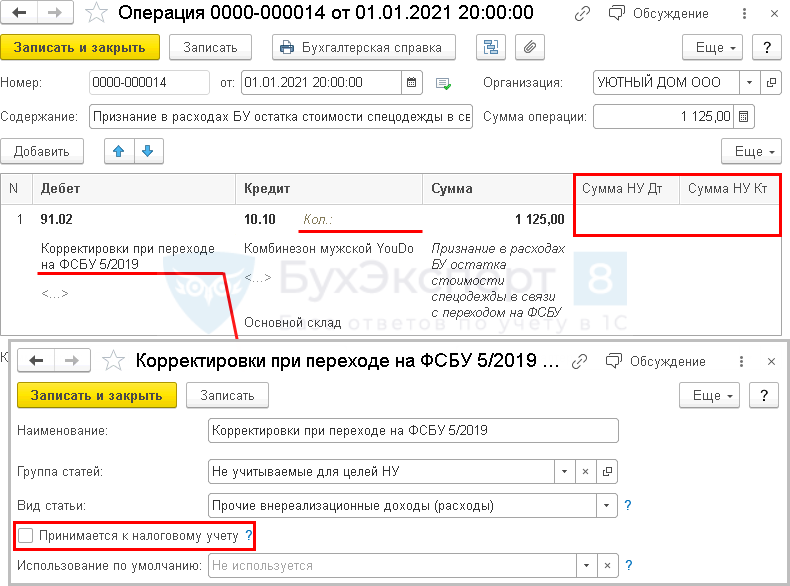

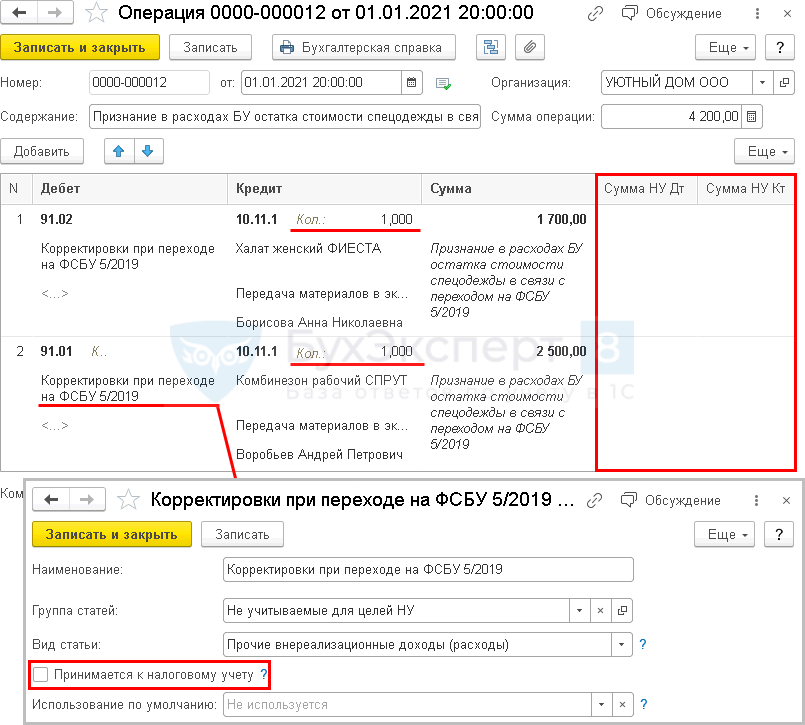

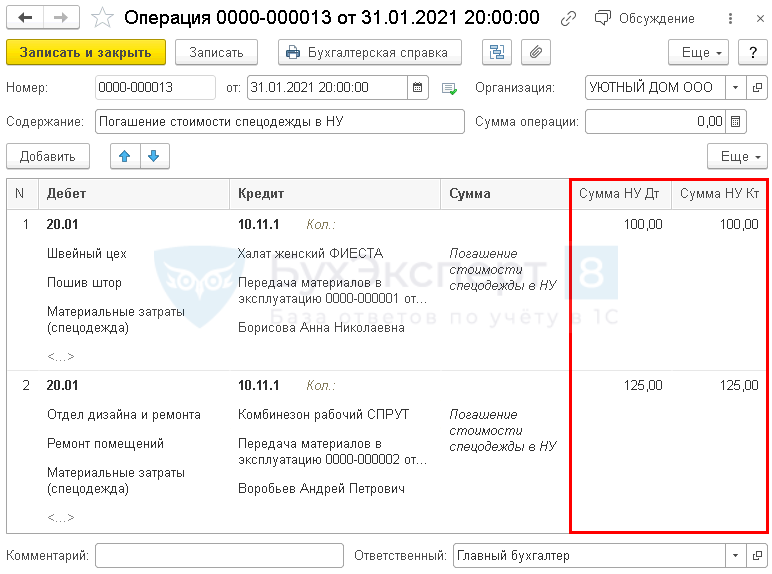

To recognize in accounting expenses the cost of workwear in a warehouse with a service life of more than 12 months in connection with the transition to FSBU 5/2019, enter the document Transaction entered manually in the Transactions .

When applying PBU 18/02 in accounting, temporary differences are formed for the asset Materials (clauses 11, 14, 15 PBU 18/02). SHE confesses. When special clothing is issued to an employee at NU, the deferred tax on it is automatically paid off.

Recognition of costs for the purchase of workwear YouDo men's overalls in the amount of RUB 1,125. expenses in BU and NU differ over time:

- BU - at the time of transition to FSBU 5 (from 01/01/2021);

- NU - after transferring the workwear to the next employee.

Therefore, at the time of recognizing the balance of the cost of workwear in accounting expenses, Accepted for tax accounting in the Other income and expenses .

Carefully transfer into the document the analytics for account 10.10 from the previously generated report Turnover balance sheet .

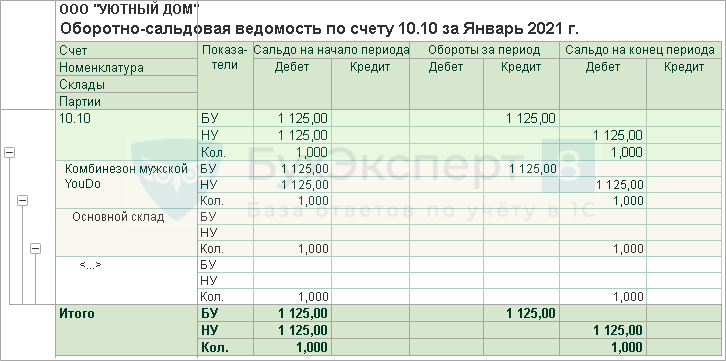

Do not fill in the quantity for invoice 10.10: otherwise, the cost of workwear in the warehouse in NU is automatically recognized as expenses on January 31 by the routine operation Adjustment of item cost at Month Closing.

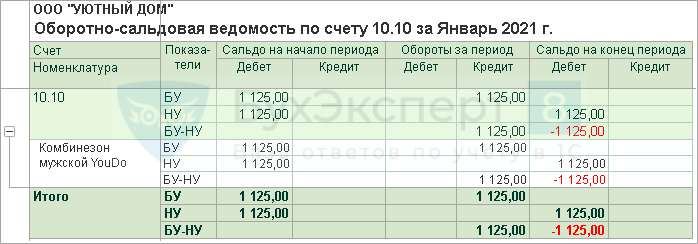

To check, we will create a balance sheet for account 10.10 for January.

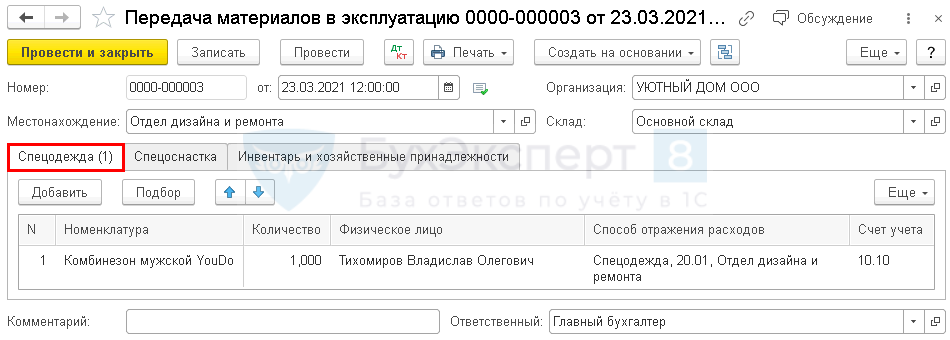

It is clear from the report that on account 10.10 only the amount for tax base remains, which will be taken into account in full as part of expenses that reduce the taxable base at the time of issuing special clothing to the employee. It is reflected in the document Transfer of materials into operation or Consumption of materials transaction type Transfer to employee in the Warehouse .

Repayment of the cost of workwear at NU

To transfer workwear to an employee, register one of the documents: Transfer of materials into operation or Consumption of materials, transaction type Transfer to employee in the Warehouse .

Learn more about using the document Material consumption when transferring workwear to an employee.

In our example, we will create a document Transfer of materials into operation.

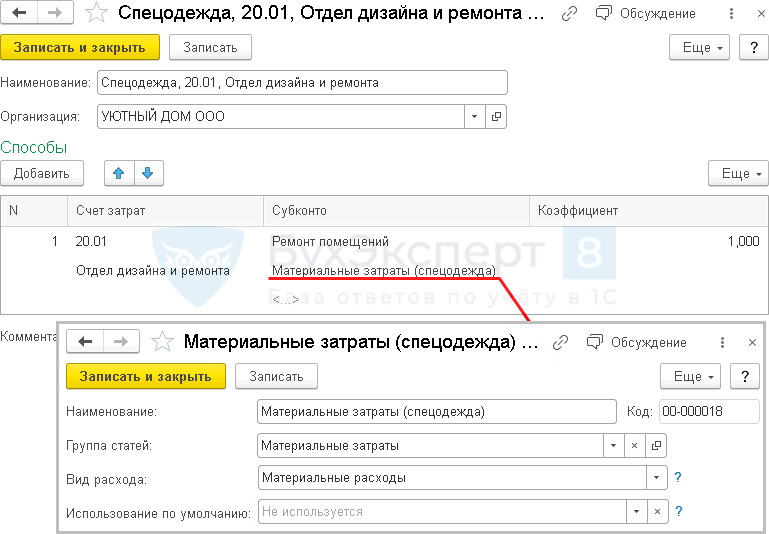

In the document, fill in the employee to whom the workwear is transferred and the Method of recording expenses .

Postings according to the document

The cost in NU will be repaid in a lump sum in full when the workwear is transferred to the employee, since changes have been made to the accounting policy for NU from 2021. In the 1C program, starting from 2021, only this method of paying off the cost will be supported for tax accounting of workwear and special equipment.

FSS will pay

Let us remind you that annually insurers can allocate up to 20% of insurance premiums for compulsory social insurance against industrial accidents and occupational diseases to prevent industrial injuries and occupational diseases.

All insurers, regardless of the form of ownership, type of activity and number of employees, have the right to financial support from insurance premiums for preventive measures on labor protection, if they carried out economic activities in the previous year. Financing is carried out in accordance with the Rules approved by Order of the Ministry of Labor dated December 10, 2012 No. 580n (hereinafter referred to as the Rules).

Applications for financial support for preventive measures are accepted until August 1. In particular, you can submit an application electronically through the Unified Government Services Portal www.gosuslugi.ru. The documents attached to the application are provided on paper, as specified by the FSS.

Financial support for preventive measures from the amounts of insurance premiums for this type of insurance is subject to the insurer's expenses for 12 occupational safety measures specified in the Rules, including the purchase of special clothing and other personal protective equipment for hazardous workers.

A prerequisite for receiving financing is the absence of arrears in the payment of insurance premiums, outstanding penalties and fines on the day of application.

Let us recall a few important nuances. Expenses for the purchase of workwear, footwear and other personal protective equipment manufactured exclusively on the territory of the Russian Federation are accepted.

But in addition to copies of certificates (declarations) of compliance with the requirements of the technical regulations of the Customs Union “On the safety of personal protective equipment”, with the application it is also necessary to submit copies of conclusions confirming the production of industrial products on the territory of the Russian Federation, issued by the Ministry of Industry and Trade in relation to the PPE selected for financing.

note

The company may recover damages from the negligent employee in the amount of the residual value of the workwear in court. In such cases, the courts recover damages from employees in the amount of the residual value of the workwear excluding VAT (appeal ruling of the Supreme Court of the Republic of Tatarstan dated May 15, 2014 in case No. 33-6316/2014).

The conclusion is a mandatory document when submitting an application and is valid for one year from the date of its issue. The list of issued conclusions is publicly available on the website of the Ministry of Industry and Trade. The expiration of the validity period of the conclusion is the basis for excluding information about the relevant conclusion from the specified list of issued conclusions. In addition, when submitting an application, the policyholder will have to indicate the date of manufacture of PPE and their expiration date.

In addition, from August 2021, an organization has the right to reimburse the costs of purchasing workwear only if it is made in Russia from fabrics, knitted fabrics, non-woven materials of a domestic manufacturer.

Here the question arises: when reimbursement of expenses for the purchase of workwear at the expense of the Federal Social Insurance Fund of Russia, is it necessary to restore the VAT, which was previously accepted for deduction from the budget? In our opinion, this is unnecessary, since such cases are not mentioned in paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

At the same time, if the Social Insurance Fund reimburses funds spent on injury prevention, including VAT, the organization has a double benefit: when purchasing and accounting for workwear, VAT was legally deducted, and subsequently the cost of PPE, including VAT, was reimbursed by the fund.

The likelihood that such a situation will cause claims from controllers is high.

But the risk is reduced in a situation where permission has been received from the FSS of Russia to reimburse expenses excluding VAT, presented by suppliers of workwear (letter of the Ministry of Finance of Russia dated August 14, 2015 No. 03-07-11/47007).

Officials confirmed the legality of deducting VAT if the cost of inventory items reduces insurance premiums to the Federal Social Insurance Fund of Russia without taking into account VAT. EXAMPLE 5. PPE “FROM FSS”

The company purchased workwear worth 10,000 rubles.

(excluding VAT). The workwear was transferred to employees in the same month, and its cost was written off as a lump sum expense. The Federal Insurance Service of Russia reimbursed the company for the costs of purchasing special clothing. The following entries must be made in accounting: Debit 10, subaccount “Special equipment and special clothing in warehouse”, Credit 60

- 10,000 rubles.

– reflects the cost of capitalized workwear; Debit 19 Credit 60

- 1800 rub.

– “input” VAT is taken into account on the cost of purchased workwear; Debit 68, subaccount “Calculations for VAT”, Credit 19

- 1800 rubles.

– accepted for deduction of VAT on the cost of workwear; Debit 10, subaccount “Special equipment and special clothing in operation”, Credit 10, subaccount “Special equipment and special clothing in warehouse”

- 10,000 rubles.

– special clothing was issued to employees; Debit 91, subaccount “Other expenses”, Credit 10, subaccount “Special equipment and special clothing in use”

- 10,000 rubles.

– the cost of issued special clothing is written off; Debit 69, subaccount “Settlements with the Federal Social Insurance Fund of Russia for contributions to insurance against accidents and occupational diseases”, Credit 76, subaccount “Settlements with the Social Insurance Fund of Russia for contributions to insurance against accidents and occupational diseases”

- 10,000 rubles.

– the debt to the Federal Social Insurance Fund of Russia for insurance premiums for the cost of workwear has been reduced; Debit 76, subaccount “Settlements with the Social Insurance Fund for contributions to insurance against accidents and occupational diseases”, Credit 91, subaccount “Other income”

- 10,000 rubles. – other income is recognized in the amount of actual expenses incurred for the purchase of workwear.

Recognition in BU expenses of the remaining cost of workwear in operation as of 01/01/2021

Determination of the remaining cost of workwear in use as of 01/01/2021

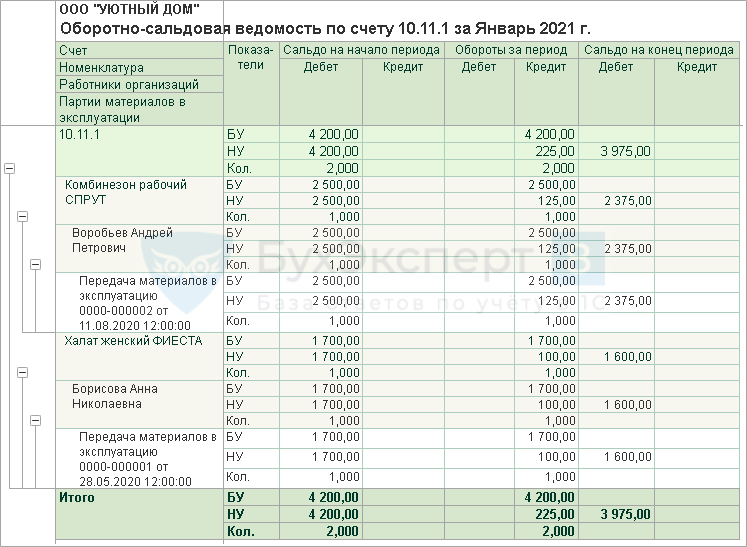

To determine the remaining cost of workwear in operation, generate the report Turnover balance sheet for account 10.11 in the Reports .

To display all data in OSV, in Show settings, set the grouping by Nomenclature , Employees of organizations , Batches of materials in operation . Such settings will allow you to correctly fill out the document when recognizing the remaining cost of workwear in use as BU expenses.

Recognition in used expenses of the remaining cost of workwear in operation

To recognize in accounting expenses the remaining cost of workwear in operation in connection with the transition to FSBU 5/2019, enter the document Transaction entered manually in the Transactions .

In NU, the balance of the cost of workwear in operation will continue to be included in expenses on a monthly basis, since during commissioning, according to the accounting policy of NU, the linear write-off method was used in proportion to the SPI. Therefore, at the time of recognizing the balance of the cost of workwear in accounting expenses, Accepted for tax accounting in the Other income and expenses .

When applying PBU 18/02 in accounting, temporary differences are formed for the asset Materials (clauses 11, 14, 15 PBU 18/02). SHE confesses. As the cost in NU is repaid, IT is automatically repaid.

In the Quantity , indicate the quantity of protective clothing in use, for which expenses are recognized in accounting.

Carefully transfer into the document the analytics for account 10.11.1 from the previously generated report Turnover balance sheet .

Repayment of the cost of workwear at NU

In NU, the cost of workwear should continue to be recognized as an expense on a monthly basis. But due to the fact that the cost of workwear is included in expenses in accounting, the accounting system will not automatically recognize its cost as expenses.

Therefore, every month it is necessary to enter a manually entered Transaction and fill it out yourself. To avoid errors, check the transactions and the monthly amount in the procedure Closing the month for December 2021 routine operation Repayment of the cost of workwear and special equipment .

To avoid errors in writing off the cost of workwear in NU, copy the previously created transaction every month until the cost of workwear is paid off in full.

To check, we will create a balance sheet for account 10.11.1 for January.

It is clear from the report that on account 10.11.1 there are only amounts left for NU, which will be included monthly in expenses taken into account for taxation of profits during the remaining period of operation using the document Transaction entered manually .

See also:

- [11/30/2020 entry] FSBU 5/2019 “Reserves”. We analyze it in detail. We are rebuilding accounting from 2021

- FSBU 5/2019. General issues

- How to reflect the transition to FAS 5/2019 in the financial statements for 2021?

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- When closing the month, transactions are not reflected in “Repayment of the cost of workwear and special equipment.” Good afternoon! When closing the month, transactions are not reflected in “Repayment...

- Acquisition and accounting of household equipment, special equipment You do not have access to view. To gain access: Complete...

- Simplified tax system 15%, accounting for special equipment in KUDiR The organization on the simplified tax system (15) purchased special equipment (preform) for 2 million rubles (100%...

- Accounting for special equipment worth more than 100 thousand rubles Good afternoon. Tell me how to take into account a magnetic plate worth 99,200...